Strong Q2 California Auction as Markets Await Reform Vote, EUAs and UKAs Rally on Linking Momentum

By Mark Lewis & Climate Finance Partners LLC (CLIFI)

4 Min. Read Time

The California Air Resources Board (CARB) meeting has extended into a second day, with the market awaiting the pivotal vote on the reforms to California’s carbon market. The reform process has been years in the making and is now nearing the finish line, with the package expected to be approved, a move that would lift the regulatory uncertainty weighing on the market over the past two years.

The positive Q2 CCA auction result announced on Wednesday of this week has already buoyed sentiment, and the greenlighting of the market-reform package would therefore leave CCAs primed to start moving structurally higher as the market assimilates the bullish implications of the tightening cap through 2030.

In Europe, both UKAs and EUAs were boosted this week by reports that the UK and EU will prioritize an agreement to link their carbon markets at their bilateral summit scheduled for July 13.

California crunch: Q2 CCA auction results positive as market awaits CARB Board vote

CCAs have had a strong month, with the benchmark Dec-26 contract closing at $30.97/t yesterday, up 6.4% from its April 30 settlement price. Market sentiment has been improving over the month ahead of the Q2 auction and the CARB Board vote on the market-reform package, now expected later today (May 29), after the large number of comments received in the public comment session yesterday (see our blog posts of May 21 and April 20 for more on the background to today’s vote).

As expected, most of the public comments related to the Manufacturing Decarbonization Initiative (MDI), which has sharply divided opinion. On the one hand, industry groups (especially the refining sector) have strongly supported the MDI proposal, while environmental groups oppose it and seek its removal from the package. At the same time, some interest groups (including some state legislators) oppose the MDI owing to the fiscal impact it will have on the state and its ability to fund other decarbonization initiatives.

All of that being said, we expected the reform package to be approved later today. If this is the case, it should pave the way for a sustained re-rating of CCAs over the rest of the year, as the market prices in the implications of a tighter cap, to be implemented from January 2027, through 2030.

The other significant development in California this week was the Q2 CCA auction. The current auction was fully subscribed, with all 49.6m V26 allowances sold at $28.81/t, up 87 cents on the Q1 auction, which cleared at the 2026 floor price of $27.94/t, and the highest auction settlement since Q1-2025. The cover ratio increased slightly to 1.11 from 1.04 in Q1, with demand exceeding supply by 5.5m allowances, the highest number for unfulfilled bids since the Q3-2025 auction. Compliance entities purchased 81.3% of the volumes offered (40.4m), and financials 18.7% (9.3m). This represented a near 40% increase in the volume of allowances purchased by financials compared with the Q1 auction, a clear sign of improving sentiment amongst speculative investors.

The advance auction also saw strong interest, with all V29 allowances selling at $28.76/t, up 82 cents on the Q1 outcome, and another healthy sign after the Q1 advance auction was undersubscribed.

UKAs boosted by renewed momentum on linking to EUAs, lifting EUAs in the process

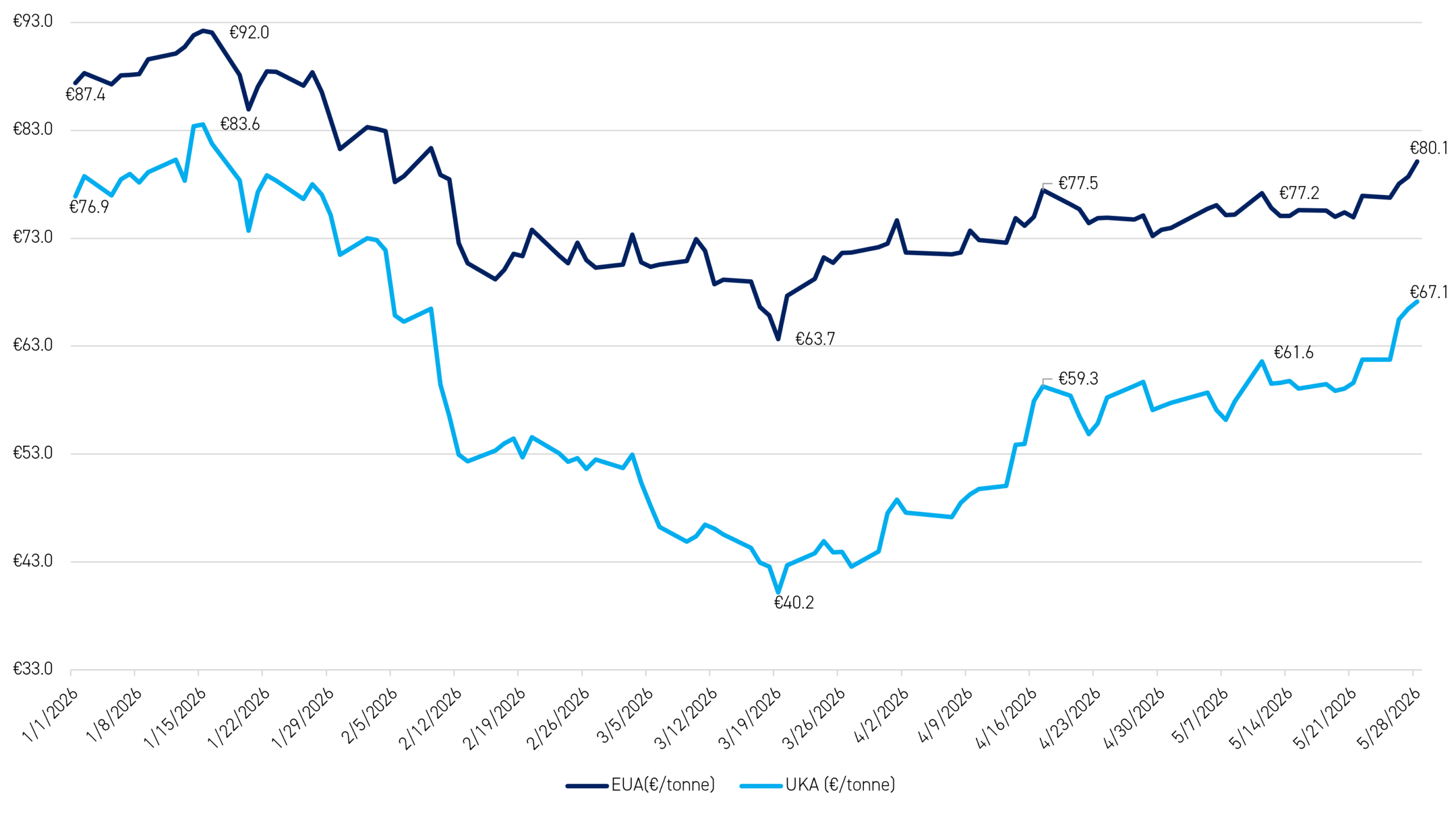

As of Thursday's settlement, EUAs are up 4% on the week to €80.1/t, and UKAs are up 8% at £67.1/t. This is the first time EUAs have closed above €80/t since February 9, when the politics of reforming the EU-ETS started to take center stage in the market narrative (see our blog of February 10).

The strong performance of UKAs, particularly over the last few days, reflects renewed market optimism about the prospect of the UK and the EU announcing an agreement to link their respective carbon markets at their July summit.

Figure 1: Front-Dec EUA (€/t) versus Front-Dec UKA (€/t*) 1 Jan-28 May 2026

Source: Bloomberg. *Note that we have converted UKA prices into €/tonne here for ease of comparison.

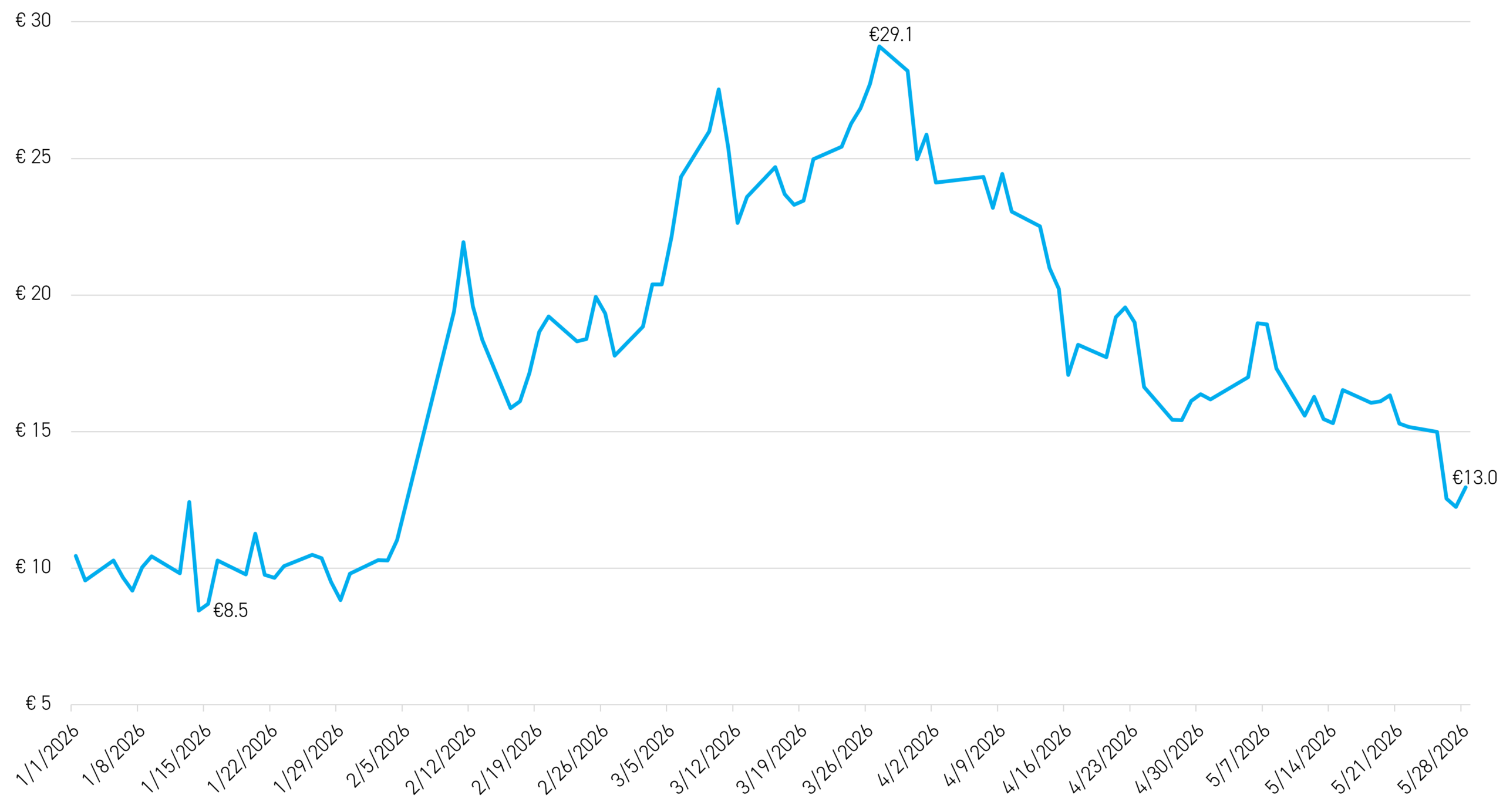

Figure 1 shows the price of the Dec-26 EUA contract versus the Dec-26 UKA contract since the beginning of this year, and Figure 2 shows the spread between the two (i.e., the discount at which UKAs trade versus EUAs).

Figure 1: Spread between Front-Dec EUA and Front-Dec UKA, 1 Jan-28 May 2026 (€/t)

Source: Bloomberg. *Note that we have converted UKA prices into €/tonne here for ease of comparison.

As shown in Figure 1, UKAs have clearly tracked EUAs' price action since the beginning of the year, though with a greater or lesser discount at any given time, reflecting the market’s optimism about a linking agreement materializing this year.

At the beginning of the year, optimism was high, and the discount hit a YTD low of €8.50/t in mid-January. Thereafter, however, the discount widened in the absence of newsflow around linking, as both the political pressure on the EU-ETS and the war with Iran's impact on energy markets put downward pressure on EUAs, squeezing the less liquid UKAs even harder. As a result, the discount reached its YTD high of €29.10/t in late March, around the same time both EUAs and UKAs hit their YTD lows.

Subsequently, the ceasefire, albeit fragile, with Iran announced on April 7 has helped calm nerves in global energy markets somewhat, with the benchmark front-month EU natural-gas price at the TTF hub in the Netherlands settling yesterday at €47/MWh, down 23% from its YTD high of €61/MWh recorded on March 19.

Against this backdrop, The Guardian newspaper reported last weekend that the UK and EU ‘hope to announce (…)an accord linking (their) emissions trading schemes’ at their July summit, and this is what has driven the spurt in UKAs this week, with EUAs getting something of a lift from the news as well.1

We are constructive on the UK and the EU reaching a deal on linking in July and on operational implementation of linking by January 2028. As a result, we think there is scope for the UKA discount to EUAs to shrink further in the coming weeks and months.

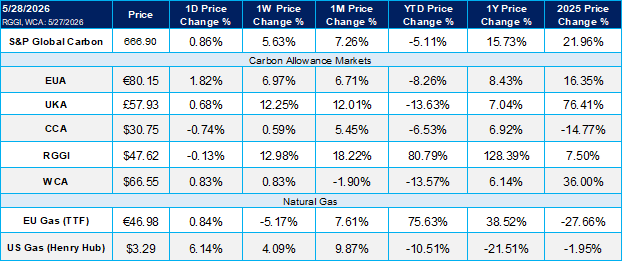

Carbon Market Roundup

The weighted global carbon price rose over the week to $57.65, up 5.63%. EUAs moved higher to €80.15, gaining 6.97% on the week, while UKAs climbed to £57.93, up 12.25%. In North America, CCA prices increased to $30.75, up 0.59%, and RGGI allowances advanced to $47.62, up 12.98%. WCA slipped modestly to $66.55, down 1.90% over the period.

- This makes sense from a fundamental point of view as on a medium to long-term basis the supply/demand balance in the UK-ETS is tighter than in the EU-ETS such that linking the two markets will increase the tightness of the EU-ETS at the margin.