UKAs Outshine EUAs, CARB Releases Amended ISOR in line with Rulemaking Deadline

5 Min. Read Time

UKAs bounced hard Thursday on the news that the UK would scrap its Carbon Price Support (CPS) mechanism from April 2028, thus reinforcing the momentum for linking the UK-ETS with the EU-ETS. EUAs benefited from the feel-good factor generated by weaker EU natural-gas prices as the ceasefire between the US/Israel and Iran continued to hold last week.

In the US, the big news was CARB’s release of the amended California Initial Statement of Reasons (ISOR) market reform package. The modified text was broadly in line with market expectations, marking a constructive step forward for the CCA rulemaking, with revisions largely clarifying industrial allocation mechanics and implementation details. The new Manufacturing Decarbonization Incentive (MDI) reserve, which awards ‘credits’ for eligible early-stage, capital-intensive decarbonization investments, drew the most attention, though CARB’s Rajinder Sahota noted the program is intended as a voluntary incentive and is unlikely to be fully utilized in the near term. This modified ISOR is now open for a quick 15-day public comment period that concludes April 29, keeping the rulemaking on track for the May 28 Board meeting.

UKAs reduce the gap to EUAs as market sees renewed momentum on linking

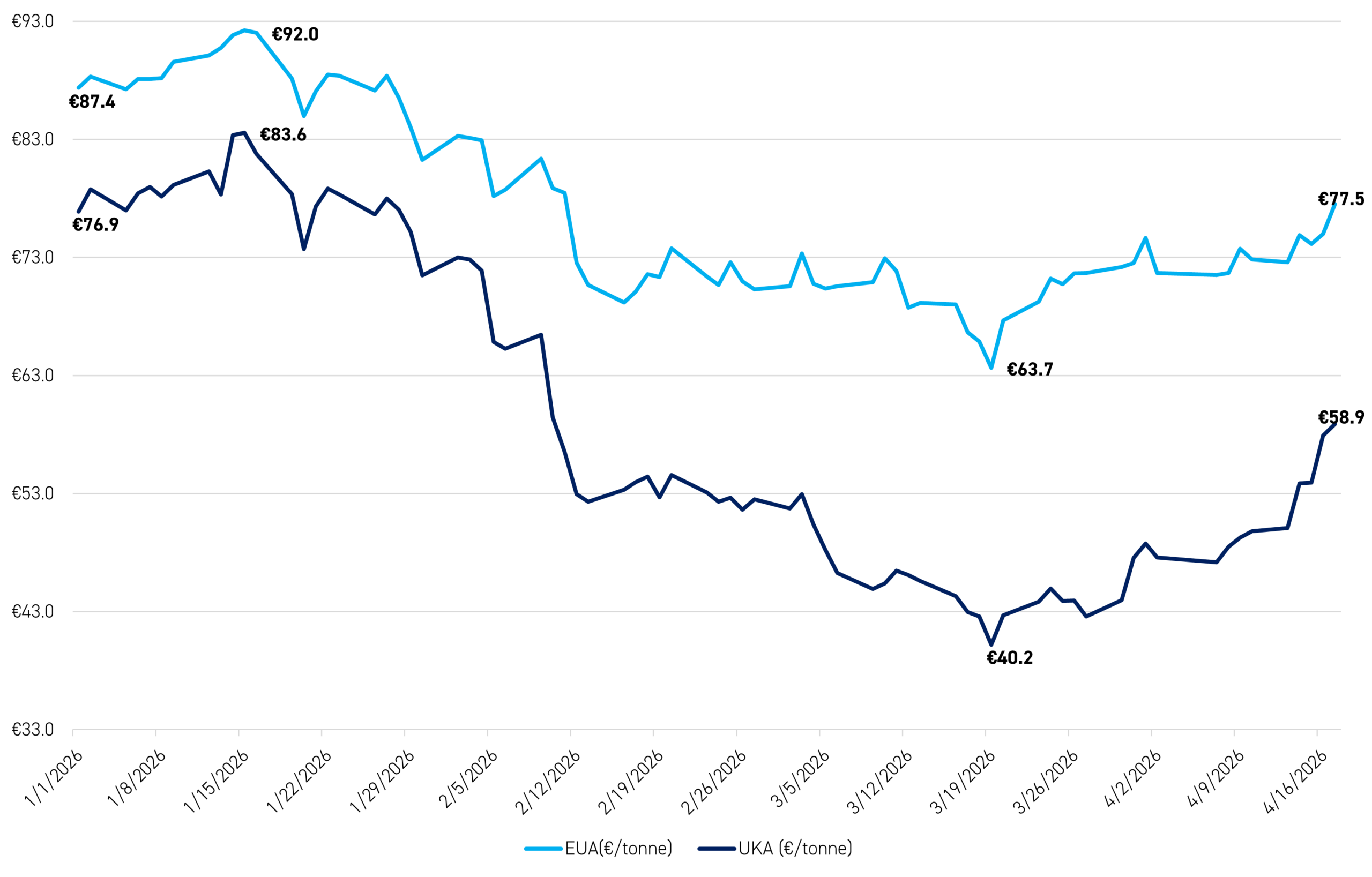

Figure 1 shows the price of the Dec-26 EUA contract versus the Dec-26 UKA contract since the beginning of this year. After narrowing over Q4 of last year, the UKA discount to EUAS had widened significantly again over the last three months, as a lack of newsflow on linking the UK-ETS with the EU-ETS had left investors fearing a slowdown in the political momentum on this issue. Last week, however, the UK announced that it would be scrapping its CPS from April 2028, and UKAs rose 6% on this news, reducing the discount to EUAs to €18/t as of COB Friday, down from the €29/t high of this year recorded on March 27.

Figure 1: Front-Dec EUA (LHS, €/t) versus Front-Dec UKA (RHS, €/t*) Jan 1 - April 17, 2026

Source: Bloomberg. *Note that we have converted UKA prices into €/tonne here for ease of comparison.

The reason UKAs bounced on this news is that the market interpreted it as a signal that the linking talks are on track. After all, if the UK Government is comfortable scrapping the CPS from April 2028, it can be read as a sign that it is confident that the UK-ETS will be formally linked with the EU-ETS by then, with full convergence of UKA prices with EUA prices also likely by that date if linking can indeed be achieved in accordance with this timeframe.

Meanwhile, EUAs are also ending the week higher, having benefitted from the prospects of a ceasefire between the US/Israel and Iran, and from the breaking news earlier Friday that Iran planned to reopen the Strait of Hormuz to all traffic, though this is coming into question this week. Oil has dropped sharply on this news – WTI and Brent are down 12% and 10% respectively Friday– and so too is the EU natural-gas benchmark, with the front-month Title Transfer Facility (TTF) contract dropping 7% on the news to close at €39.5/MWh Friday, its lowest level since 27 February, which was the last trading day before the conflict with Iran began. With EU policymakers extremely sensitive to the impact of high natural-gas and electricity prices on industrial competitiveness, EUAs have become inversely correlated to TTF and have therefore staged a relief rally Friday.

Clearly, however, the conflict between the US/Israel and Iran remains very tense, and any sign that the ceasefire is at risk and hence that kinetic hostilities might resume in the near term will continue to be a risk weighing on both EUAs and UKAs.

CARB releases amended ISOR, reaction so far muted, but constructive progress for approval process

In California, CARB released the much-anticipated amended ISOR on April 14, starting a 15-day public comment period to allow for feedback on the revisions. Importantly, the amended ISOR did not propose any changes to the California cap trajectory presented in the original ISOR, with the updated version still removing 118.3 million allowances from the 2027-2030 budget years, and the cap trajectory still declining to 30.3 million by 2045, in line with the Golden State’s long-term climate target. CARB's Rajinder Sahota made a point to emphasize the ambition of the tightening, nearly 3x steeper than current statutory reductions (~11% annual decline through 2030 and ~7% thereafter vs ~4% today).

The main focus of the modified ISOR was the introduction of the “Build Up California Reserve” account for the new Manufacturing Decarbonization Initiative (MDI). The MDI was first introduced in the original ISOR and is intended to minimize carbon leakage risk and thereby support the decarbonization of California’s manufacturing industry. The MDI provides additional free 'units' for eligible facilities that commit to undertaking specific on-site GHG emissions reductions (electrification, hydrogen fuel switching, CCUS), designed to support early-stage, capital-intensive projects amid federal policy pullbacks. These units effectively become allowances once they are awarded (used for compliance obligations and can be traded in the market), and are similar to price ceiling units in that they come from an additional reserve that can be drawn on if compliance entities qualify. While the original ISOR did not make explicit how many CCAs would be made available for the MDI, CARB did estimate that up to 40 million could be taken from future vintage years.

In the modified text, CARB created a new reserve and explicitly capped it at a 118.3M limit, which is the same as the cap reductions over the 2027-30 period and therefore caused confusion over what that meant for the market's supply dynamics. However, in a webinar following the release, Rajender noted that it's important to distinguish between the cap reductions being separate and unaffiliated from this reserve, and was chosen because it's a "familiar" number. Additionally, issuance is conditional on stringent verified project activity, so the full reserve is neither guaranteed nor expected to fully enter circulation. Projects that fail to deliver the expected reductions or allocated value not used for qualifying investment must be returned to CARB to be retired, unless redirected to another eligible project, effectively a “use-it-or-lose-it” structure.

The other main change in the amended ISOR was that CARB is now proposing a material increase in the number of free allowances to be allocated to industry, especially refiners. However, this will not have any bearing on overall supply and should therefore be price neutral. On the one hand, it will mean less hedging by industry, which might be considered bearish, but on the other, it will reduce liquidity, which could squeeze prices higher and might therefore be considered bullish. Moreover, while in the original ISOR, refiners were not eligible for the MDI, they have now been included in it in response to the public comments received. The post-2030 free allocation framework was also deferred to future rulemaking.

Following the release of the amended ISOR, CCAs remained near the floor-price support level, likely reflecting initial concern over how many of the 118M allowances to be removed might ultimately come back to market. As the market digests the changes and their potential impact on longer-term balances, however, we would expect to see CCA prices gradually rebound. Furthermore, and crucially, we now expect CARB to submit its proposed amendments to the Board meeting of May 28, as we do not expect CARB to make any further changes to the ISOR following the conclusion of the new 15-day comment period on April 29. Accordingly, we think CARB remains on track to implement the change from January 1 next year, thereby removing the risk of any further delays to the long-awaited tightening of the market.

Carbon Market Roundup

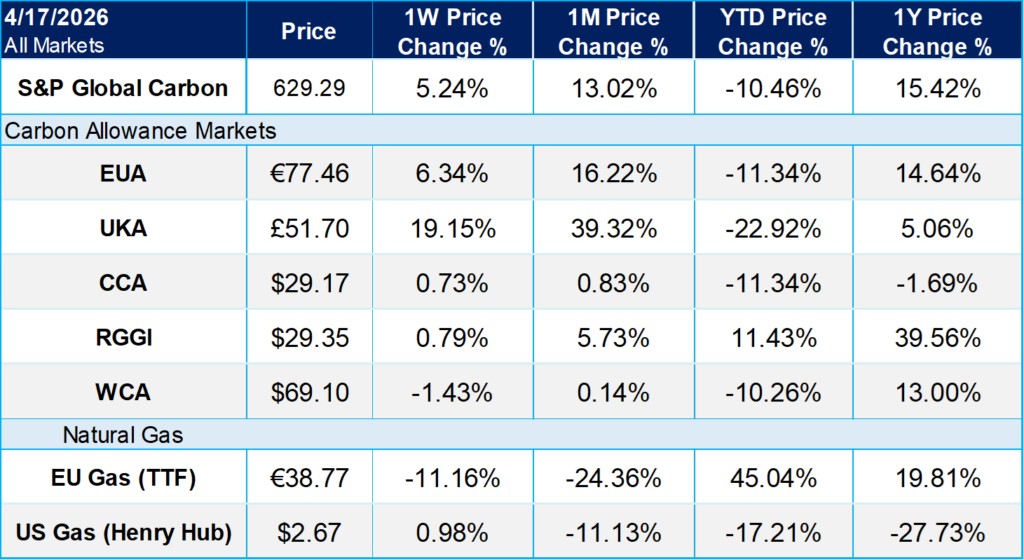

The weighted global price of carbon ended the week at $54.40, up 5.24% week over week. EUAs rose to €77.46, gaining 6.34% on the week, while UKAs jumped to £51.70, up 19.15%. In North America, CCA prices edged higher to $29.17, up 0.73%, and RGGI allowances increased to $29.35, up 0.79%. WCA was the only major carbon benchmark to ease, finishing at $69.10, down 1.43% over the period.