CCAs Boosted by Rulemaking Board Notice, Washington Q1 Reserve Auction Attracts Strong Interest

By Mark Lewis & Climate Finance Partners LLC (CLIFI)

4 Min. Read Time

With EUAs and UKAs holding within their recent trading ranges (see May 15 blog), US carbon markets are stealing the limelight this week. CCAs await the rulemaking approval vote at the May 28 Board meeting, the Northeast power market (RGGI) continues to trade near its recent all-time highs, and Washington’s additional reserve (APCR) auction saw strong interest for the limited volume on offer.

Big week ahead for CCAs with Q2-auction results on May 27, CARB Board meeting May 28

As highlighted in last week’s blog, the CCA market had been in a holding pattern over the last few weeks while participants waited to see whether the regulator, the California Air Resources Board (CARB), would propose any further changes to the reform package, currently published as proposals under the Initial Statement of Reasons (ISOR) document, following the completion of the 15-day consultation period for its updated version.

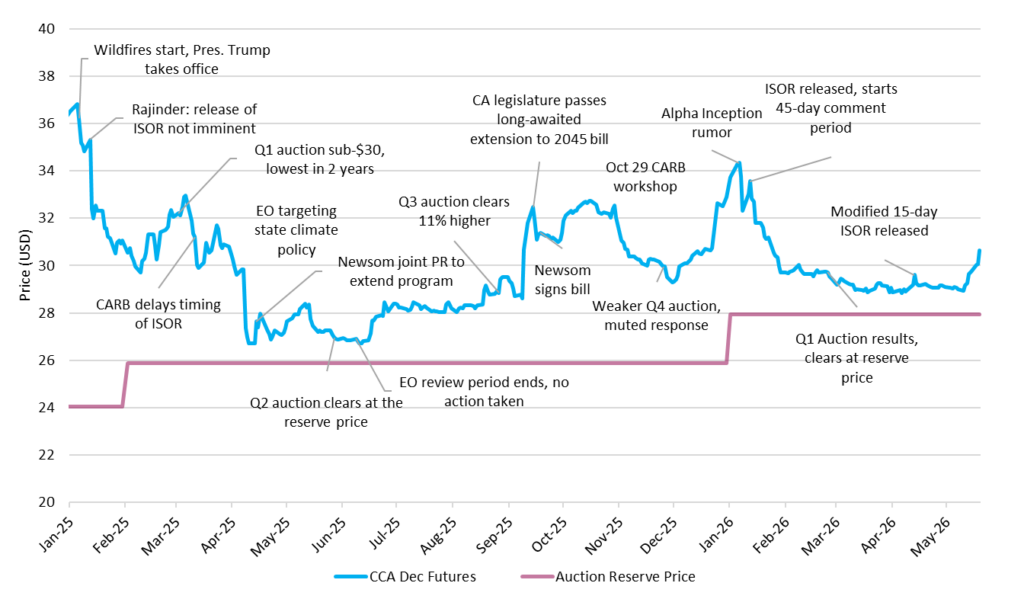

Following confirmation of the rulemaking vote on May 28 in CARB's notice posted last Friday evening, CCAs broke out of their tight trading range, pushing above the psychological $30 level and the 100-day moving average at $29.98. We expect the Board to approve the package and instruct CARB to publish guidance on the Manufacturing Decarbonization Initiative (MDI) program to address stakeholder concerns over the newly proposed reserve of additional allowances that awards credits for investments in early-stage, capital-intensive decarbonization projects. If all stays on track, the market amendments will take effect on January 1, 2027.

CCAs closed at $30.64/t on May 20, up 4.8% on the week since May 13, and up 5% from the YTD closing low of $28.90/t last seen on May 11 (Figure 1).

Figure 1: Dec-26 CCA contract, January 1, 2025 – May 20, 2026 ($/t)

In addition to the positive sentiment created by the publication of the CARB board agenda, CCAs were also boosted by the April US Consumer Price Index (CPI) reading, which came in at a three-year high of 3.8%, and could mean a higher 2027 reserve price if this rate persists. The market's reserve price, which serves as a downside floor level at auctions, rises by 5% plus CPI annually. Using the latest inflation print, the 2027 reserve price rises to $30.40/t up from $27.94 this year. Over the two days following the inflation release, trading volumes in CCA were noticeably higher than usual (34m in the week ending May 15 compared with 9.5m in the week to May 8).

We expect this positive momentum to translate into a higher settlement price at the Q2-WCI auction held on Wednesday, compared with recent auctions, likely seeing it fully subscribed in a settlement range of $28.5-30/t, with results due on May 27.

RGGI continues to trade near its All-time-highs

As explained in our blog on May 1, Regional Greenhouse Gas Initiative Allowances (RGAs), which cover the power sector across 10 Northeastern US states, have been very strong following confirmation that Virginia will be re-admitted into the RGGI program from July 1. The Dec-26 contract closed on May 19 at $43.18/short ton, up 63% YTD.

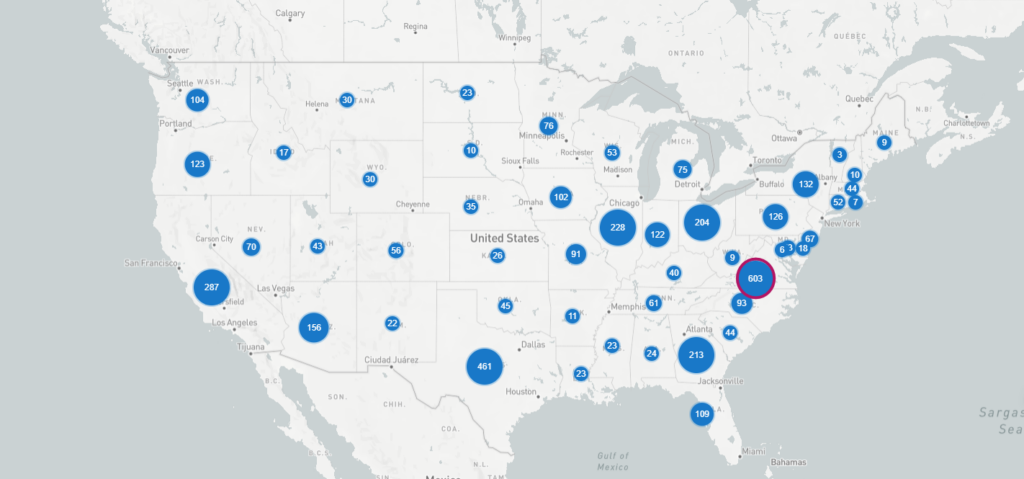

Viringia's inclusion is influential because the state is dominating the data center boom, which is driving outsized energy demand at a rate much faster than in other RGGI states. According to Veyt, Virginia alone could double power demand within RGGI by 2040. Currently, New York is the highest-emitting state, but Virginia comes in as a close second and could easily overtake the top spot depending on where its growing energy uptake is sourced. Unlike California's market, RGGI does not include imported energy, which adds an additional nuance for Virginia, a PJM* power market member that imports power from non-RGGI states.

Figure 2: Number of Data Centers by State

With over 600 data centers in the state, Virginia dominates the space relative to the rest of the country, with Texas second at ~450.

As we noted in last week’s blog, this continued price strength comes despite RGGI Inc.'s May 8 statement cautioning that current high RGA prices might require further cost-protection measures for consumers, yet current RGGI regulations provide no mechanism for direct intervention outside of the already depleted Cost Containment Reserve (CCR). The CCR consists of a quantity of allowances in addition to the cap, held in a reserve account and released to the market only when a certain trigger price is reached at the auctions (i.e., $18.22 in 2026).

Auction settlements have consistently exceeded the CCR trigger since March 2024 without any action being taken by the regulator. While the new Model Rule currently being adopted by RGGI states will expand this cost-containment mechanism into a two-tiered measure rather than a single level for 2027, it is not clear what measures RGGI Inc. could take this year to control prices. RGAs are already trading above both 2027 CCR tier levels of $19.50 and $29.25, respectively.

As a result, we expect RGAs to remain elevated in the near term, with compliance players having to cover their shortfall this year not only from primary auction supply but also from existing speculative holdings. The Q2-RGGI auction will take place on June 1, and we expect strong compliance interest.

Washington’s Q2-APCR auction attracts strong interest, WCAs anchored at the APCR level

Washington May 2026 Allowance Price Containment Reserve (APCR) auction (serves a similar function to RGGI's CCR mechanism) saw the full number of allowances on offer this quarter – 129,262 WCAs out of a total 2026 pool of 646,310 allowances – sold at the Tier-1 APCR price of $65.26/t. The 13 compliance entities that qualified for the auction included large refiners, power generators, and smaller covered entities. The cover ratio was very strong at 7.79x, driven by the small volumes on offer.

We expect the remaining regular quarterly WCA auctions this year to settle at or above the Tier-1 APCR trigger price of $65.26/t, which would trigger the residual 517k WCAs from the 2026 APCR pool to be auctioned over the rest of the year and in Q1-2027.

The next regular quarterly Washington auction will be held on June 3.

Carbon Market Roundup

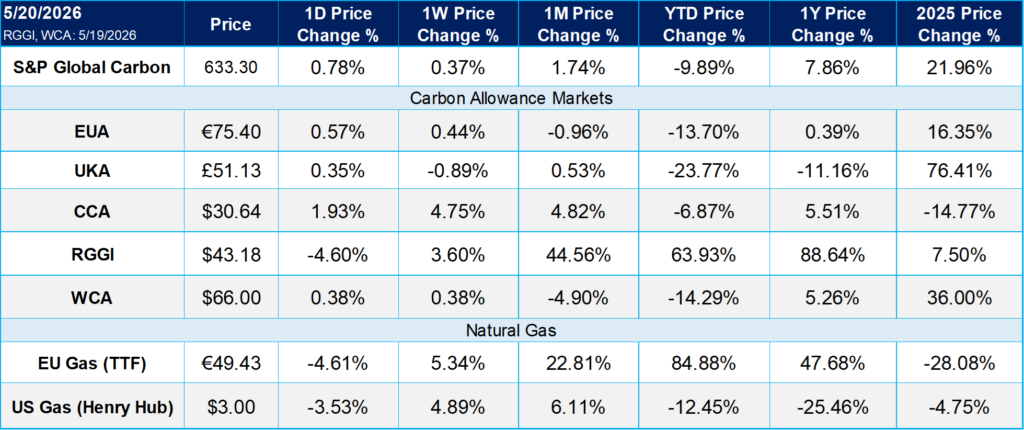

The weighted global carbon price closed at $54.75 up 0.37% week-over-week. EUAs ended at €75.40, up 0.44% week-on-week, while UKAs closed at £51.13, down 0.89%. In North America, CCA prices rose to $30.64, up 4.75%, and RGGI allowances advanced to $43.18, up 3.60%. WCA finished at $66.00, also higher by 0.38% over the week.

*PJM: Pennsylvania-New Jersey-Maryland, the largest power grid operator in the United States, which expanded its coverage from its original three states to now serve 13 states in the mid-Atlantic and Midwest area.