Moment of Truth for EU-ETS This Week, US Markets Remain Stable

By Mark Lewis & Climate Finance Partners LLC (CLIFI)

9 Min. Read Time

This coming Friday, July 17, the European Commission will launch the long-awaited EU-ETS Review, a process that will run for the following 12-18 months and that will decide the operational and pricing parameters of the world’s largest carbon market for the next decade and beyond. While the market already has a good idea of where the main elements of the review are likely to land, media reports at the end of last week indicate that there may still be surprises in store in some key areas. Meanwhile, US markets have been stable over the last couple of weeks, with CCAs steadily trending higher, and RGAs and WCAs holding steady at recent levels.

European Commission poised to launch EU-ETS Review: where are we now, just 3 days out?

We set out our expectations for the EU-ETS Review in our Carbon Crunch blogpost of June 23, identifying five key areas that will be crucial to determining the future of the EU carbon market’s supply/demand balances over the next decade. However, last week saw a flurry of media stories on these key areas that, if substantiated when the Commission makes its announcement on Friday, could change our assumptions and hence our expectations for future S/D balances.

In particular, we see two variables out of the five that we identified in Carbon Crunch that would have major implications for our modeling of EU-ETS fundamentals over 2028-30 if last week’s media reports regarding the Commission’s latest thinking on these points prove accurate. These variables are: 1) the so-called Investment Booster, which is designed to channel €30bn to European industry for decarbonization investments; 2) the Total Number of Allowances in Circulation (TNAC) threshold level at which the Market Stability Reserve (MSR) ceases to remove allowances from auction volumes.

A reminder of our current base-case modeling

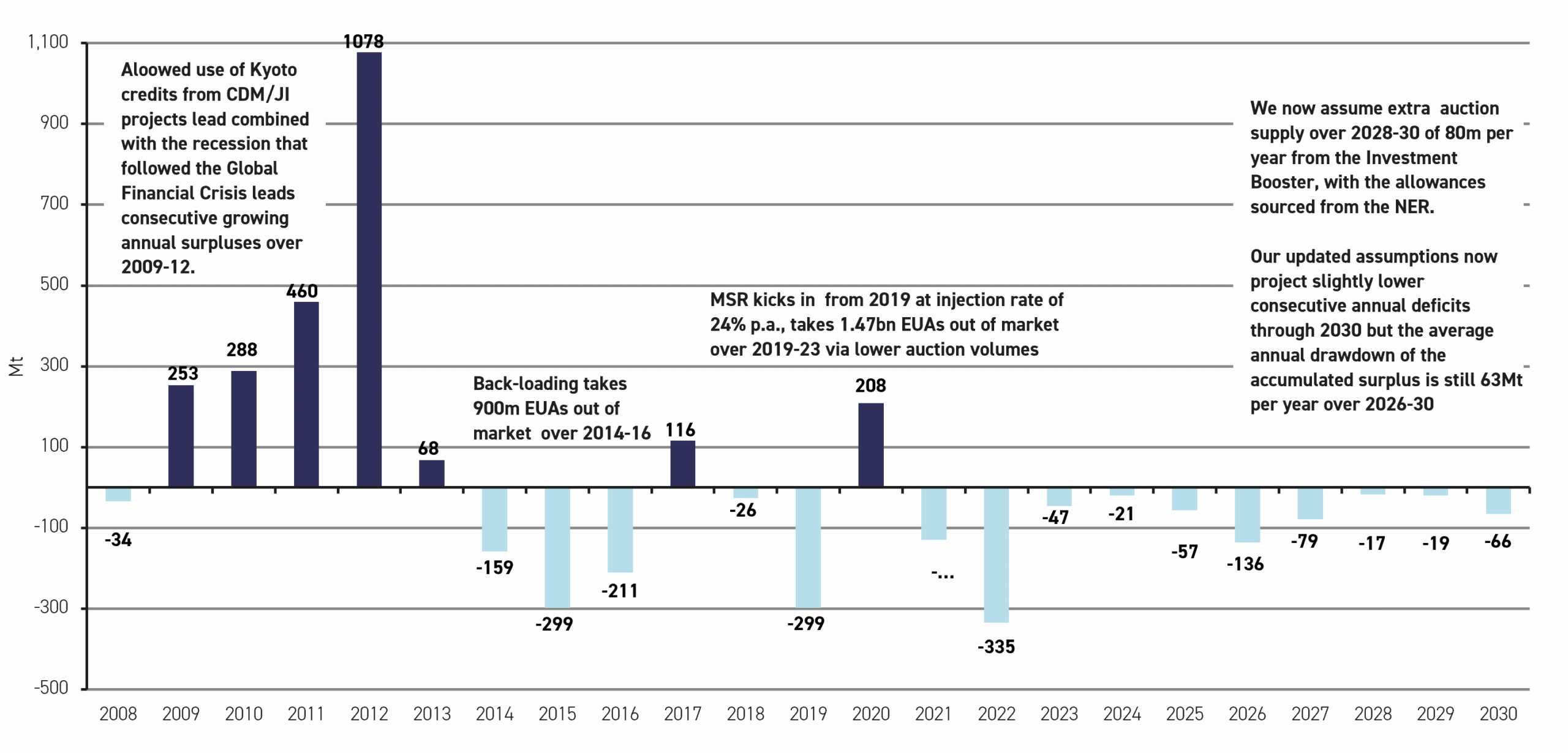

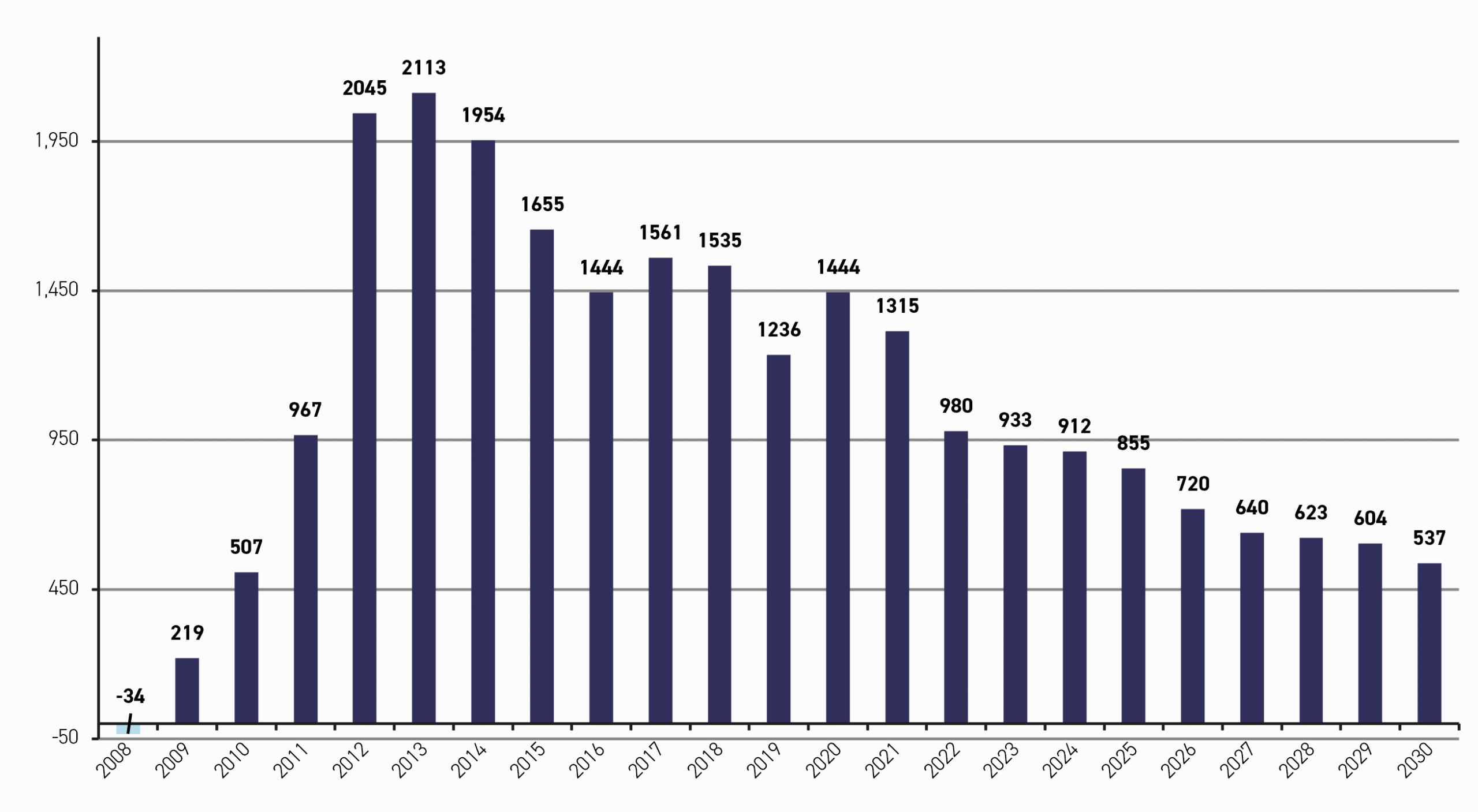

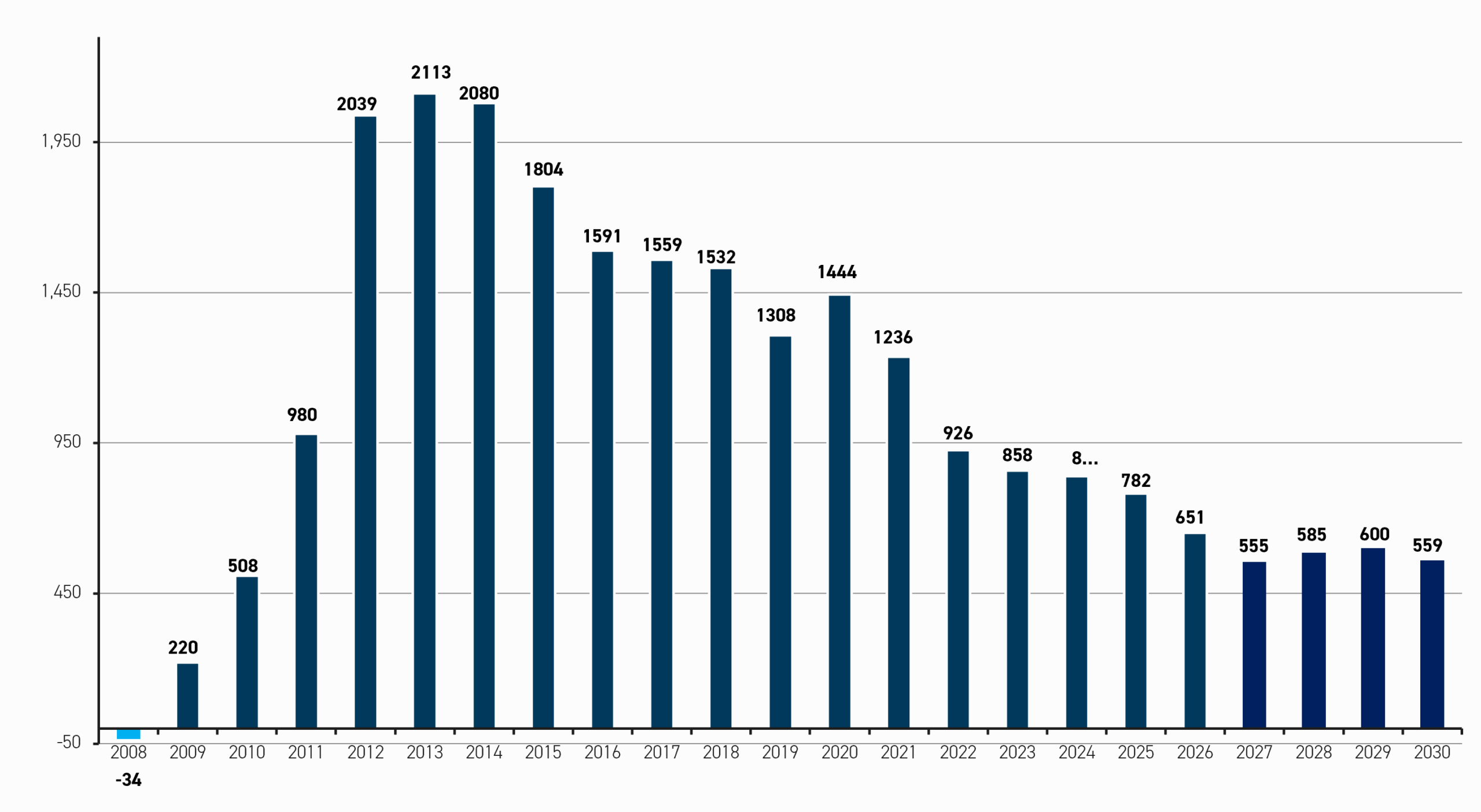

Before examining the implications of the latest media stories on these points, it is useful to remind ourselves of the assumptions behind our current base-case forecasts as set out in our Carbon Crunch blogpost. Figure 1 shows our current base-case projections for the annual balances through 2030, and Figure 2 shows our current base-case projected reduction in the total surplus of allowances accumulated since 2008 (i.e., with the full cumulative aviation deficit included from 2012).

Figure 1: CLIFI current base-case EU-ETS annual S/D balances, 2008-30 (Mt)

Source: European Commission, CLIFI

As can be seen, our modeling projects consecutive annual deficits over 2026-30 (Figure 1) such that the system-wide cumulative surplus falls by 317Mt over this period to reach 537Mt by the end of 2030 (Figure 2).

Figure 2: CLIFI current base-case cumulative system-wide* EU-ETS surplus (total TNAC), 2008-30 (Mt)

Source: European Commission, CLIFI; *This number differs from the TNAC published by the European Commission every year in that it includes the cumulative Aviation balance from 2012, not just from 2024. This explains why this system-wide cumulative-surplus number is 180Mt lower than the TNAC published by the European Commission.

The key assumptions underlying our current base-case projections are that the 400m allowances that we already know will be used to fund the €30bn investment booster will be auctioned over the five years 2028-32 at a rate of 80m per year, and that the EU-ETS Review will not propose any change to either the method for calculating the TNAC or the MSR intake and release thresholds.

Latest media reports on the Commission’s intended proposals

In a story published on July 8, Bloomberg reported that the Commission will now propose disbursing the 400m allowances for the Investment Booster over only three years instead of the five that we are assuming, and that these allowances will be allocated for free instead of being auctioned. If true, this raises the prospect of 133m allowances being added to the free-allocation volumes over 2028-30, which would mean an extra 53m allowances per year of total supply over this period, above and beyond what we are already assuming in our current modeling (as shown in Figure 1, we assume 80m EUAs per year are auctioned over 2028-30). The Bloomberg report also stated that the Commission would make €6bn worth of extra allowances available for free allocation to energy-intensive industry to soften the heat and fuel fallback benchmarks (our current base case assumes €4bn).

Secondly, reports on the carbon newswire site, Carbon Pulse, last week suggested that the Commission will change the way it calculates the TNAC to include the cumulative deficit of Aviation from 2012, as opposed to the current calculation, which only includes the Aviation balance from 2024. In our view, this would be a positive move as it would bring the market supply (TNAC), as calculated by the Commission every year, for the purposes of determining the volumes to be placed in the MSR, into line with the actual TNAC in reality.

This is because the actual system-wide TNAC is approximately 180Mt lower than the TNAC as calculated by the Commission, with this 180Mt discrepancy being the cumulative deficit of Aviation over 2012-23, which is currently excluded from the Commission’s calculation.

This is important because what matters to the market is the true level of inventory outstanding in the market, so including the cumulative Aviation deficit in the TNAC calculation would increase transparency and avoid confusion. That is why we always show the outstanding inventory in the market, including the cumulative Aviation deficit from 2012, as per Figure 2 above.

At the same time, media reports last week also suggested that the Commission would lower the threshold at which the MSR stops withholding allowances from the market to 650m from the current 833m. The Market Stability Reserve (MSR) is the EU ETS’s supply-management mechanism that automatically adjusts the total number of allowances in the market based on the overall market surplus, helping prevent excessive oversupply and stabilize carbon prices. Reducing the upper MSR threshold to 650m while at the same time changing the TNAC calculation to include the cumulative Aviation deficit would mean no change in practice to the point in time at which the MSR would stop withholding auction volumes from the market as it would simply mean that the upper MSR threshold is adjusted by almost exactly the same amount as the TNAC, i.e. 180Mt (833m-650m =183m).

Scenario analysis: what would the impact on our S/D balances over 2028-30 be?

The key question for our modeling purposes here concerns the impact of changing the rate at which the Investment Booster’s 400m allowances are disbursed to three years instead of five. Of course, if this is what the Commission does in fact propose on Friday, and if this were ultimately agreed to by the EU Council and EU Parliament, there is still the question of how this would happen in practice, as there would have to be conditionality guardrails on the free allocation of these allowances tied to commitments for investments in industrial decarbonization, and then there would be all the bureaucratic bandwidth required to ensure these conditionality guardrails were being met.

It is therefore much more difficult to model the allocation of free allowances from the Investment Booster than it is to model the auctioning of the same volumes. This is because we cannot know in advance either how much demand there will be for free allowances conditional upon decarbonization commitments or how much of this demand would meet the eligibility criteria. By contrast, once we know what the volume of allowances to be auctioned over a given timeframe is, it is simply a mechanical exercise to plug those numbers into a model.

At this stage, we think it is very unlikely that 400m allowances will end up being allocated for free from the Investment Booster over 2028-30 in practice, even if this is what ends up being proposed by the Commission and agreed to by Council and Parliament. This is because it is hard to imagine that there would be sufficient demand that could meet the eligibility criteria in such a short space of time (note, though, that we do not even know yet what the eligibility criteria would be).

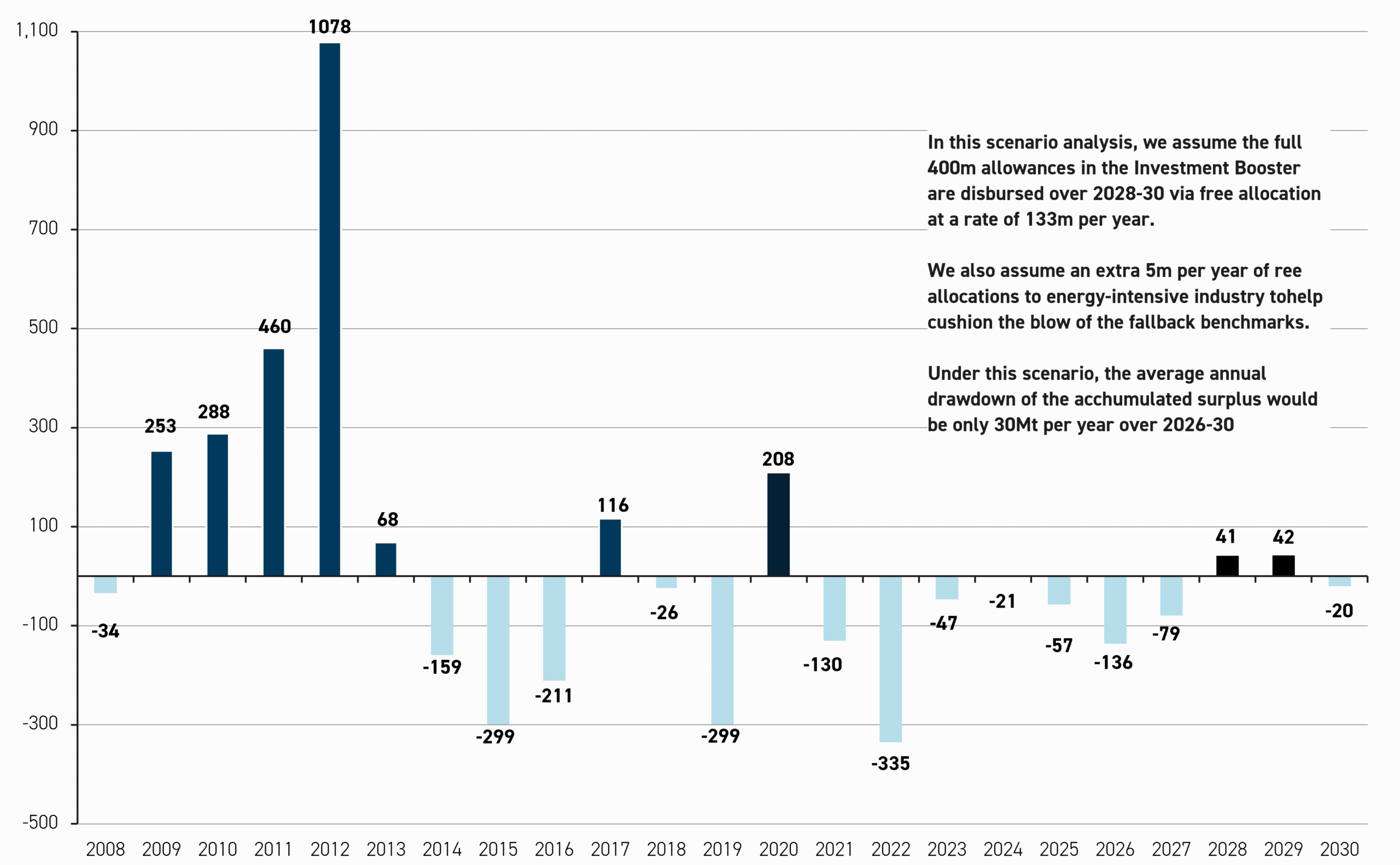

Nonetheless, as a thought exercise, we have modeled how the S/D balances would change if 400m allowances were indeed to end up being disbursed for free by the Investment Booster over 2028-30 (Figure 3) as a worst-case scenario in terms of the magnitude of the supply increase.

Figure 3: CLIFI scenario analysis of potential EU Commission proposals under EU-ETS Review and their impact on EU-ETS annual S/D balances through 2030 (Mt)

Source: CLIFI

At the same time, we have also included in this exercise how a change to the TNAC calculation to include the cumulative Aviation deficit from 2012 and a reduction in the upper MSR threshold to 650m would alter the annual S/D dynamics over 2028-30. And we have also increased the assumed volumes of free allocations to energy-intensive industrial companies to €6bn from €4bn over 2028-30, resulting in an extra 5m allowances of supply per year over this period.

Putting all of this together, we get the S/D balances shown in Figure 3, and the trend in the total TNAC – i.e., including the cumulative Aviation deficit from 2012 – shown in Figure 4 (as such, Figure 4 here is directly comparable with Figure 2 above in that both show the total underlying TNAC after including Aviation balances from 2012).

Figure 4: CLIFI scenario analysis of potential EU Commission proposals under EU-ETS Review and their impact on the EU-ETS surplus (total TNAC) through 2030 (Mt)

Source: CLIFI

Comparing Figure 3 with Figure 1 and Figure 4 with Figure 2, we can gauge the impact of the Commission’s proposals – should they come out as reported – on the S/D dynamics of the EU-ETS through 2030. The headline difference is that the annual consecutive deficits over the five years 2028-30 seen in Figure 1 are interrupted by surpluses in 2028 and 2029 in Figure 3, while the deficit in 2030 is lower under our scenario analysis than under our current base case (-20Mt versus -66Mt, respectively).

This means that the cumulative deficit over 2026-30 under our scenario analysis would fall to only 152Mt versus 317Mt in our current base case, and that the total TNAC would therefore stand at 703Mt in 2030 versus only 537Mt in our current base case.

Conclusion: even the worst-case scenario from the EU-ETS Review would be manageable

If recent media reports prove correct and the Commission proposes to add the full 400m of supply envisaged under the Investment booster over 2028-30 via free allocation – and assuming such a scenario were even technically feasible given the logistical challenges it would present – we think our modelling shown in Figures 3 and 4 gives a realistic indication of what the impact would be (assuming the Commission’s proposals were also then accepted by Council and Parliament).

Undoubtedly, the increase in supply this would entail would loosen the balances over 2028-30, and on our projections, it would reduce the cumulative deficit over the five years 2026-30 by 165Mt (317Mt in our base case versus 152Mt in our scenario analysis). Nonetheless, the fundamental integrity of the system would be upheld, as the total TNAC would still fall by 20% over the period, while the political sustainability of the EU-ETS would be reinforced.

Moreover, we would emphasize that this is very much a worst-case scenario, as in reality, we do not think that it will be technically possible to allocate 400m allowances before 2030 for free, given the conditionality safeguards and supervisory infrastructure that would be required to ensure the eligibility criteria are met.

Accordingly, we continue to think our existing base-case scenario – which assumes 240m of the total 400m available under the Investment Booster comes to market over 2028-30 – remains a more reasonable estimate of the likely practical reality, whatever the Commission proposes on Friday. It is nonetheless reassuring to know that the worst-case scenario would not be such a negative outcome for the market as might be feared.

Indeed, this seems to be what the market itself has concluded, with EUAs trading at time of writing today at €80/t versus a close of €79.04/t on July 8 after the Bloomberg story first broke. Let us now wait and see what Friday brings.

US markets remain stable, CCAs steadily chasing Jan high

In California, CARB is aiming to implement the reform package by September 1, and in order to meet this timeframe, it must submit the Final Statement of Reason (FSOR) document to the Office of Administrative Law (OAL) for final review. Given that the OAL has 30 working days to evaluate the FSOR, then CARB would need to submit it by the week of July 20 to meet its targeted implementation deadline, and we would therefore expect the FSOR to be published in the coming days.

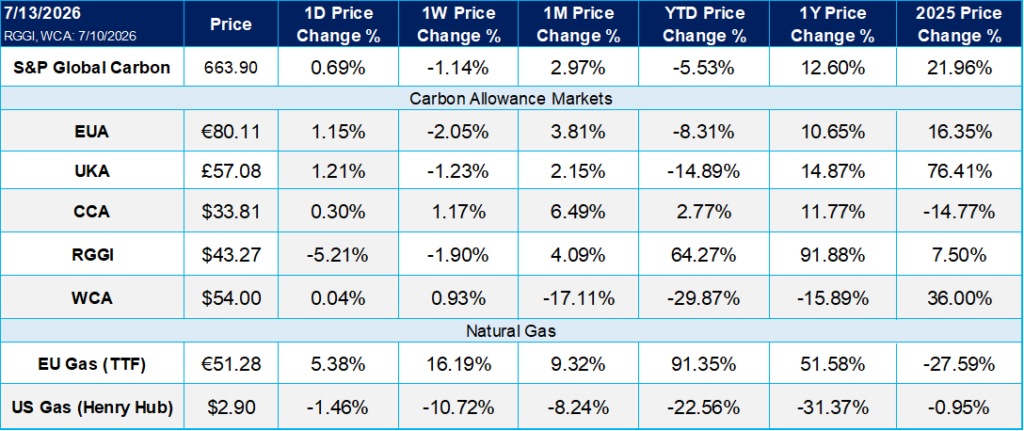

Carbon Market Roundup

The weighted global price of cabron drifted lower over the week to $58.70, down 1.14%. EUAs fell to €80.11, down 2.05% week over week, while UKAs slipped to £57.08, down 1.23%. In North America, CCA prices rose to $33.81, up 1.17%, while RGGI allowances declined to $43.27, down 1.90%. WCA also moved higher to $54.00, up 0.93% over the period.