CCAs Await CARB Board Meeting, EU Publishes Free Allocation Benchmarks

By Mark Lewis & Climate Finance Partners LLC (CLIFI)

4 Min. Read Time

EUAs and UKAs remain within their trading ranges of the last month, while CCAs move modestly higher ahead of the upcoming CARB Board meeting on May 28 and the release of meeting materials today. Meanwhile, RGAs continue to trade near their recent all-time highs.

EUAs and UKAs stuck in recent trading range, linking remains on track

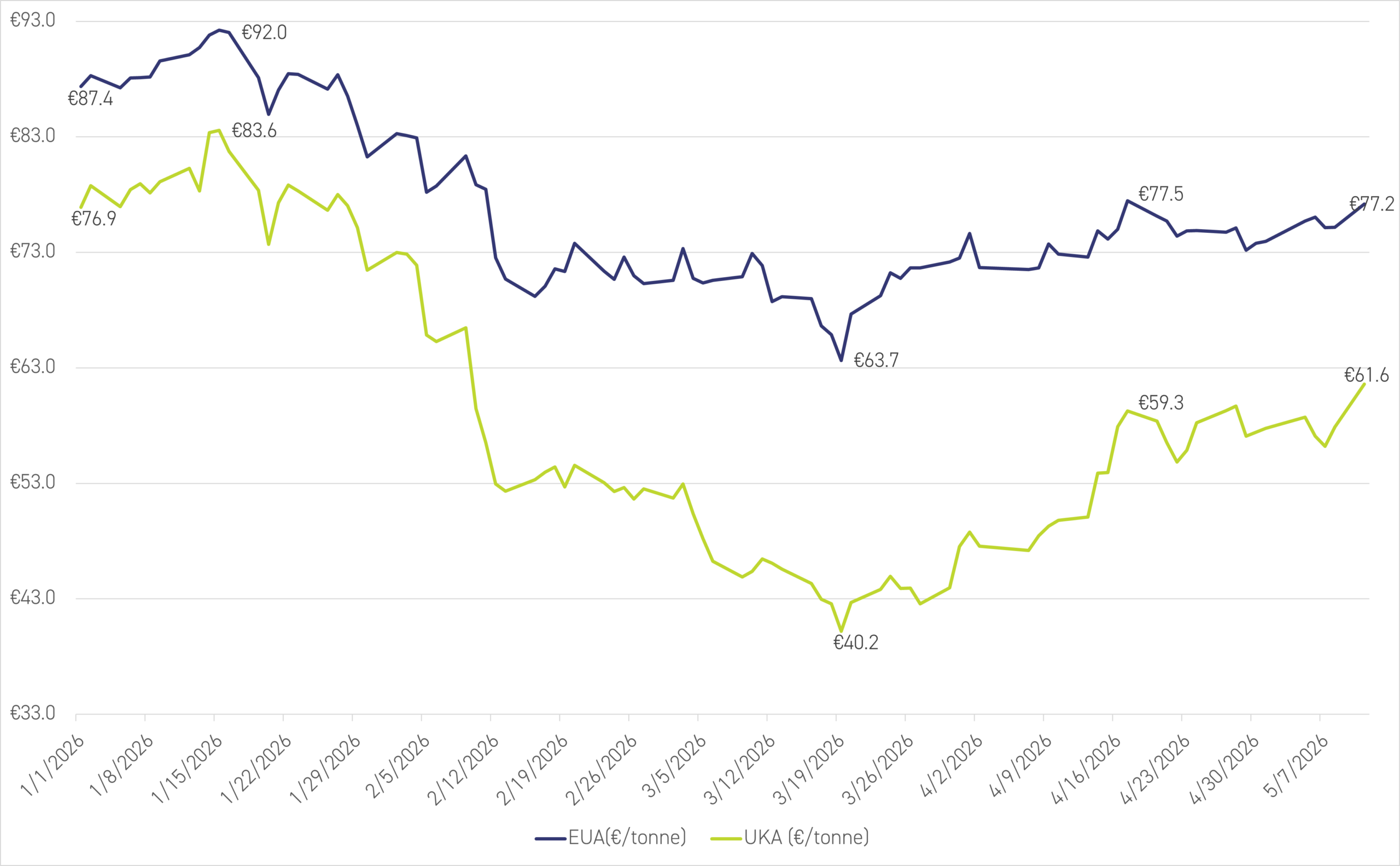

Figure 1 shows the price of the Dec-26 EUA and UKA contracts since the beginning of this year. Both markets have remained within their respective trading ranges over the last month – €73-€77.5 for EUAs, and a wider £42-£52 for UKAs – reflecting a more stable EU natural-gas price1 owing to the ongoing but still fragile ceasefire between the US and Iran and less background noise from policymakers as the market now awaits the launch of the EU-ETS Review in July.

Figure 1: Dec-26 EUA versus Dec-26 UKA, January 1 – May 11, 2026 (€/tonne)*

Source: Bloomberg; * UKAs converted into €/t for ease of comparison

On Monday, May 11, the European Commission published its updated benchmarks for free allocation to industry, which came in at the tighter end of expectations (marginally bullish), while earlier in the week, it was announced that an extra 50m EUAs would be auctioned in 2026 than previously expected (marginally bearish) in order to fund the social cohesion fund for the ETS-2.

As long as the US/Iran conflict remains deadlocked in a ceasefire, we would expect EUAs to continue treading water over the next few weeks ahead of the launch of the EU-ETS Review in July. We see scope for UKAs to creep up over the next few weeks, thereby narrowing the discount to EUAs, in expectation of a formal announcement by the UK and EU at some point in July that they have reached a formal agreement to link their carbon markets. Despite the political uncertainty in the UK at the moment over the position of Prime Minister Keir Starmer, we think that, should he be replaced from within the ruling Labor Party, any of the likely candidates to succeed him would be equally enthusiastic about pursuing closer links with the EU, including the formal linking of the UK-ETS with the EU-ETS.

California awaits May 28 CARB Board meeting, RGAs continue to feel boost from Virginia

CCAs continue to trade close to the floor price, with the Dec-26 contract settling yesterday at $29.53/t, as the market awaits the publication of the agenda for the May 28 CARB meeting, which should be posted on Monday (May 18). Ten days prior to the meeting, CARB is required to publish meeting materials for the Board meeting, which should give better insight into how they've responded to the most recent 15-day public comment period. There was some pushback from certain legislators calling for more ambitious measures, specifically that the MDI provisions in the updated ISOR are too generous to industry and would cause fiscal problems for the state by reducing auction revenues through additional free allowances. Some legislators have even voiced concern that if passed, the MDI provisions would necessitate a re-opening of state budget negotiations with the Governor, arguing that the MDI provisions in the updated ISOR should therefore be looked at again. However, CARB appears to be holding the line that a May 28 vote is essential for respecting the implementation timeframe.

There are a lot of uncertainties regarding the number of allowances that will ultimately come to market over the 2028-35 period from the MDI, as set out in the updated ISOR, not least as the Cap Adjustment Factors (CAFs) for the 2031-35 period have not been set yet. As a result, we are currently thinking about different scenarios pending CARB's response to the most recently concluded 15-day consultation period on the revised ISOR. We don't expect CARB to make material changes going forward, as it's crucial that the regulator sticks to the May 28 timeline and instead publishes additional guidelines on how they plan to monitor the integrity of the MDI program.

As a result, Monday’s meeting agenda and materials release should provide further clarity and market support. We will provide updates as they come.

Meanwhile, as explained in our blog post of May 1, RGAs have been very strong following confirmation that Virginia will be re-admitted into the RGGI program from July 1. The Dec-26 contract closed Thursday at $45.35, up 72% YTD, making RGAs by far the best-performing carbon instrument in the world so far this year.

Moreover, this continuing price strength comes despite the publication on May 8 by RGGI Inc of a statement cautioning that current high RGA prices might require further cost-protection measures for consumers. The key paragraph in the statement reads as follows:

Recent futures prices are above thresholds established to automatically mitigate price growth by releasing additional allowances at auctions for cost containment. RGGI has a long history of stability. Regular program reviews have made adjustments to align the program with policy objectives of a reliable, affordable, and clean electricity supply. A sustained period of elevated auction prices would not meet these objectives and may require renewed consideration of improvements.

The forthcoming Q2 RGGI auction on June 1 will therefore be a very interesting first test of this statement.

Carbon Market Roundup

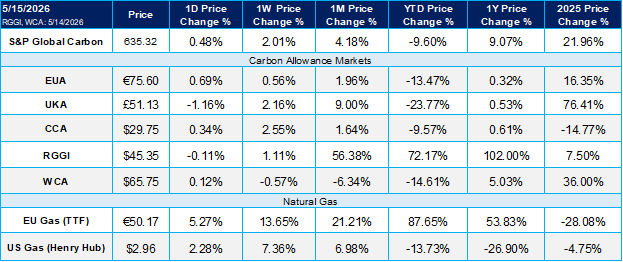

The weighted global price of carbon ended the week higher, closing at $54.92, up 2.01%. EUAs were little changed at €75.60, up 0.56%, while UKAs climbed to £51.13, up 2.16%. In North America, CCA prices closed at $29.75, gaining 2.55%, and RGGI allowances settled at $45.35, up 1.11%. WCA eased to $65.75, down -0.57% over the period.