CCA Reform Package Approved at Board Meeting, EUAs React to New Low-Carbon Investment Tool

5 Min. Read Time

Last Friday, the California Air Resources Board (CARB) approved the regulatory reform package contained in the revised Initial Statement of Reasons (ISOR), a significant moment in the history of the Golden State’s Cap-and-Invest program. We think this now paves the way for CCAs to continue their recent steady upward trend over the next 12-18 months.

In Europe, both EUAs and UKAs have fallen back after last week’s rally, with a Bloomberg story on the planned sale of 400m EUAs to fund €30bn of industrial decarbonization prompting initial concern yesterday – overdone in our view – that the market could see extra supply coming to market in the near term.

With CARB Board’s approval of reform package, CCAs can put regulatory risk behind them

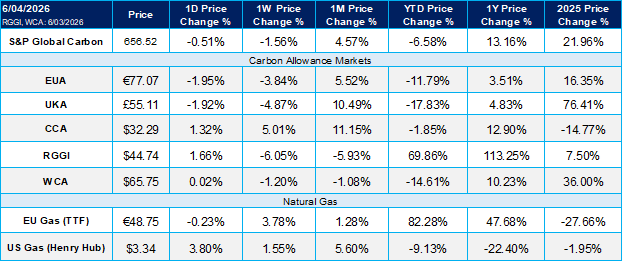

After the CARB Board approved the reform package for California’s Cap-and-Invest program on May 29, CCAs have continued to move higher, with the benchmark Dec-26 contract closing last night at $32.29/t, up 5% on their settlement price a week prior and now up 11% over the month.

The ongoing bullish sentiment reflects the adoption of the regulatory package, with the reform passing with a 10-3 vote by the CARB Board. Under the terms of the adoption, CARB is now required to develop further guidance concerning the Manufacturing Decarbonization Initiative (MDI), such as providing full transparency on MDI applications, the tracking of MDI allowances, and annual updates on MDI issuances and retirements. CARB will also have to reveal the progress of MDI-funded projects towards their projected emissions reductions. Moreover, CARB may propose additional changes to the MDI program before MDI allowances are distributed.

We expect 30 million CCAs from the MDI pool to be distributed over the 2028-30 period, and then a further 40m over 2031-35 period, totalling 70m MDI allowances from the overall MDI budget of 118m.

This means we expect the WCI bank of allowances to be depleted by 2033, one year later than in our modeling of the original ISOR. This means we now project a structural deficit in the WCI market by the end of 2033 of -37Mt, while under a scenario of the full 118m coming back to market over 2028-35 the cumulative deficit by the end of 2033 would be only -1Mt. Overall, while the MDI in the revised ISOR approved in the reform package at the CARB Board meeting last week will increase allowance supply versus the original ISOR, the declining cap and supply adjustments for offset usage should still lead to a broad decline in the WCI bank over the forecasting period.

And while the softer Cap Adjustment Factors (CAFs) and increased free allocations versus the original ISOR will reduce compliance demand through 2030, we think speculative demand could take up the slack as the fundamental S/D balance equation has not been dramatically altered. We think there will also likely be increased speculative interest in CCAs in 2027 as the prospects for linking the Washington market with the WCI come into sharper focus, which would add tightness to WCI balances at the margin.

The Board's adoption of the reform package is a very significant moment in the evolution of California’s ETS, and removes the regulatory risk that has been hanging over CCAs for the last two years. The package will now be sent to the Department of Finance for fiscal estimates, which could take up to 3 months. After that, CARB will submit the package to the California Office of Administrative Law (OAL), a process that can take up to 30 days. Overall, we think the way is now clear for CCAs to start trending structurally higher over the next 12-18 months.

Meanwhile, in the RGGI market, the results of the Q2-2026 auction were released this morning, with the price settling at a new ATH of $35/short ton. This represents a 40% premium versus the Q1 auction settlement of $24.99, but a 21% discount to the spot price on auction day of $44.51, with the auction's cover ratio falling to 2.4 from 3.3 in Q1. This suggests prices may have peaked for now and that a correction is due in the secondary market.

After breaking above €80/t last week, EUAs fall back

European Union allowances (EUAs) closed last night down 4.5% so far this week at €77.07/t, with UKAs also tracking lower and down 6% at £55.1/t. A Bloomberg story yesterday (EU Designs €30 Billion Carbon Market Tool to Avoid Permit Deluge) referencing the 400m allowances that the EU plans to sell in order to fund €30bn of low-carbon industrial investment appeared to spook the market, with EUAs down nearly €2/t in the morning.

The idea of the 400m allowance/€30bn investment booster was not new information to the market – it was actually formally proposed at the EU Council meeting in March – but the key questions are where the allowances will be taken from and over what period they will be sold to the market.

On the first of these questions, the Bloomberg article stated that the 400m allowances would come from the New Entrant Reserve and the reserve buffer of free allowances (totalling 3% of the Phase-4 cap) that was set aside at the beginning of Phase-4:

“The details of the new ETS-based instrument will be outlined when the EU unveils a review of its flagship cap-and-trade emissions program on July 15. The allowances in the booster will come from a reserve for new entrants in the ETS and from an existing buffer of free permits that can be handed to companies as support for low-carbon investments," said the people, who asked not to be identified discussing a confidential matter.

In terms of the timing of the sale of these 400m allowances – clearly the most price-sensitive question – the Bloomberg story said:

“The European Union plans to stagger the sale of €30 billion of carbon permits, seeking to ensure that its push to help industries finance a shift to clean energy doesn’t depress emissions prices.”

This should have been a reassuring message for the market, especially considering the notoriously long time it takes to amend EU Directives. Indeed, even allowing for an accelerated process in the revision of the EU-ETS Directive, given the political urgency to provide visibility to EU industry, we think it unlikely that the process will conclude before summer 2027, in which case the earliest that any of the 400m could ordinarily be sold would be September 2027 or more likely January 2028.

However, the concluding paragraph of the article then left open the possibility that some of these 400m EUAs could come to market before the revisions to the ETS Directive have been finalized and passed into EU Law:

“One option under consideration by the Commission is to propose fast-tracking a part of the reform to bring forward permit sales under the booster, helping to accelerate the industrial shift to cleaner energy.”

This probably explains the drop in prices yesterday, although EUAs did recover somewhat in the afternoon. However, while this means uncertainty around the timing of the sale of the 400m allowances will hang over the market until the ETS Review is launched on July 15, we think the European Commission will ensure a measured and orderly sale process of these 400m allowances over the medium term. As a result, we think it is highly unlikely that any of these 400m EUAs will come to market already in 2026.

Meanwhile, on May 29, the European Commission published the Total Number of Allowances in Circulation (TNAC) for December 31, 2025, which came to 1,023.5m. This was in line with market consensus, which means that 190m EUAs will be removed from auction volumes over September 2026-August 2027 and placed in the Market Stability Reserve.

Carbon Market Roundup

The weighted global price of carbon eased over the week, closing at $58.05, down 1.56%. EUAs fell to €77.07, down 3.84%, while UKAs slipped to £55.11, down 4.87%. In North America, CCA prices rose to $32.29, up 5.01%, and RGGI allowances moved lower to $44.74, down 6.05%. WCA also edged down to $65.75, a 1.20% weekly decline.