Geopolitics in Focus for EUAs Again, RGAs Rally Hard on Virginia Re-Joining RGGI

4 Min. Read Time

After reaching its highest level since the conflict with Iran began on April 17, EUAs eased over the week, with sustained risks around the Strait of Hormuz lifting oil and benchmark European gas, the front-month Title Transfer Facility (TTF), prices.

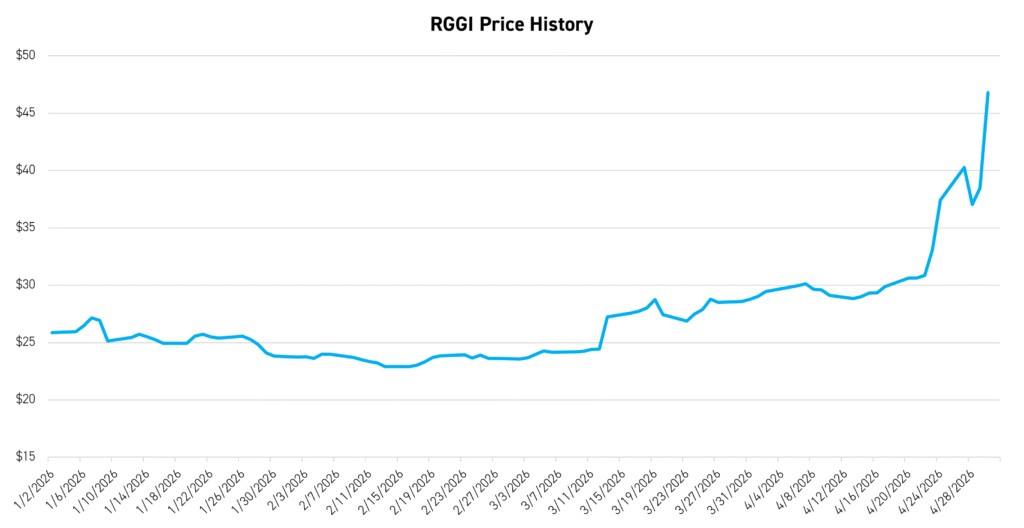

In the US, the Northeastern power market (RGGI) surged higher on Virginia’s official re-acceptance into the carbon market, which was confirmed late Wednesday. RGAs had rallied more than 30% from their April 17 level of $29.87/short ton (st) to a new all-time high (ATH) of $42.19/st on April 24, before falling sharply on April 25 and then rallying back to $40/st on Wednesday on the official confirmation of Virginia re-joining. The surge in RGAs reflects expectations that Virginia’s return will significantly tighten the RGGI market balance in the second half of the year.

EUAs drift lower on continuing stand-off between the US and Iran over the Strait of Hormuz

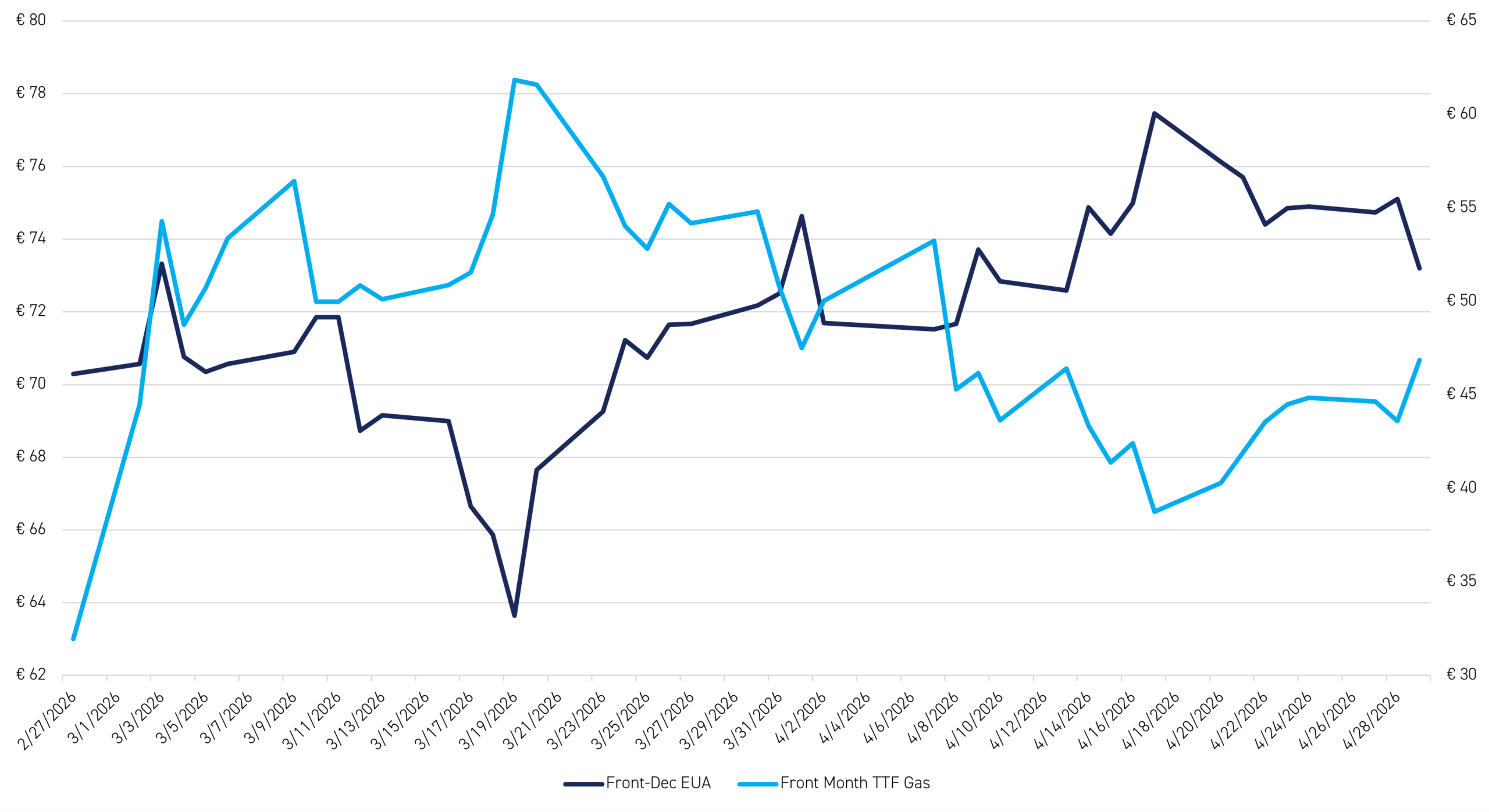

Figure 1 shows the price of the Dec-26 EUA contract versus the Front-Month TTF natural-gas contract since the outbreak of the war between the US/Israel and Iran at the end of February.

Figure 1: Front-Dec EUA (LHS, €/t) versus Front-Month TTF (RHS, €/MWh) Feb 26-April 29 2026

Source: Bloomberg

As explained in recent blogs (see, for example, our blogs of April 10 and March 4), there is a strong inverse correlation between EUAs and TTF. This is because the higher TTF goes, the greater the pressure on EU industry, and hence the greater the perceived political pressure to intervene in the carbon market. This is why the highest closing price for TTF year-to-date so far of €61.8/MWh on March 19 coincided with the lowest closing price YTD for EUAs of €63.7/t. With the announcement of an initial two-week ceasefire on April 8 bringing relief to global energy markets, TTF had fallen 28% by April 17 from its close immediately before the ceasefire deal was announced, thereby prompting a €6/t rally in EUAs over the same period as they hit their highest close since the war began on April 17 of €77.5/t.

Over the last two weeks, however, global energy markets have rallied hard on the US blockade of Iranian shipments out of Hormuz and the fact that Iran views this blockade as a violation of the ceasefire (albeit without any return to military aggression on its part so far). The benchmark Brent crude-oil front-month contract hit $126/bbl in early London trading this morning, its highest level since June 2022, and up $36/bbl (40%) in only 8 trading days since April 17. As a result, TTF has also rallied, albeit less dramatically, closing Wednesday at €46.90/MWh, up 21% from April 17.

With TTF going higher, EUAs have drifted lower, closing at €73.40/t on Wednesday. With EU policymakers still extremely sensitive to the impact of high natural-gas and electricity prices on industrial competitiveness, the pattern of inverse correlation shown in Figure 1 therefore continues. The bottom line is that the conflict between the US/Israel and Iran remains very tense, and any sign that the ceasefire is at risk and hence that kinetic hostilities might resume in the near term will continue to be a risk weighing on EUAs, especially with the EU-ETS Review to be formally launched in July.

Virginia will officially re-join RGGI from July 1, sparked sharp rally and volatility in RGAs

As explained in our blog on April 10, RGGI allowances (RGAs) had already received a strong boost in early April from Virginia’s bid to re-join RGGI as of July 1, even though it was not a done deal that it would be able to re-join the scheme halfway through the year, given potential resistance from other member-states fearing a tighter market as a result. Indeed, we thought that January 1, 2027, would be a more realistic date for Virginia’s readmission.

Over the last week, however, RGA prices rose on speculation that Virginia would in fact be re-admitted from July 1, with the benchmark Dec-26 contract closing at an ATH of $40.28 on Monday, April 27, up 35% from the close on April 17. The price surge continued on Tuesday morning to post a new intraday ATH of $42.19 before then dropping sharply on Tuesday afternoon to close at $37.04. On Wednesday, prices then surged again to close at $40.50 after RGGI issued an official statement at 5 pm Eastern Time re-admitting Virginia to the scheme from July 1.

The RGGI statement read as follows:

With the approval by Governor Spanberger of Virginia’s regulation reinstating their CO2 budget trading program, the RGGI participating states are pleased to welcome Virginia as a returning RGGI participant. Virginia’s participation, along with their compliance requirements, will resume July 1, 2026. Virginia’s allowance budget for the second half of 2026 will be 11.48 million allowances, and they will participate in the September 9 and December 2, 2026 auctions. This will be in addition to allowance offerings from the other ten RGGI participating states in those auctions. Virginia will also originate 1.148 million Cost Containment Reserve (CCR) allowances for the remainder of 2026. Later this year, Virginia will undertake regulatory action to align the state’s program with the outcomes of the Third Program Review and the updated Model Rule by January 1, 2027.

By Thursday, RGA prices then rose another 16% to close at $46.79 after hitting a new intraday ATH of $47.1.

Figure 1: Front-Dec RGA ($/st) Jan 1-April 30, 2026

Source: Bloomberg

Virginia’s re-entry is regarded as bullish for RGAs because the state is expected to significantly boost allowance demand for the program. The state’s emissions have risen sharply over the last couple of years on the back of surging power demand from data centers (currently home to the most data centers in the country) and increased gas-fired power generation, with the state looking set for a significant supply deficit this year. Clear Blue Markets estimates that the re-admission of Virginia will flip RGGI for the second half of this year into a supply deficit of nearly 0.8m short tons for the full year 2026, compared with an expected surplus without Virginia being included.

Meanwhile, California carbon allowances (CCAs) and Washington state carbon allowances (WCAs) have remained subdued in the last couple of weeks. The Dec-26 CCA contract closed at $29.16/t on April 28, flat against its close on April 17 of $29.17/t as the market awaits the end of the 15-day consultation on the revised ISOR later this week. The Dec-26 WCA contract closed on April 28 at $66.49/t, down 4% against its closing level on April 17.

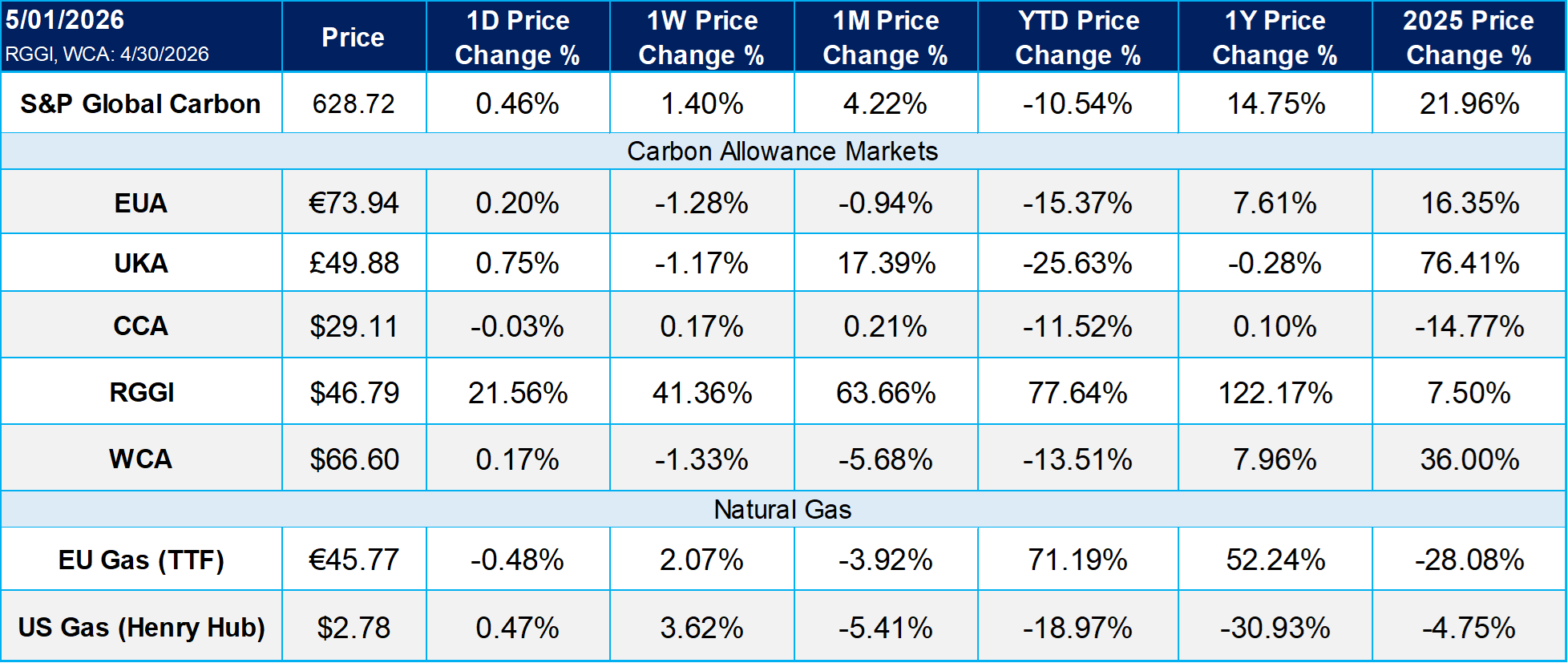

Carbon Market Roundup

The weighted global price of carbon rose over the week to $54.35, up 1.40%. EUAs eased to €73.94, down 1.28% on the week, while UKAs ended at £49.88, down 1.17%. In North America, CCA prices were little changed at $29.11, up 0.17%, while RGGI allowances surged to $46.79, up 41.36%! WCA slipped to $66.60, down 1.33% over the period.