Updated California Supply-Demand Balances, EUAs Back at €80 on Iran Peace Deal

By Mark Lewis & Climate Finance Partners LLC (CLIFI)

4 Min. Read Time

Following the approval of the California Cap-and-Invest Program reform package at the CARB Board meeting on May 28-29, we have updated our supply-demand balances through 2035, including our latest assumptions on the linked Quebec market as well.

In Europe, both EUAs and UKAs have bounced on the breakthrough in peace talks with Iran last weekend, as well as on the planned UK-EU summit in mid-July and a likely formal agreement to link the UK-ETS with the EU-ETS.

Updated WCI balances show tightening supply

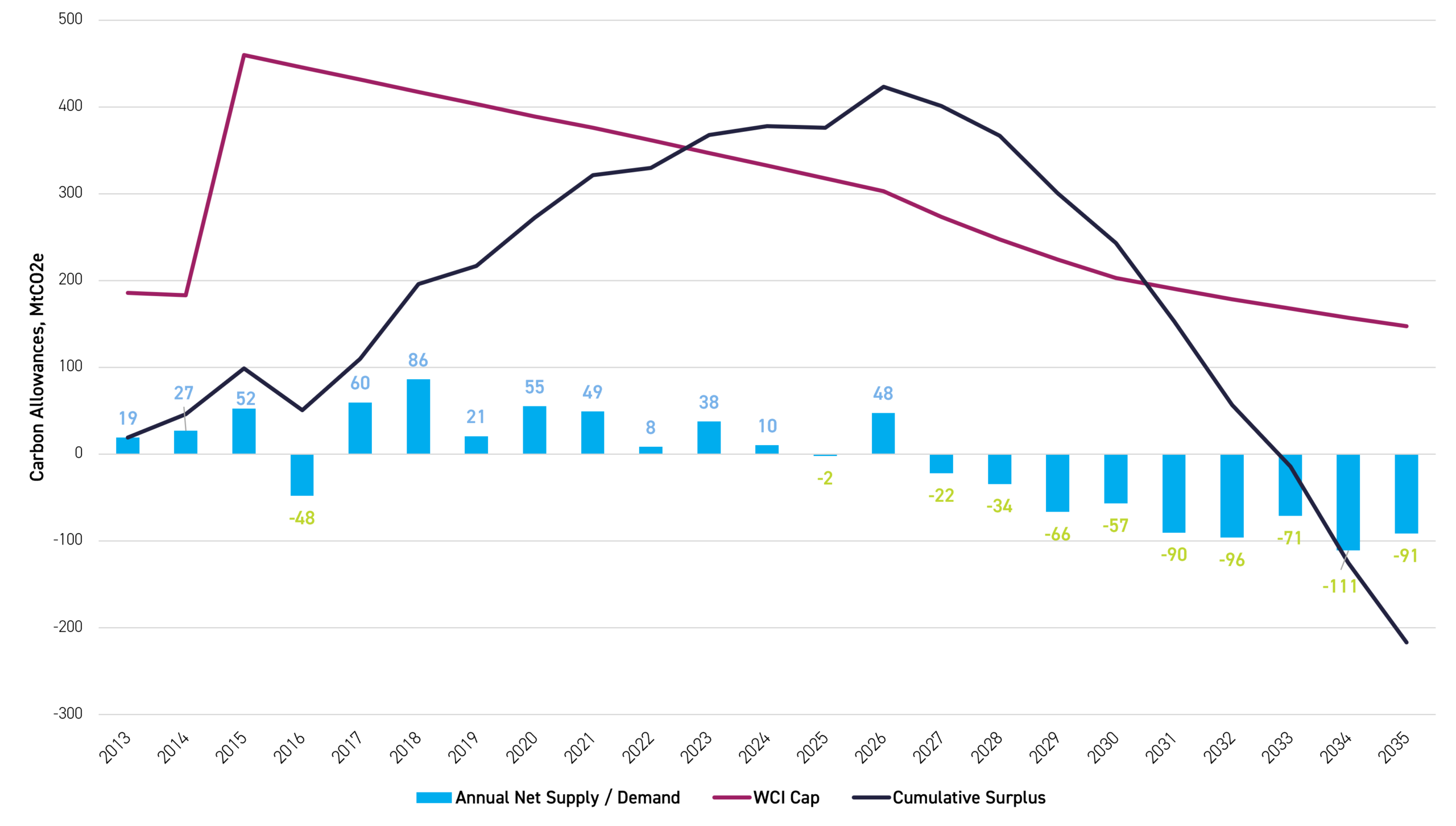

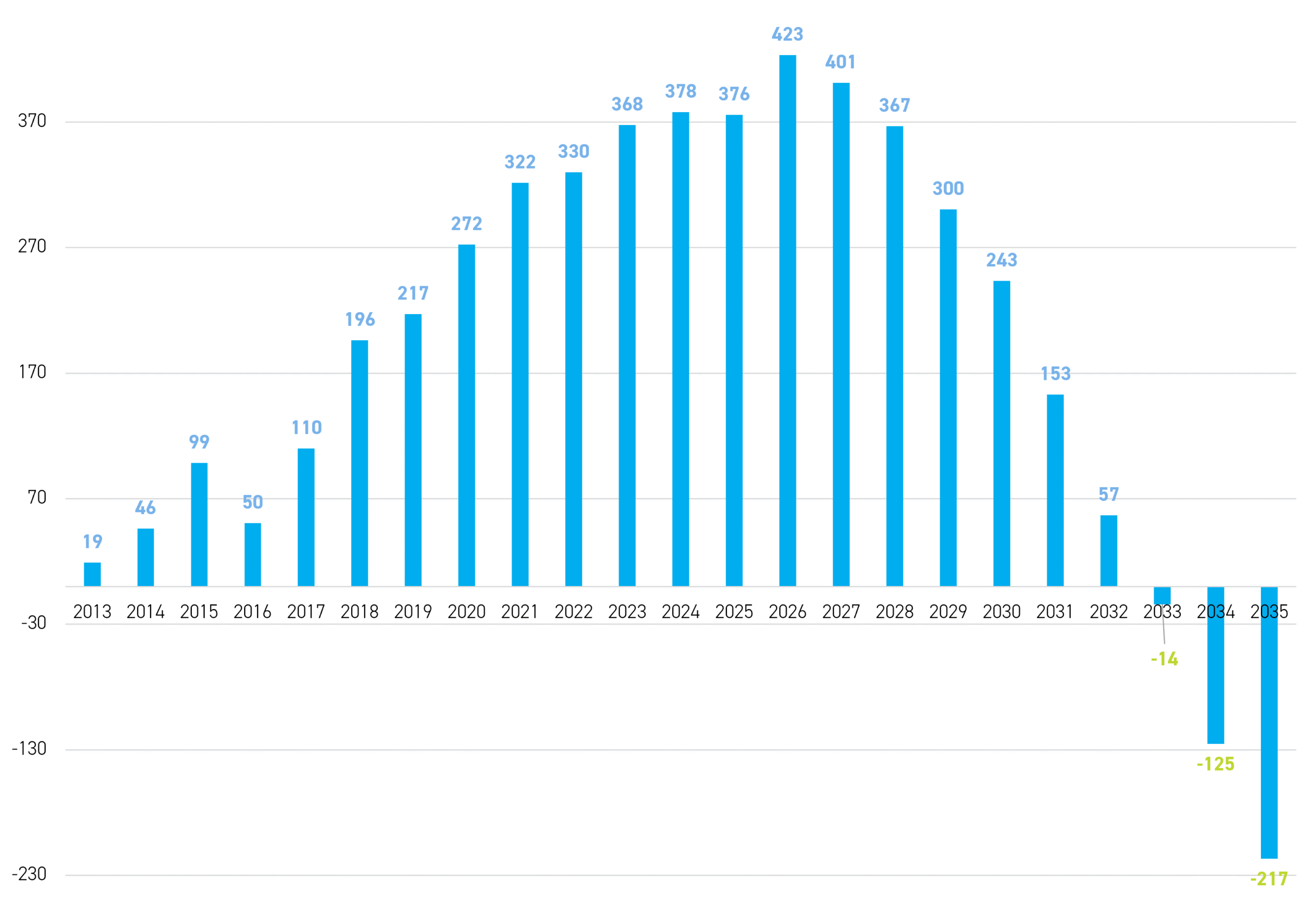

Figure 1 shows our updated supply/demand balances for the Western Climate Initiative (WCI), ie., the joint California and Quebec market, through 2035, and Figure 2 shows the cumulative surplus/(deficit) through 2035.

Figure 1: WCI annual cap and annual and cumulative system balances, 2013-35 (Mt)

Source: CLIFI, Clear Blue Markets

As explained in our June 5 blog, we expect 30 million CCAs from the Manufacturing Decarbonization Initiative (MDI) pool to be distributed over 2028-30, and then a further 40 million over 2031-35, totaling 70 million MDI allowances from the overall MDI reserve of 118 million. The new MDI program selectively awards MDI allowances to compliance entities that invest in eligible decarbonization projects to support industrial competitiveness. It was a slightly more contentious policy item due to the introduction of an additional reserve and its implications for supply. However, even if the full reserve is utilized, albeit higly unlikely, the market is still projected to see its cumulative bank depleted in the same year (just with a smaller cumulative deficit).

At the same time, we have also updated our assumptions on the S/D implications for the WCI arising from Quebec’s updated regulatory package published on May 20. Quebec’s updated package no longer removes the 17m allowances from its pre-2030 caps that it had originally proposed.

After accounting for these changes to our assumptions, we are now projecting a surplus of 46Mt this year, followed by continuous annual drawdowns of the accumulated bank of allowances over 2028-35.

As shown in Figure 2, this means we now expect the WCI bank of allowances to be depleted by 2033, one year later than in our modeling of the original reform package formally introduced through the Initial Statement of Reasons (ISOR) in January 2026, with a projected structural deficit in the WCI market by the end of 2033 of -14Mt. Thereafter, the cumulative deficit increases quickly, reaching -125Mt in 2034 and -217Mt in 2035.

CCAs have performed well during Q2, closing at $32.29/t last night, up 12% since March 31 and 4% since May 27, the day before the CARB Board meeting that approved the revised ISOR began. We think the way is now clear for CCAs to reprice structurally over the next 12-18 months.

Figure 2: WCI cumulative system balance 2013-35 (Mt)

Source: CLIFI, Clear Blue Markets

Additionally, we think there will likely be increased speculative interest in CCAs in 2027 as the prospects for linking the Washington market with the WCI come into sharper focus, which would add tightness to WCI balances at the margin.

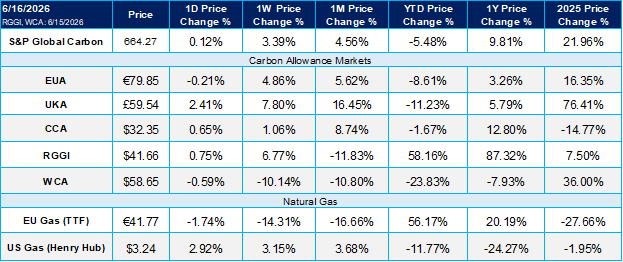

Elsewhere in the US, RGGI prices have climbed back above $40/t in recent days, with the benchmark Dec-26 contract closing last night at $42.25/short ton. This is an impressive recovery following the sell-off in response to the Q2 auction, which settled at $35 (a 21% discount to the spot price on auction day of $44.5), and reflects the additional tightness that Virginia will add to the RGGI system when it re-enters on July 1. RGAs are now up 46% in Q2, and 60% YTD.

Meanwhile, Washington’s Q2-2026 auction results released on June 10 showed a settlement price of $64.56/t, just shy of the 2026 Allowance Price Containment Reserve (APCR) trigger price of $65.26/t, and 39 cents below the spot price on auction day. The APCR trigger is serves as a speed bump to to stablize the market from excess price spikes by releasing additional allowances from a reserve if triggered, where the trigger price rising 5% plus CPI annually. This is the lowest settlement price since Q3-2025 and means there will not be an APCR auction ahead of the September auction, the first time this has happened since the Q3-2025 auction.

The passage of the WCA market reform, HB-1975, in the Washington House of Representatives in May 2025 has greatly reduced the risk of the first compliance period (CP1) being short, as it allows for the funneling of an additional 5.6m V23-26 allowances to the market in the first three auctions of 2027, ahead of the CP1 compliance deadline of November 2027, together with an additional 14.1m APCR allowances, should the market need them. This is more than enough supply to meet CP1 demand. The benchmark Dec-26 contract closed last night at $57.25/t, down -19% in Q2 so far, and -26% YTD.

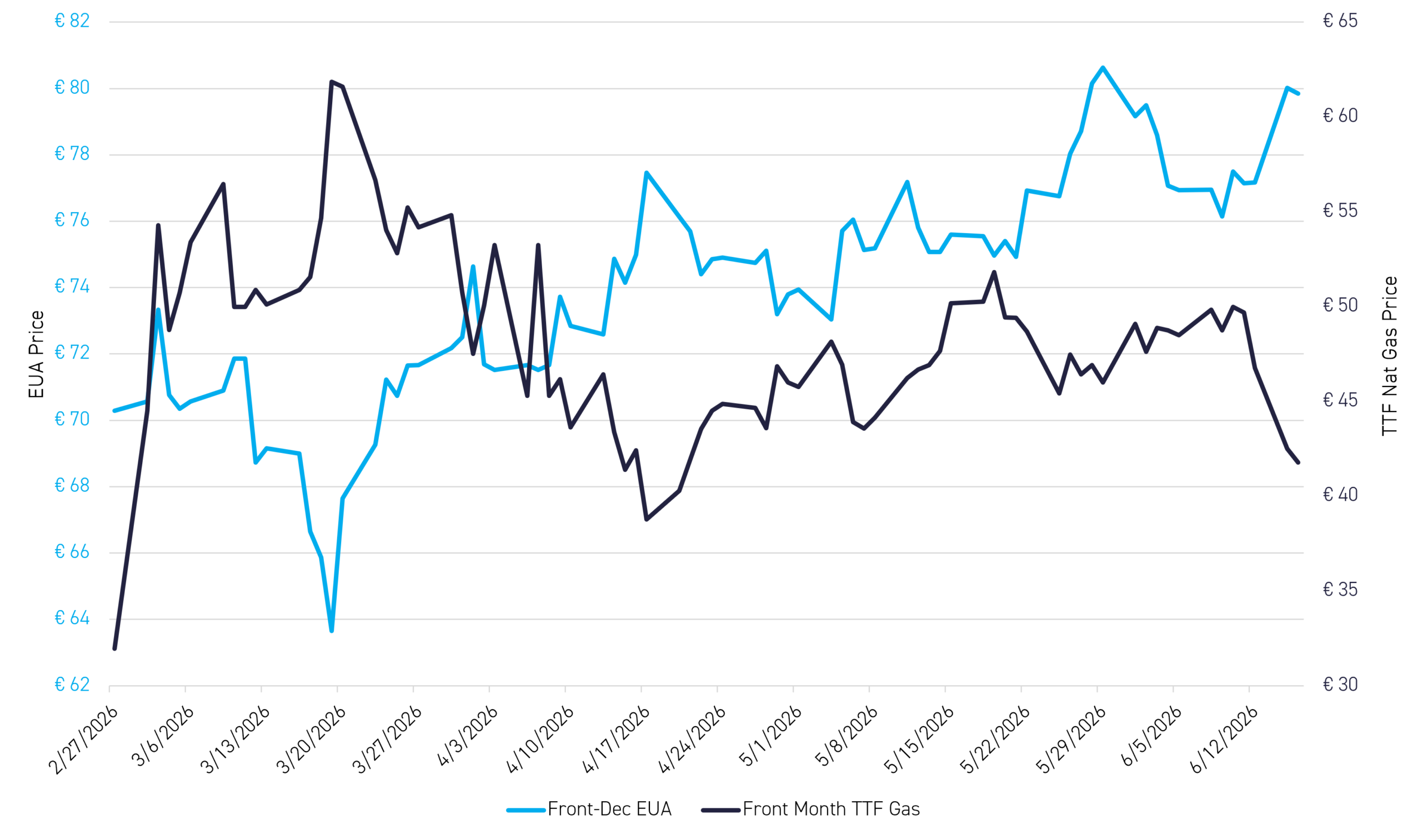

EUAs back at above €80/t last week, EUAs fall back

EUAs closed last night at €79.85/t, and UKAs at £59.54/t, with both having had a strong week so far following the news that the US and Iran had reached an agreement on a peace deal, with a 14-point Memorandum of Understanding (MoU) set to be signed this Friday in Geneva.

EUAs and UKAs have suffered much more than US carbon allowances from the Iran war, owing to the strong upward pressure on EU natural-gas prices – and hence the increased political pressure on carbon prices – that the war has brought.

Figure 3 shows EUAs against the European natural gas benchmark Title Transfer Factility (TTF) since 27 February, the day before the kinetic conflict between the US and Iran began. There is a clear inverse relationship between EUAs and TTF over this period, and as hopes for a deal have increased since the beginning of June, EUAs have risen and TTF has dropped.

Figure 3: Front-Dec EUA (LHS, €/t) versus Front-Month TTF (RHS, €/MWh) Feb 27-June 16, 2026

Source: Bloomberg

With the MoU agreed over the weekend, creating hopes of a permanent end to the conflict and a re-opening of the Strait of Hormuz, Brent Oil futures and the benchmark EU TTF natural-gas price have both fallen sharply since Monday’s open, allowing EUAs to hit €80/t again in intra-day trading yesterday and now again today at the time of writing.

Meanwhile, UKAs posted their highest settlement since February 4 yesterday at £59.54/t, boosted both by the US-Iran MoU and by expectations of a formal deal on linking to be announced at the UK-EU summit penciled in for mid-July

Carbon Market Roundup

The weighted global price of carbon rose over the week to $58.74, up 3.39%. EUAs moved higher to €79.85, gaining 4.86% on the week, while UKAs climbed to £59.54, up 7.80%. In North America, CCA prices increased to $32.35, up 1.06%, and RGGI allowances advanced to $41.66, up 6.77%. WCA was the only major carbon benchmark to weaken, ending at $58.65, down 10.14% over the period.