EUA Volatility Amid Tariff Threats, Net Length Extends to Further Highs

2 Min. Read Time

European carbon allowance prices mirrored the sharp increase in volatility in wider financial and commodity markets, as investors reacted to renewed trade tensions between the US and China.

Last weekend, President Trump floated an additional set of tariffs on Chinese goods after Beijing had announced new restrictions on the export of rare earth minerals, which are a vital component of electronics including smartphones, electric vehicles and wind turbines.

Also last week, both the US and China increased port fees on vessels linked to each other.

Responding to the Chinese rare earths announcement, President Trump last Friday announced plans to impose tariffs of 100% on China exports to the US from November 1, triggering a widespread sell-off in equities and commodities that saw crude oil fall 3.8% and EUAs drop 2% on Monday.

The weakness extended until Wednesday, when carbon, natural gas and German power all staged rallies as the latest tariff threat appeared to recede among more measured comments from leading US policymakers.

EUAs bottomed out at €76.68 on Wednesday, before staging a rally that saw them back near €80.00 just 24 hours later, showing a revival in volatility that has sparked an uptick in options hedging.

It’s worth bearing in mind that the latest trade spat between Washington and Beijing has little directly to do with the EU or its trade balance, and this highlights a growing feature of the EU ETS: the increasing role of speculative capital and its influences.

Industrial production in Europe and the resulting demand from compliance entities is seen as a secondary influence that is less price-sensitive.

Instead, trading sources refer to the growing link between EUA prices and equity indices such as the S&P 500, and carbon has indeed started to follow the wider risk-on and risk-off momentum in financial markets.

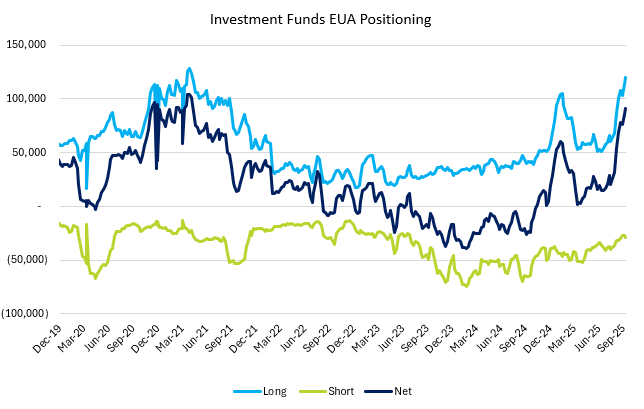

Underlining speculators’ growing role, the latest data from the two main European exchanges show that investment funds now account for 9.5% of total open interest in EUA futures contracts, the most since mid-March.

Funds’ net long positioning has increased to 90.8 million EUAs, the biggest bullish bet since April 2021 – the year when carbon prices soared by 150%.

Analysts have suggested that this latest jump in length may not have much further to go, with Energy Aspects’ Jahn Olsen suggesting that commodity trade advisors have maximized their possible length, and that the market may therefore not be able to sustain a move above €80.00 until later this year.

Even the role of natural gas in pricing EUAs has diminished somewhat, as European supplies are more comfortable ahead of the coming winter, and Asian demand has remained subdued.

The 10-day rolling correlation between front-month TTF and EUA prices has dropped from +0.77 to +0.33 in the last month, while the 10-day correlation in the daily price changes between the two has fallen to -0.09 from +0.78 a month ago.

This leaves EUAs increasingly vulnerable to speculative flows that may not reflect carbon fundamentals, some seasoned observers point out. While the medium-term outlook still calls for a sharp supply cut during 2026 that is expected to boost prices, some participants express concern that the full effect of this reduction in supply may be diluted by continuing declines in European industrial activity.

Carbon Market Roundup

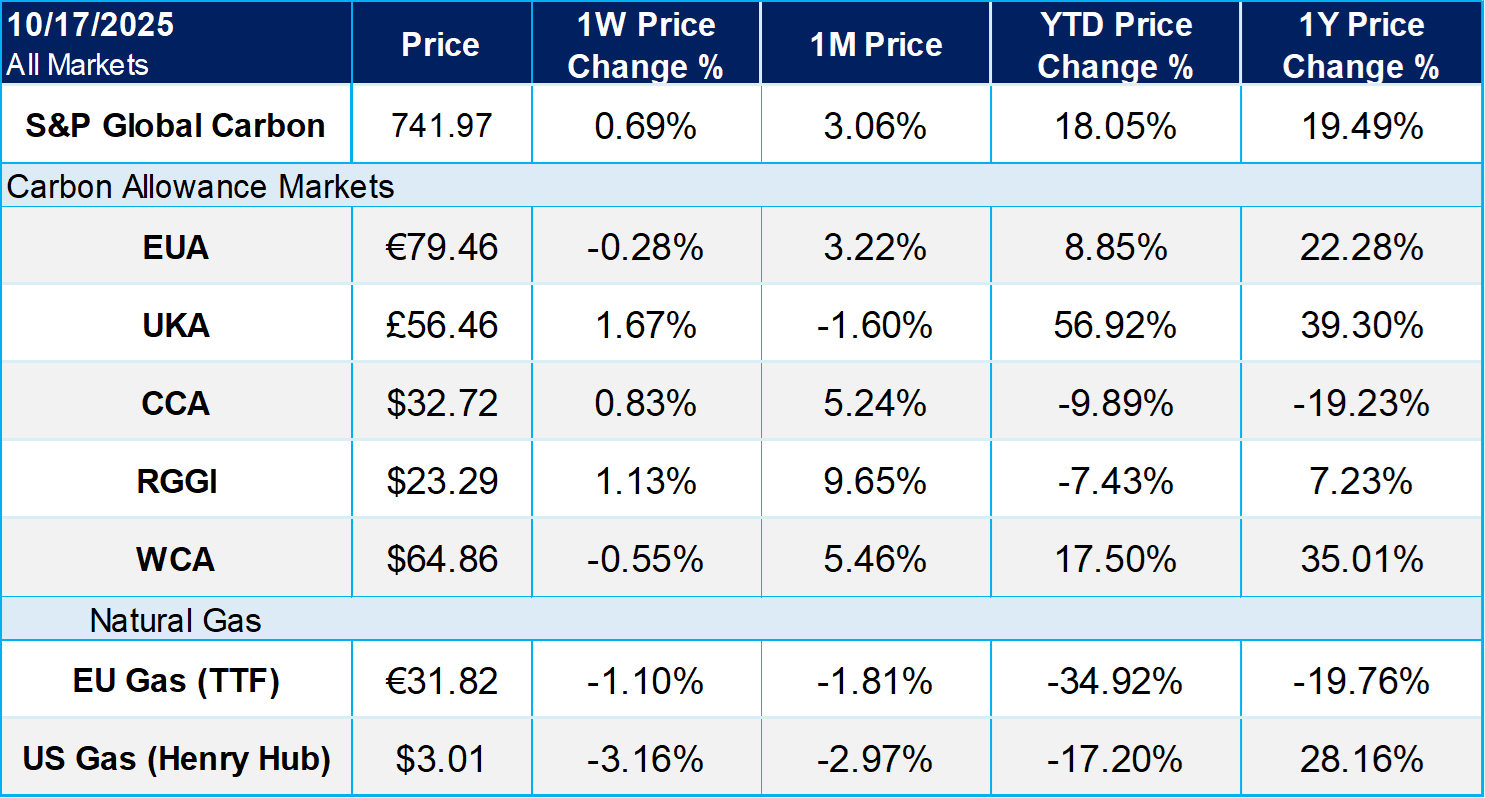

The weighted global price of carbon was $56.26, up 0.7% week over week. EUAs were down 0.3% to settle at €79.46. UKAs were up 1.7% at £56.46. CCAs closed at $32.72, up 0.8% for the week. RGGI was up 1.1% at $23.29 while WCAs were down 0.6% at $64.86.