Executive Order Deadline Nears; RGGI, Washington Hold Q2 Auction

3 Min. Read Time

Across global markets, RGGI and Washington state both had their second quarterly auction for the year on Wednesday, with results expected next week. For those watching the California carbon market, we could get some clarity from the Attorney General as we reach the 60 day deadline following the President's April Executive Order.

The market is expecting a response from the AG though the content could range widely. On one end of the spectrum, it could skip over California altogether and focus just on New York, Vermont, and others that seemed to be at the core of the EO. It could include a direct focus on California's cap-and-trade along the lines of the program's linkage with Quebec or state energy imports, both of which the market has anticipated but is widely seen as legally defensible. On the more extreme end of the spectrum, there could be an unanticipated new item that might create volatility in the short term while the market digests its merits. However, we ultimately think this outcome is unlikely, and the auction reserve price provides decent support especially with its 5%+CPI adjustment 6 months away.

The market has largely priced in the middle scenario, so we would expect a relatively muted response with that outcome, especially as CCAs are already trading at the floor. And, any volatility below that level could create buying opportunities for traders. We also might not see anything materialize, but that is more unlikely. Ultimately, our main takeaway is that clarity, in any form, is positive.

What we do know so far is that the Department of Justice (DOJ) filed lawsuits against New York and Vermont’s “climate superfund” laws, which retroactively require fossil fuel companies to pay for historic climate damages. Michigan and Hawaii are also facing legal challenges for signaling their intent to sue oil and gas firms over similar claims. These moves were widely expected and appeared to be the immediate focus of the administration.

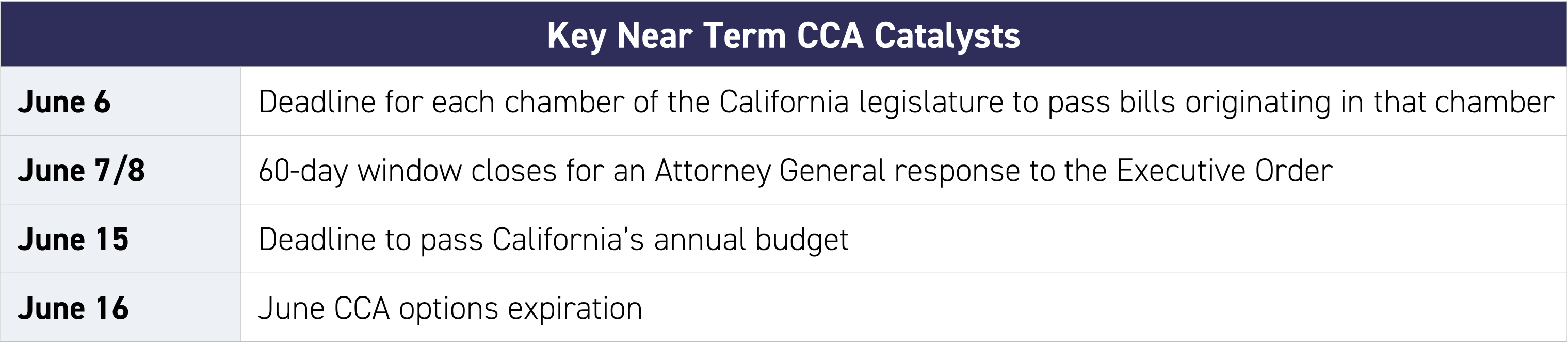

That said, there are still a couple more days left for the AG to file a report. If California is in scope, the most likely direction taken will be the previously attempted (and failed) attack on the program, is through California’s linkage with Quebec under the Western Climate Initiative. The AG could cite the “Compact clause” of the constitution, which prohibits states from entering into “any Agreement or Compact with another State” or with a foreign government without the consent of Congress. An alternative angle targets the out-of-state power providers that sell into the state as the AG could find it violates the Constitution’s “Commerce Clause,” which reserves regulation of interstate commerce for Congress.

Pursuing these measures would also take several years, potentially extending into the next presidential term. We saw this play out with the last challenge against the WCI linkage under Trump's first term, and was ultimately dropped under Biden's administration.

Outside of the EO, other near-term legislative items on the docket include the deadline on June 6 for the Assembly and Senate to approve bills that began in their respective chambers. Two potential vehicles for extending California’s Cap-and-Trade program through 2045—the Governor’s budget trailer bill, AB 1207 or its Senate counterpart, SB 840—are being closely watched as candidates to carry the extension forward. We also expect to see some increased volatility ahead of the June 16 options expiry, though to what extent will depend on how these policy updates pan out.

Looking ahead, market attention remains squarely on the path forward for California’s carbon market, namely the ongoing policy reform and program extension. The reform package, in particular, has become the key driver of CCA price action as it shapes expectations around future supply-demand dynamics.

In some ways, the recent Executive Order served as a catalyst, galvenizing state leadership to reaffirm its commitment to the program and accelerate progress on its extension.

As Rajinder Sahota, Deputy Executive Officer for Climate Programs and Research at the California Air Resources Board, put it, the cap-and-trade program “has never backpedaled—only progressed.” The CCA auctions generate over $1 billion in revenue each quarter that gets redirected back to consumers in the form of utility rebates and investments in energy efficiency, clean transportation, and renewables. This steady stream of funding makes the program a critical pillar of California’s broader economic and energy strategy—one whose value should extend beyond political debate.

Stay tuned for updates related to this EO and other upcoming legislative catalysts.

Carbon Market Roundup

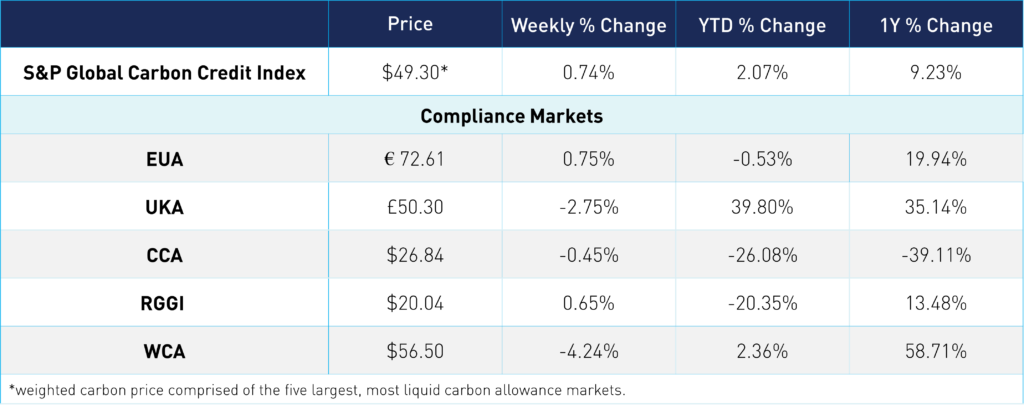

The weighted global price of carbon is $49.30, up 0.7% week over week. EUAs were up 0.8% at €72.61. UKAs were down 2.8% to close at £50.30. CCAs were down 0.5% at $26.84. RGGI was up 0.7% at $20.04, while WCAs were 4.2% lower at $56.50.