UKAs See Support from Investment Funds, CCAs Make a Comeback

2 Min. Read Time

While UK Allowance (UKA) prices have been more volatile than their EU neighbor over the course of the summer, dropping by as much as 20% at one point, UKAs have since rallied over 7% in the last month and are just 9% lower than their quarter-end closing price.

In contrast, EU Allowances have been much more stable, with prices falling by a maximum of just 4.8% in the period between June 28 and today. But while EUAs have lately come under selling pressure, UKAs have found support from investment funds, who currently hold close to a record-long position in futures contracts.

UK market participants are looking ahead to the autumn with optimism, expecting the new Labour government to announce measures to bolster the market and likely also to boost auction revenue. While Westminster has played its cards close to its chest, traders speculate that the new climate and energy minister, Ed Miliband, could unveil proposed reforms before the end of the year. These might include the introduction of a Supply Adjustment Mechanism (SAM), which would replicate the functions of the EU ETS’ Market Stability Reserve.

The EU’s MSR is programmed to remove a percentage of the calculated market oversupply each year and has so far taken around 1.6 billion EUAs out of circulation. Its introduction in 2019 was instrumental in boosting the price of EUAs from less than €10/tonne and setting it on a path to top €100 as recently as 2023.

Further reforms to the UK ETS have also been discussed, including adding the waste sector to the market coverage and enabling the use of greenhouse gas removals to achieve compliance.

Some stakeholders have also suggested that the government might increase the auction reserve price, which also acts as a floor for the secondary market. The reserve is presently set at £22/tonne, though the front-December futures contract has never traded at below £33.50.

All the while, there is a steady drumbeat of encouragement from industry and its allies to link the UK ETS to its larger neighbor. The UK ETS is about 10% of the size of the EU market, and participants in the British system are keen to access the greater liquidity and pool of allowances in the larger market.

Meanwhile, the EU ETS price has fallen by nearly 8% in the past week amid widespread selling pressure across the whole energy complex. The decline was triggered by gloomy economic growth data from China, which in turn led to weakness in metals and oil, and fed through into gas and carbon. December 2024 EUA futures had traded at as high as €72.21 last week, and reached a low of €65.25 on Thursday.

California carbon allowance (CCA) prices have rallied in the last month, after falling to just over $30 in August as the Q3 auction cleared at a weak $30.24.

The December contract climbed back to as high as $35.50 in the last week, triggering some profit-taking, but market participants have suggested prices are likely to remain in the same region for the balance of the year.

Carbon Market Roundup

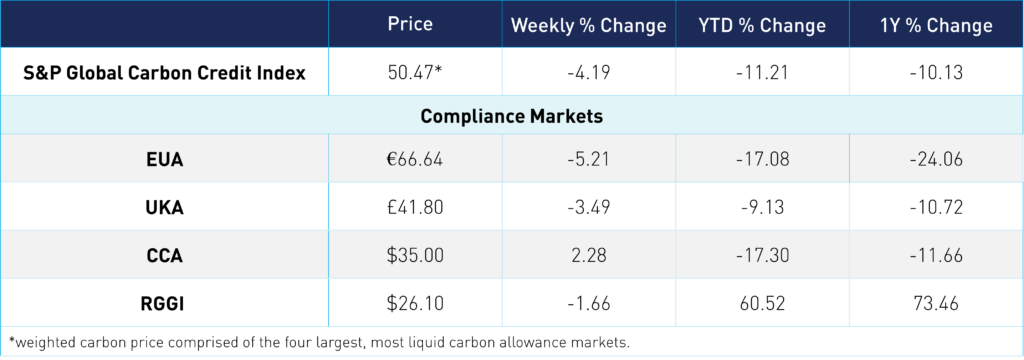

The global weighted price of carbon is $50.47, down 4.19% from the previous week. EUAs are up 5.21% for the week at €66.64, while UKAs are down 3.49% to £41.80. CCAs trended up by 2.28% at $35.00. RGGI was down 1.66% at $26.10.