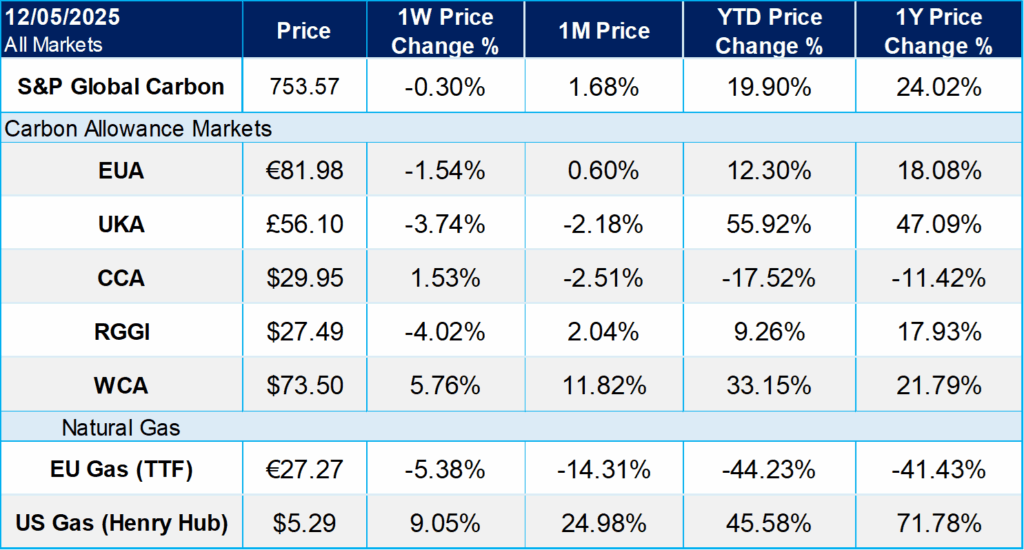

Q4 RGGI Auction Sets New Record, Investment Funds Extend EUA Net Length to All-Time High

3 Min. Read Time

The Q4-2025 RGGI auction cleared at $26.73, which was $4.48 higher (+20%) than the Q3 auction clearing price of $22.25 and a new all-time high for a RGGI auction settlement. The benchmark Dec-25 V25 RGA contract closed at $27.96 last Thursday evening and fell by $1 on Friday morning when the auction results were published, before recovering some of the lost ground to close out the week at $27.15. The cover ratio of 2.4 was down from the Q3 level of 2.8 and the lowest of the year, suggesting that compliance entities were well supplied going into the auction and reluctant to pay above $27.50. Compliance entities purchased 8.2m RGAs (54% of the volume offered), and speculators 7m (46%), such that following the auction compliance-oriented entities now hold 62% of the allowances in circulation, an increase from the 59% they held following the Q3 auction.

RGAs have had a spectacular bull run since hitting the year’s low of $17 in early April, driven both by compliance hedging on the part of power generators expecting increased power demand on the back of AI/data-center growth, and by speculative buying associated with this same narrative. A pause for breath in the final auction of the year should therefore not come as a surprise, and we would now expect a period of consolidation through year-end and into Q1.

In the Washington cap-and-invest program, the benchmark front-year Dec-25 V25 WCAs hit an all-time-high of $75.74 on December 3 – the day of the Q4 auction – before dropping back to close the session that day at $73.5 and ending unchanged on December 4. According to a survey of three analysts conducted by Carbon Pulse, analyst expectations for the results of the Q4 auction clearing price – which will be released at 12pm Pacific Time on December 10 – range from $66.5-71.06, well above the first 2025 Allowance Price Containment Reserve (APCR-1) level of $60.43, and indeed in all cases above the newly released 2026 APCR-1 level of $65.26. This reflects the by now well understood fundamental tightness in the Washington market.

A total of 7.4m V25 WCAs will be offered in the current auction, and 1.9m V28 WCAs in the advance auction, and if the current Q4 auction does indeed clear above the ACPR-1 level of $60.43 then the remaining 3.6m WCAs held in the 2025 Tier-1 reserve pool will be auctioned in Q1 2026.

CCAs had a quiet week after the Q4 auction, with the benchmark Dec-25 V25 contract closing at $29.57 on December 4, up 7 cents versus the previous week’s close. The market is now waiting to see whether the long-awaited ISOR will be published before year-end.

Both California and Washington published their updated auction-floor and APCR levels for 2026, and in both cases the levels will rise by 8% reflecting the annual uplift of 5% plus a CPI bump of 3%. For California, the 2026 auction-floor level will increase to $27.94 (from $25.97 in 2025), while the APCR-1 and APCR-2 levels will increase to $65.31 and $83.92 respectively, and the price ceiling to $102.52. For Washington, the 2026 auction-floor level will increase to $27.92 (from $25.85 in 2025), while the APCR-1 level will increase to $65.26. With the Washington price ceiling set at $80 for both 2026 and 2027, the 2026 APCR-2 level remains to be finalized.

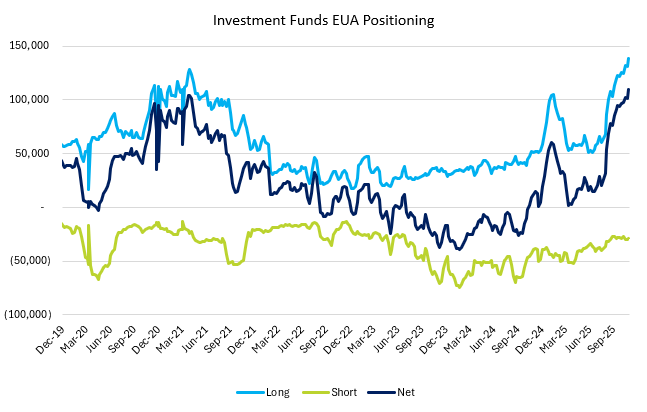

EUAs see record high speculative positioning with end-of year auction break looming

The latest Commitment of Traders (CoT) data published on December 3 revealed that net speculative positioning in EUAs increased by 9Mt last week to reach a new all-time high of 110m tonnes (Mt), surpassing the previous record of 104Mt set in April 2021. This reflects the continuing market consensus that balances in 2026 and 2027 are extremely tight and that this will result in a significant drawdown in the total number of allowances in circulation (TNAC) – the outstanding market inventory – and hence a potential rally in prices as the deficit kicks in.

There is also probably an extra opportunistic element in the large week-on-week increase in speculative positioning in that we are getting closer to the three-week end-of-year-holiday auction break: the last EUA auction of 2025 will be on December 15 and the first of 2026 on January 8. In thin holiday markets with no primary supply prices have typically rallied 5-10% over the end-of-year and new-year period since 2015.

EUA prices actually came off slightly over the last week, though, closing at €81.98 on December 5, down 1.5% versus the previous week’s close. All eyes are now on the options expiry on December 10, with most open interest at the €80 and €85 levels. Once the options expiry is over the market will then focus more on the forthcoming auction break, so we would not be surprised to see a further build in speculative length when the next CoT data is released on 10 December.

Meanwhile, this coming week will see the first meeting in the so-called trilogue process between the EU Commission, Council, and Parliament to reach a compromise agreement on the legislative framework for the 2040 EU Climate Law. This will likely result in headlines about potential areas of compromise, but we think positions are already sufficiently well aligned between the three EU law-making entities that there are unlikely to be any market-moving surprises.

Carbon Market Roundup

The weighted global price of carbon was $58.07, down 0.3% week. EUAs were down 1.5% for the week, at €81.98. UKAs closed at £56.10, down 3.7% over the week. CCAs were up 1.5% at $29.95. RGGI fell 4.0% to $27.49. WCAs were up 5.8% at $73.50.