EUAs Get Some Relief Ahead of Upcoming Changes, CCAs Await Results of Q1 Auction

6 Min. Read Time

EUAs closed last week at €73.78/t, up 4.3% on the previous week’s close, a welcome relief after the precipitous drop from mid-January and the first weekly increase since the week ending January 16. UKAs mirrored EUAs, posting a 4.6% increase on the week to close at £47.62/t, again the first weekly rise since January 16. Meanwhile, we attended an event with a senior former EU policymaker on Monday of this week and gained a clearer understanding of the way the debate about the reform of the EU-ETS is shaping up ahead of the forthcoming EU Council meeting on March 19-20 and the formal launch of the EU-ETS review itself in July.

In the US, CCAs were quiet last week, with the Dec-26 contract up 9 cents on the week to $29.72/t and trading volumes down as traders await the results of the Q1 auction due later today (February 25).

EUAs: March EU Summit now in view, shape of future reforms becoming clearer

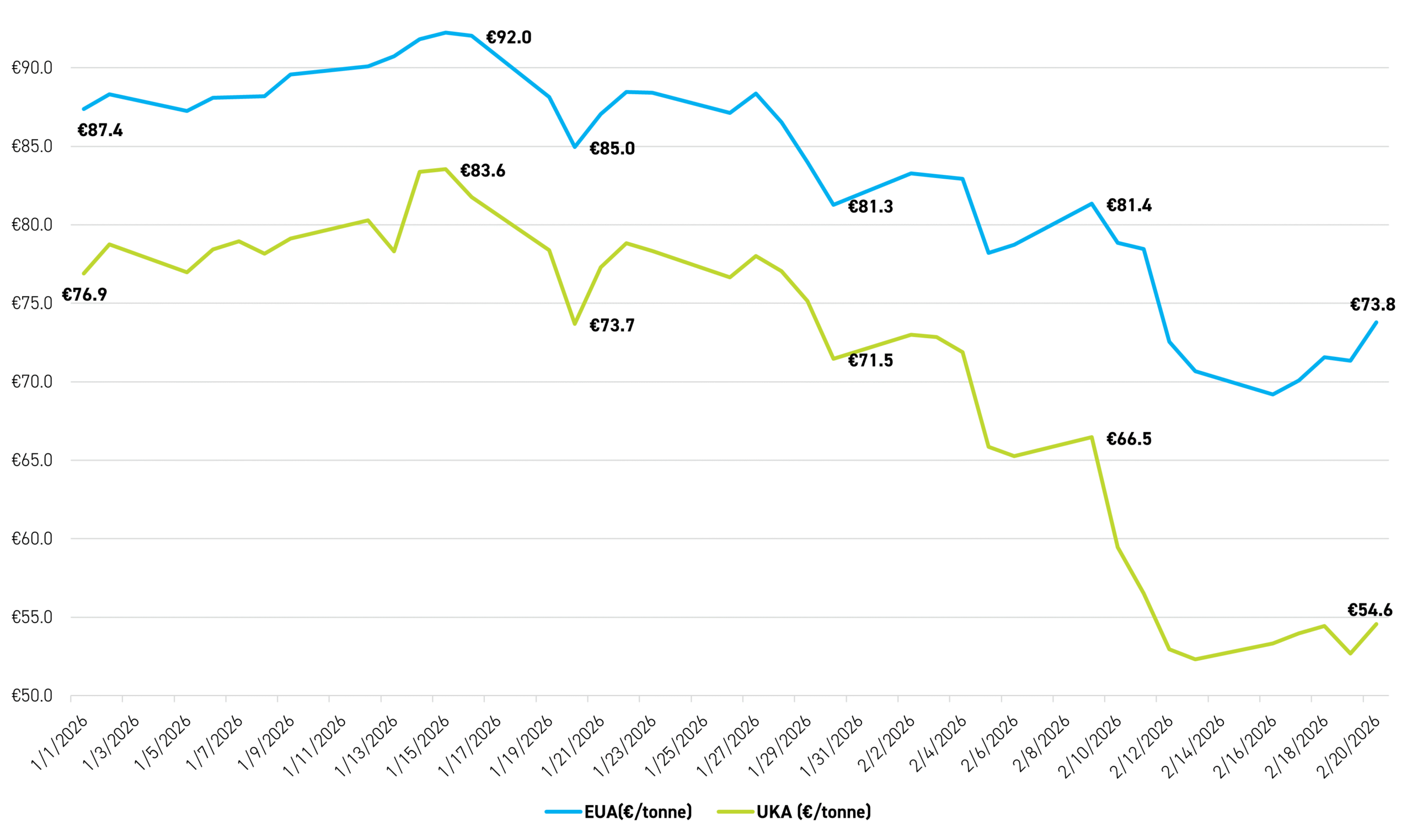

EUAs had a welcome bounce last week, closing up on the week after four consecutive weekly declines, with UKAs also recovering after the buffeting of the last four weeks. As of Friday, February 20, EUAs and UKAs were down 16% and 29%, respectively, for the year to date, with the spread having widened to €19.2/t from €10.5/t at the beginning of the year (Figure 1).

Figure 1: EUA/UKA* closing prices (Dec-26 contract), January 1 - February 20, 2026 (€/tonne)

Source: Bloomberg; *Note that UKA prices are here shown in €/tonne to show the discount at which they still trade to EUAs.

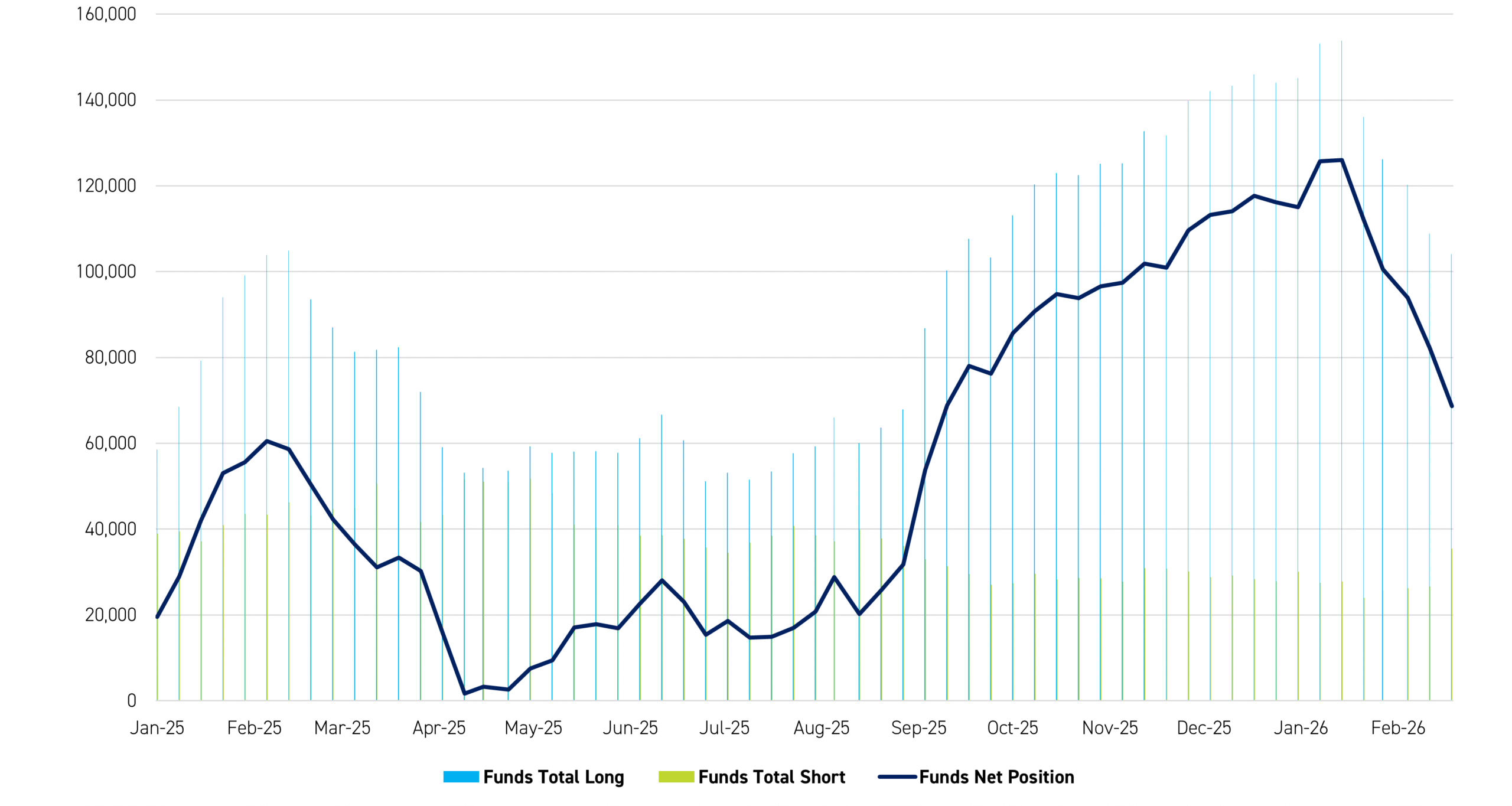

The price drawdown in EUAs over the last four weeks has prompted a significant reduction in net speculative length over the last month. According to the latest Commitment-of-Traders (COT) data published this morning, investment funds held a net long position as of COB on Friday, February 20, of 68.6Mt, down 57.4Mt from the ATH of 126Mt recorded only five weeks ago on January 16 (Figure 2). This brings investment funds’ positioning back to the level of week-ending September 12 last year.

Figure 2: Net speculative length in EUAs, January 3, 2025 - February 20, 2026 (Kt)

Source: ICE

As explained in our recent blog posts,1 there has been a barrage of policy noise in the last few weeks, and this prompted the sell-off in EUAs (and by extension in UKAs) and hence also the reduction in net speculative length. The policy noise has now subsided for the time being as the EU prepares for the next EU Council gathering on March 19-20, and it was against this backdrop that we attended a meeting with a senior former EU policymaker in the carbon space earlier this week who explained how he now sees things shaping up politically ahead of the forthcoming EU Council summit and of the EU-ETS Review in Q3.

We see three main takeaways from the comments made in that meeting, and all three are ideas that have been floated publicly in the last few weeks and covered in our recent blogposts:

These three takeaways are as follows:

- On free allowances: We think there is a growing consensus to delay the phase-out of free allowances2 to industry as well as to allocate the residual allowances in the so-called Cross-Sectoral Correction Factor (CSCF) buffer reserve3 – a total of 260Mt – free of charge to industry (rather than auctioning them back to the market as foreseen in the current legislation). However, such a measure, if implemented, would almost certainly have to come with a commitment in exchange from the recipients of such free allowances that they make low-carbon investments.

- Changes to the MSR: In addition to the EU-ETS Review later this year, the Commission will also be conducting a review of the Market Stability Reserve (MSR), and we think important changes are likely here. For context, the MSR automatically adjusts the supply of carbon allowances by removing surplus permits from circulation when the market is oversupplied and releasing them when supply is tight, with the aim of stabilizing prices and reinforcing long-term scarcity. An idea that seems to be gaining ground is stopping the cancellation of EUAs in the MSR above the current threshold of 400m from 2027 onwards, perhaps together with a move to make it easier for allowances to be released from the MSR if prices spike too aggressively, too quickly at any point in the future.

- A looser LRF: On February 10, well-known Member of the European Parliament (MEP) Pieter Liese – who previously led the Parliament’s work on the EU-ETS – suggested that the Linear Reduction Factor (LRF), the annual reduction rate of the cap on allowances, should be reduced to 3.4% from the existing 4.4% under the forthcoming EU-ETS Review. We explained the background to and mechanics of Liese’s proposal on the LRF in our blog post on February 11, and we think that it is now inevitable that the LRF will be reduced, the only questions being whether in line with Liese’s proposal or by more, and whether from 2029 or 2031.

As explained in our recent blogposts referenced above, the overall combined impact of these proposals would be an increase in the size of the overall cap beyond 2030, extension to the duration of the cap by a few years beyond 2039 (which is the date by which the cap falls to zero under the current legislation), and increase in the total amount of free allowances awarded to industry rather than auctioned.

From a political point of view, it would also give policymakers the ability to control prices more easily should they spike too quickly at any given point in the future. This is because – in keeping with point 2 above – allowing a larger number of allowances to be stored in the MSR from 2027 onwards than the 400m at which the MSR is currently capped would give the Commission more supply to play with in the future if prices were to exceed a politically acceptable level, especially if the conditions under which allowances in the MSR could be made available to the market were to be loosened as well.4

If policy were indeed to develop along these lines during the MSR Review – and that, of course, remains to be seen – we would effectively be looking at a more flexible price-control mechanism than the current very cumbersome Article 29a in the ETS Directive (which has never been used in any case), and in our view this is something that should therefore be watched very carefully as the policy discussions get underway formally, starting with the EU Council Summit on March 19-20.

US news: CCAs await outcome of the Q1 auction

California held its first quarterly auction of the year last week, and the results will be published later today. There were 55 million V26 allowances on offer in this auction, together with an additional 7.2m V25 allowances from the under-subscribed May 2025 auction. With current spot prices barely above the 2026 floor of $27.94/t, there is some speculation that this auction too might be under-subscribed, but we expect compliance players to support the auction given the current low prices near the floor and the expectations of a tighter market going forward in line with the recently published ISOR package.

Carbon Market Roundup

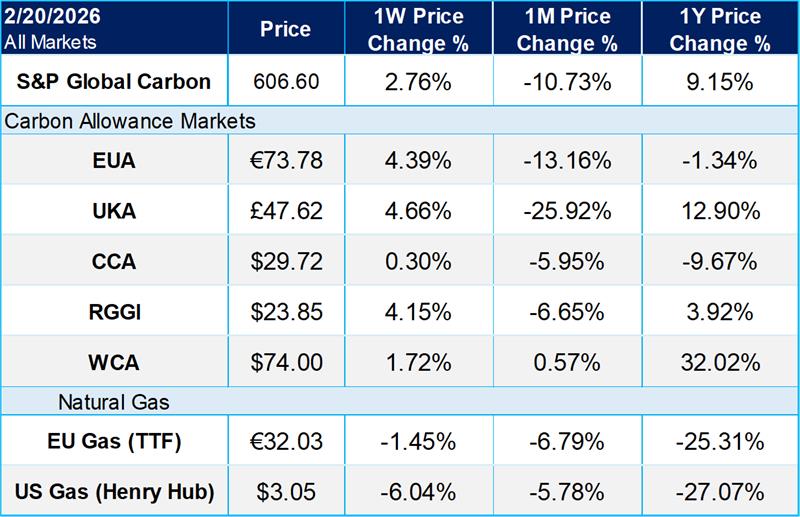

The weighted global price of carbon recovered over the week to close at $52.44, up 2.76% week over week. EUAs rose to €73.78, gaining 4.39% on the week, while UKAs closed at £47.62, up 4.66%. In North America, CCA prices edged up to $29.72, a 0.30% weekly increase, with RGGI allowances advancing to $23.85, up 4.15%. WCA also moved higher, ending at $74.00, a 1.72% gain over the period.

- See in particular our posts on Climate Market Now of February 11 (Hold Tight! Chancellor Merz adds to EU-ETS policy noise with confused intervention), February 10 (Cool Heads Required as EUAs Face Increased Volatility from Political Risk), and February 5 (EUAs Drop on Bloomberg Story, So What is Going On?).

- For context, free allowances are EUAs that are granted at no cost to industries at high risk of carbon leakage to safeguard industrial competitiveness.

- The Cross-Sectoral Correction Factor (CSCF) buffer is a pool of allowances carved out under the 2021-30 cap under Article 10a5a of the EU-ETS directive. These allowances were intended to be allocated to industry as a top-up in the event that the aggregate number of free allowances proposed by member states first over 2021-25 and then over 2026-30 exceeded the maximum allowed amount of free allowances across the EU as a whole.

- Under the current legislation, the MSR can only start releasing EUAs back into the market at a rate of 100m per year once the Total Number of Allowances in Circulation – i.e., the outstanding market inventory of EUAs – has fallen below the level of 400m. We think the MSR Review will prompt a discussion about loosening this criterion with a view to giving more discretion to the European Commission about when and in what volumes the MSR can release EUAs to the market, with the price level becoming a key element in this discussion.