EUAs Fall on Positioning Unwind, CCAs Drift Lower Ahead of February Auction

3 Min. Read Time

Last week saw the continuation of the previous week’s drop in EUAs and UKAs as rising geopolitical tensions triggered a further wave of selling by speculators from still historically high long positioning. And while the underlying fundamentals remain very strong, the positioning shakeout that began with President Trump’s risks of tariffs over Greenland might still have some way to go, given the record length accumulated over the last five months. That said, we think the market will find strong support from compliance buyers in the €75-80/t range, and compliance buyers are ultimately what will make for a sustainable rally. For CCAs, it was a soft week again as the market continues to digest the long-term implications of the ISOR while also awaiting California’s Q1 auction later this month.

EUAs: fundamentals still very supportive but record net speculative length is unwinding

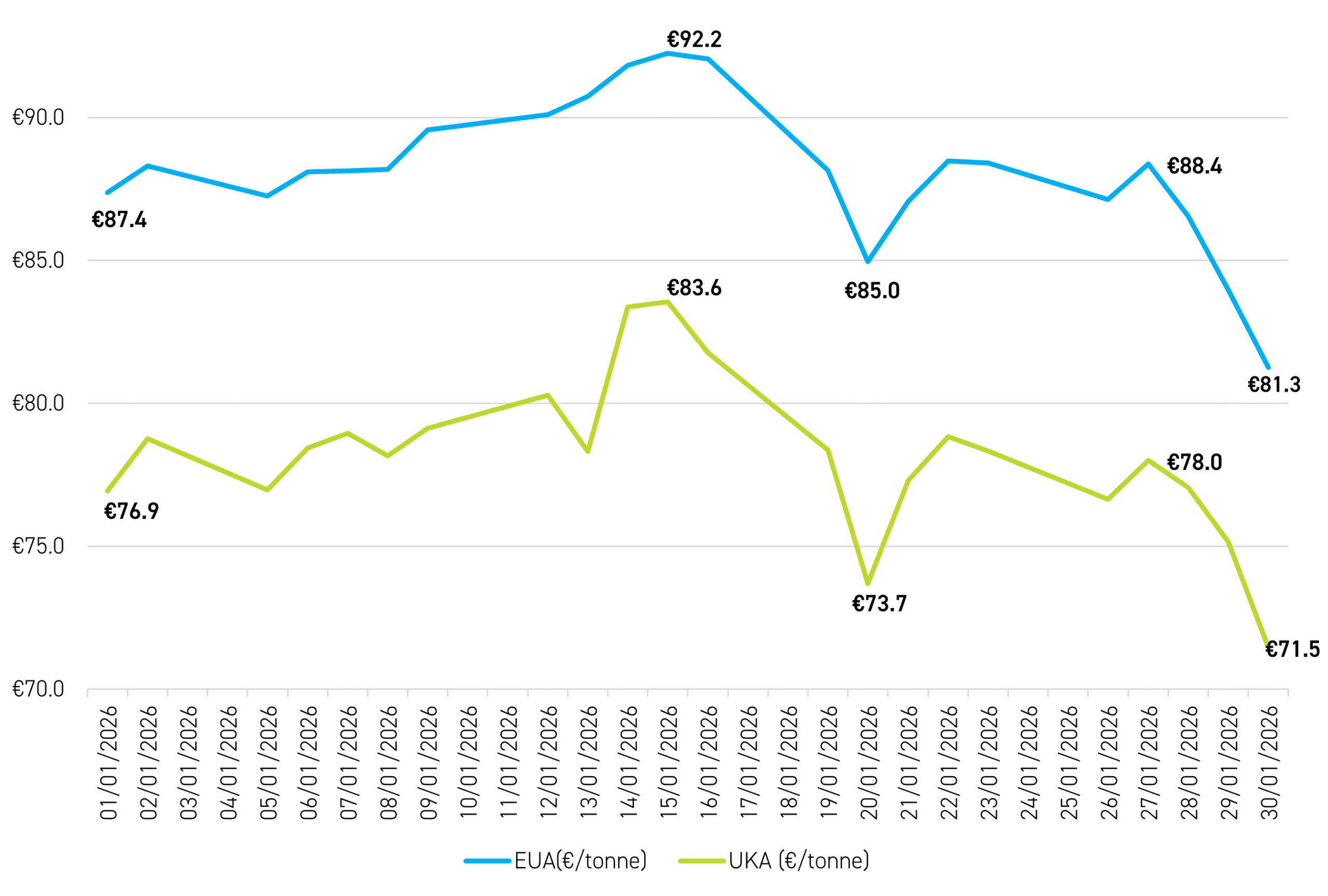

Prices for EUAs and UKAs ended last week at €81.3/t and £61.9/t, down 8% and 9% respectively on the week. Figure 1 shows the performance of the benchmark EUA and UKA contracts since January 1, with UKAs converted from GBP into EUR. As can be seen, the month of January has been a tale of two halves, with EUAs and UKAs having a strong start over the first two weeks of the year but then dropping sharply on geopolitical risks and the shakeout of over-extended speculative positioning, to end the month down 7%.1

Figure 1: EUA/UKA* closing prices (Dec-26), 1-30 January 2026 (€/tonne)

Source: Bloomberg; *Note that UKA prices are here shown in €/tonne to show the discount at which they still trade to EUAs.

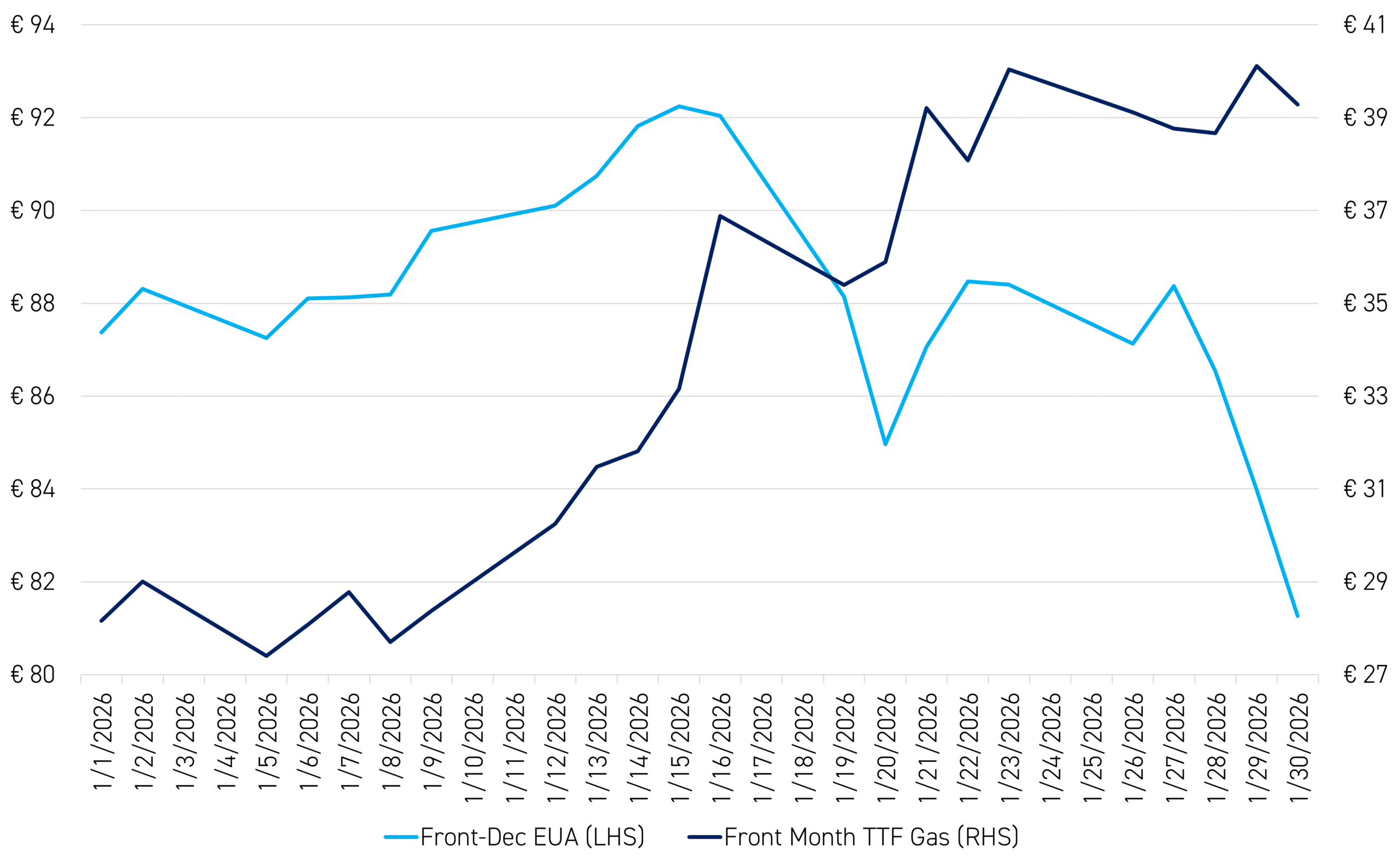

The drop in prices over the last two weeks has been driven by an increase in geopolitical risk, prompting a sharp reversal in European natural-gas prices, with both coming against the backdrop of record net-long speculative positioning.

First, there was President Trump’s tariff threat to the EU and UK over the issue of Greenland, then renewed tension in the Middle East as President Trump increased US naval strength in the region with a view to a potential attack on Iran. At the same time, EU gas prices increased suddenly on both this geopolitical tension and colder weather. As we have highlighted before, the correlation between EUAs and the benchmark EU natural-gas price – the front-month Title Transfer Facility (TTF) contract – broke down last year, and with many speculators having shorted TTF while being long EUAs, there was a corresponding sell-off in EUAs over the last two weeks as they covered their short TTF positions.

Figure 2 shows the price action in EUAs and TTF over the course of January, with the inverse correlation between the two very clear.

Figure 1: Dec-26 EUAs (€/tonne) versus Front-Month TTF (€/MWh)), 1-30 January 2026

Source: Bloomberg

Meanwhile, all of this has been happening against record-high net-long EUA positioning by speculative investment funds. As highlighted in last week’s blog, the net length of 126Mt as of January 16 was an ATH, but we then saw a contraction of 14Mt in the week ending January 23 in the Commitment of Traders (COT) data published by the ICE exchange last week to 112Mt, and we would expect to see a further material reduction in net speculative length when the COT data as of 30 January is published later this week.

Overall, though, given the massive accumulation of speculative length over the last five months, we think the ongoing reduction of this length is healthy, and we continue to view the supply/demand fundamentals in the EU-ETS as very constructive on a medium to long-term basis (see previous blog for more on EUA fundamentals).

CCAs softer again last week as market awaits the Q1 auction

The Dec-26 CCA contract closed last week at $29.7/t, down 4.8% on the previous week’s close of $31.19/t, and now down 10% YTD. We think the softer market tone following CARB’s publication of the Initial Statement of Reasons (ISOR) on January 13 mainly reflects lingering concerns around the possibility of federal action against US state carbon markets and the fact that the ISOR backloads the reduction in the cap to 2028-30, leaving 2027 still well supplied.

There is also the Q1 auction on 18 February coming into view that may be weighing on prices, as there will be an extra 7m CCAs auctioned this time that were unsold from previous auctions.

Overall, however, we remain of the view that the ISOR is very constructive on a medium to long-term outlook. As a result, we would expect both compliance entities and investors to become more constructive on the outlook for prices in the coming weeks and months.

Carbon Market Roundup

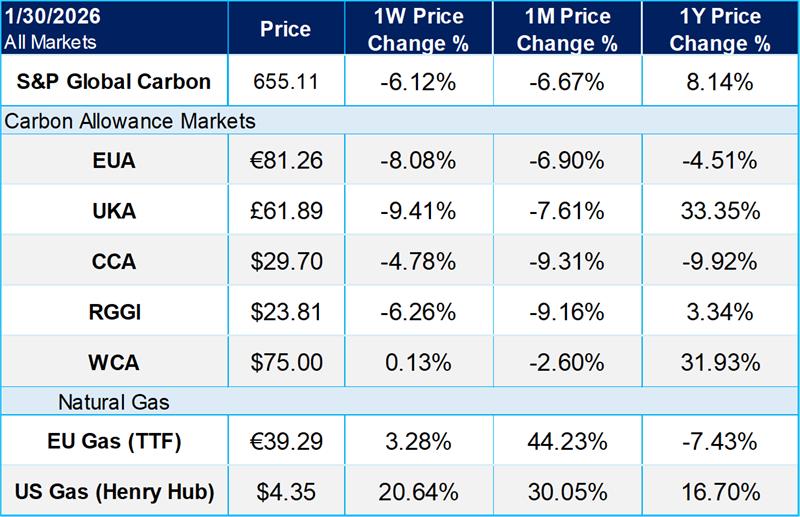

The weighted global price of carbon was $56.64, down 6.12% week over week. EUAs were down 8.08% at €81.26. UKAs fell 9.4% at £61.89. CCAs were down 4.78% for the week, at $29.70. RGGI slipped 6.26% to close the week at $23.81, while WCAs were up 0.13% at $75.00.

- As explained in earlier blogposts this month (see Climate Market Now on January 12 and 21), the price action in EUAs and UKAs is now essentially identical, reflecting the political momentum behind linking the UK-ETS with the EU-ETS and hence the fact that UKAs are now to all intents and purposes a discounted proxy for EUAs.