EU to Propose Amended MSR This Week, CARB to Publish ISOR Amendments Soon

6 Min. Read Time

EUAs were up 6% last week to €71.67/t on continuing relief that the EU council meeting on March 19-20 had not thrown up any negative surprises, while also potentially benefiting from a 12% drop in the benchmark front-month EU natural-gas price (the Title Transfer Facility, or TTF price). All eyes this week will be on the European Commission’s proposals to be announced this Wednesday, April 1, for changes to the Market Stability Reserve (MSR) and the free-allocation benchmarks to industry.

In US carbon, it has been another quiet week, with CCAs edging up above the 2026 floor price over the last few trading days as the market awaits the publication of amendments to the ISOR.

EUAs bounce on weaker TTF as market awaits proposals for MSR and industrial benchmarks

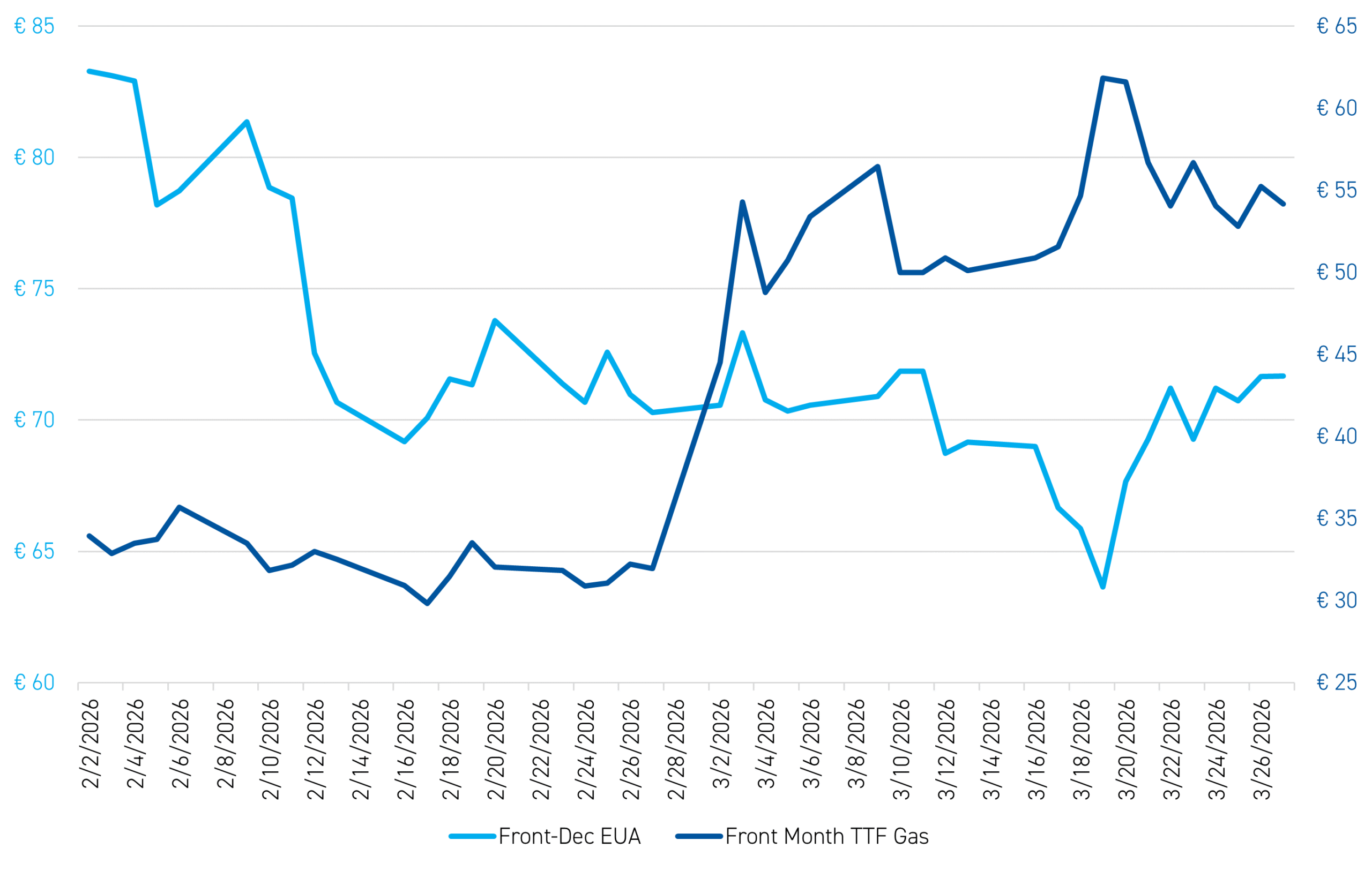

Figure 1 shows the Dec-26 EUA contract against the front-month TTF contract since the beginning of February, showing a clear inverse correlation between the two since the outbreak of hostilities between the US/Israel and Iran on February 28.

Figure 1: Front-Dec EUA (LHS, €/t) versus Front-Month TTF (RHS, €/MWh) February 2 - March 27, 2026

Source: Bloomberg

Over the four weeks since February 28, TTF nat gas is up 70%, and EUAs are down 2%, but over the course of last week, TTF dropped 12% while EUAs rallied 6%. In our view, the logic of this inverse correlation is straightforward: the higher the TTF price goes, the greater the pressure on EU industry and citizens in the form of both higher natural-gas and higher electricity prices, and hence the greater the perceived political pressure to intervene in the carbon market. It is noticeable from Figure 1, for example, that the highest closing price for TTF year-to-date so far of €61.8/MWh on March 19 coincided with the lowest closing price YTD for EUAs of €63.7/t.

It is for this reason that keeping a close eye on TTF prices as a gauge for EUA prices is instructive, as they are a barometer of political pressure at a time when EU industry labours under natural-gas prices that are five times higher than those of the United States, and when any further escalation in the conflict between the US/Israel and Iran could lead to further spikes in global energy prices and hence to a further increase in TTF prices.

All of which leads naturally to the political reaction, with important news to be announced this week on the future of the EU-ETS. As we explained in our last blog, at the recent EU Council meeting on March 19-20, the Commission’s president, Ursula von der Leyen, announced that of the various measures the Commission would propose to amend the EU-ETS to help deal with high energy prices, two would be unveiled ‘in the coming days’. Last week, we learned that these two measures – namely, proposed revisions to the free-allocation benchmarks and the MSR – will be announced this Wednesday, 1 April.1

As far as the benchmarks are concerned, the question is how much more generous these will now be for particular industrial sectors and sub-sectors, with the Chemicals sector in particular – the one most directly affected by higher natural-gas prices – seeking greater relief. However, more generous benchmarks in and of themselves should not really have any significant bearing on EUA prices, as in the end this is about how the same number of overall EUAs are distributed – for free or via auction – rather than about the total amount of supply available to the market.

As far as changes to the MSR are concerned, there are essentially three ways in which the MSR’s workings could be changed.

First, the current rule whereby the number of allowances in the MSR is capped at 400m EUAs and any allowances above that number are cancelled every year could be scrapped from 2027, thus allowing the MSR to build up a larger supply of allowances for smoothing future price spikes.2 We firmly expect the Commission to propose this, and for it to be warmly welcomed by EU member-state governments, and we think this could be fast-tracked in such a way that the new measure could take effect already from January 2027. In other words, we think that all of the allowances taken into the MSR over the course of 2026 – a total of 262m on our numbers – will likely remain there, such that the MSR by the end of 2026 will contain >650m EUAs rather than the 400m mandated by the current legislation.

Second, the Commission could propose to reduce the annual intake rate from the current 24% to 12%, thereby increasing the amount of EUAs available for auction. However, according to a Bloomberg report published earlier today,3 the Commission has in the end decided not to propose any change to the intake rate.

Third, the Commission could look to change the threshold below which it releases allowances back to the market. Currently, EUAs can only be released from the MSR once the outstanding number of allowances held in the market – the so-called TNAC (Total Number of Allowances in Circulation) – falls below 400m (as of December 31, 2024, the TNAC stood at 1,148m). Moreover, the rate of release is currently restricted to 100m per year once the 400m TNAC figure is breached, so the Commission might also look to change this in order to make the MSR more flexible in responding to price spikes. Again, however, according to this morning’s Bloomberg story, the Commission will not propose any change either to the TNAC threshold for releasing allowances back to the market or the rate at which allowances can be fed back.

Having opened up slightly down this morning EUAs have subsequently rallied on the back of the Bloomberg story (published at 10:47 am CEST), on the logic that the changes to the MSR that the Commission appears set to announce on Wednesday will be restricted to scrapping the invalidation of allowances above 400m such that the intake rate and thresholds for feeding EUAs into and releasing EUAs from the MSR remain unchanged.

If confirmed, this would certainly be a less extensive change to the workings of the MSR than the market had expected until now.

We question whether such a limited proposal for changing the MSR will be enough to satisfy those member states who have been most concerned about the impact of high EUA prices on the EU’s industrial competitiveness. As a result, if this turns out to be what the Commission does in fact propose we think there may yet be more pressure applied by member states to widen the scope of the MSR Review once the co-decision process formally begins.

US news: another quiet week as CCAs await amended ISOR proposals

The Dec-26 CCA contract traded up 21 cents over the course of last week, closing at $29.16/t on March 27. The front-month and spot values traded back above the 2026 floor price of $27.96/t, but overall activity was muted with trading volumes down 10% week-on-week. The market remains subdued as traders await an update from CARB on proposed amendments to the ISOR, and given the high number of comments (>800) in response to the original 45-day consultation period, concerns over affordability – exacerbated by the impact on gasoline prices of the war between the US/Israel and Iran – are weighing on the market.

We still expect CARB to retain the proposed reduction in the cap to 2030 outlined in the ISOR in the face of these pressures, but to show flexibility on the question of free allocations by revising these upwards, particularly for the Refining sector. In order to meet its target of bringing the proposed new regulations for the cap to a Board meeting in late May, CARB will need to publish amendments to the ISOR by mid-April at the latest so that a 15-day consultation period for comments and its response can be accommodated. We expect CCA prices and activity to remain subdued until the amendments are published.

As of the close of business on March 27, the year-to-date performance of the Dec-26 CCA contract was -11%, while for RGAs and WCAs, the equivalent contracts were down 8% and -9%, respectively, YTD.

Carbon Market Roundup

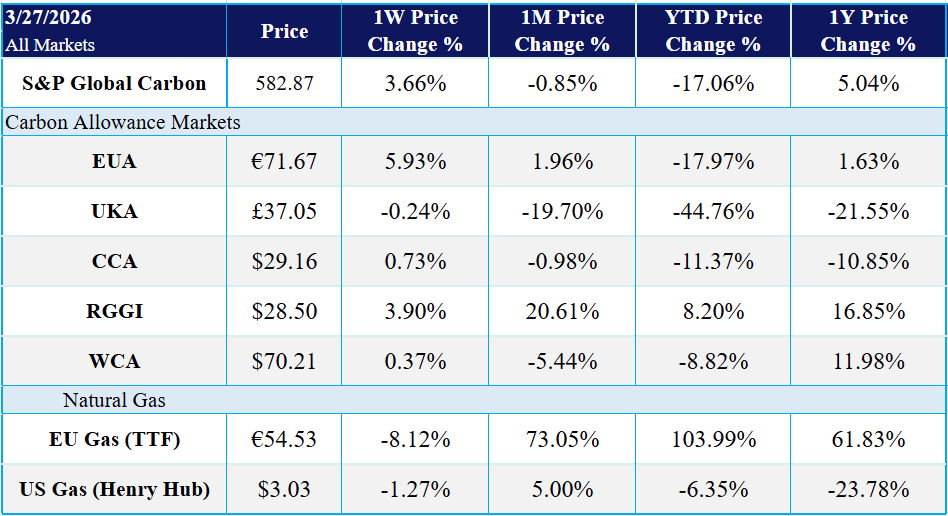

The weighted global price of carbon rebounded over the week, ending at $50.39 last Friday, up 3.66%. EUAs rose to €71.67, gaining 5.93% on the week, while UKAs edged lower to £37.05, down 0.24%. In North America, CCA prices increased to $29.16, up 0.73%, and RGGI allowances advanced to $28.50, rising 3.90%. WCA rose slightly, up 0.37% over the period to close at $70.21.

1 The other proposed measures announced by Von der Leyen on 20 March will come in May/June as part of the EU-ETS review, the main ones being: i) an extension of free allowances to industry beyond 2034, and hence a revision to the current timeframe for the full phaseout of free allowances; ii) a lower Linear Reduction Factor for the EU-ETS cap, probably from 2031 onwards, and iii) an ‘investment booster’ of €30 billion for industry to invest in low-carbon technologies, to be financed via the sale of 400m EUAs.

2 For more on the background to this measure, see our blogpost of 18 February, Searching for the Signal: Making Sense of Last Week’s EU and US Policy Noise

3 See the Bloomberg story EU Short-Term Carbon Amendment Won’t change Reserve Parameters