EU Summit Brings Relief for EUAs, All Quiet on the Western (Climate Initiative) Front

5 Min. Read Time

EUAs ended the week higher, despite ongoing energy market volatility following Iran’s closure of the Strait of Hormuz. The market saw a boost from key updates coming out of the EU Council in Brussels, which helped calm recent political debate and provide clarity on the path of the EU ETS reform.

In the US, it has been a relatively quiet week across all three compliance markets following recent auctions, though pressure in CCAs persists as the market awaits guidance on potential revisions after the rulemaking public comment period.

EUAs bouncing today despite continued spike in the benchmark EU natural-gas price

After hitting a YTD low of €63.07/t yesterday (and the lowest price since April 11 last year), the Dec-26 EUA contract is bouncing hard today, having traded as high as €69.8/t on relief that the outcome of the EU Council in Brussels appears to have resulted in decisions consistent with the more thoughtful interventions made in recent weeks by technocrats such as Jos Delbeke and Peter Liese rather than with some of the more populist interventions from the leaders of certain EU member states. Specifically, EU Commission President Ursula von der Leyen has outlined four major conclusions from the summit.1

These four measures are as follows: i) to update the benchmarks determining the free allocation of EUAs to industry in a less aggressive way than originally intended, thereby giving industry more free allowances over 2026-30 than previously expected; ii) to give the Market Stability Reserve (MSR) ‘more firepower’ for the future; iii) an extension of free allowances to industry beyond 2034, and hence a revision to the current timeframe for the full phaseout of free allowances; iv) an ‘investment booster’ of €30 billion for industry to invest in low-carbon technologies, to be financed via the sale of 400m EUAs (implying an average price of €75/t).

Von der Leyen said that details regarding the first two measures would come ‘in the next few days’, while the third and fourth measures would be discussed under the EU-ETS review later in the year. The EU-ETS Review is scheduled to start in Q3, but given the intense political pressure to provide relief for industry on energy prices, we think this may now be brought forward to May or June.

Overall, what does all this mean, and what, if anything in all of this, is actually new?

As far as the benchmarks are concerned, this is not new, as it has been widely expected for weeks now that the Commission would come forward with more generous terms to take some of the pressure off industry. The open question is how much more generous these benchmarks will be for particular industrial sectors and sub-sectors. However, while this will obviously be very important for the relevant industries themselves, it should not really have any bearing on EUA prices as, in the end, this is about how the same number of overall EUAs are distributed – for free or via auction – rather than about the total amount of supply available to the market.

Regarding ‘more firepower’ for the MSR, we highlighted in our blogpost of February 18 the suggestion from former senior Commission official Jos Delbeke that the provision whereby the number of allowances in the MSR is capped at 400m EUAs and any allowances above that number are cancelled every year should be scrapped from 2027 so that the MSR could build up a larger supply of allowances to be used to curb future price spikes. We expect this to be the Commission’s confirmed policy proposal in the next couple of weeks.

In terms of extending the phaseout of fee allowances beyond 2034, this was first publicly proposed by the prominent Member of the European Parliament Peter Liese, as we explained in our blogpost of February 11.

We would expect this measure to be accompanied by a lower Linear Reduction Factor (LRF) as well, as also first proposed by Liese, and as also explained in our blog on February 10. However, these measures will form part of the EU-ETS Review and will therefore most likely not have any implications for either the trajectory of free allowances or the cap before 2031.

Finally, there are still no details on where the 400m EUAs will come from to finance the so-called ‘investment booster’ of €30bn for industry to invest in low-carbon technologies, other than from ‘existing reserves’. In our view, this means von der Leyen is most likely referring to the allowances set aside in the so-called Cross-Sectoral Correction Factor (CSCF) buffer (379m in total), and again, this was originally a suggestion made by Jos Delbeke in an interview with Bloomberg on February 5, as explained in our blogpost on that day.

Overall, these four measures do not amount to any significant new information for the market, although it is fair to say that we await confirmation on certain important details, most notably on exactly where the 400m allowances to finance the €30bn ‘investment booster’ will come from, and over what timeframe and exactly how they will be allocated. The key point for the time being, though, is that there was nothing more radical agreed to at the EU Council that would have given the market cause to doubt the EU’s long-term commitment to maintaining a robust and viable market, and that is why we think EUA prices are bouncing hard today.

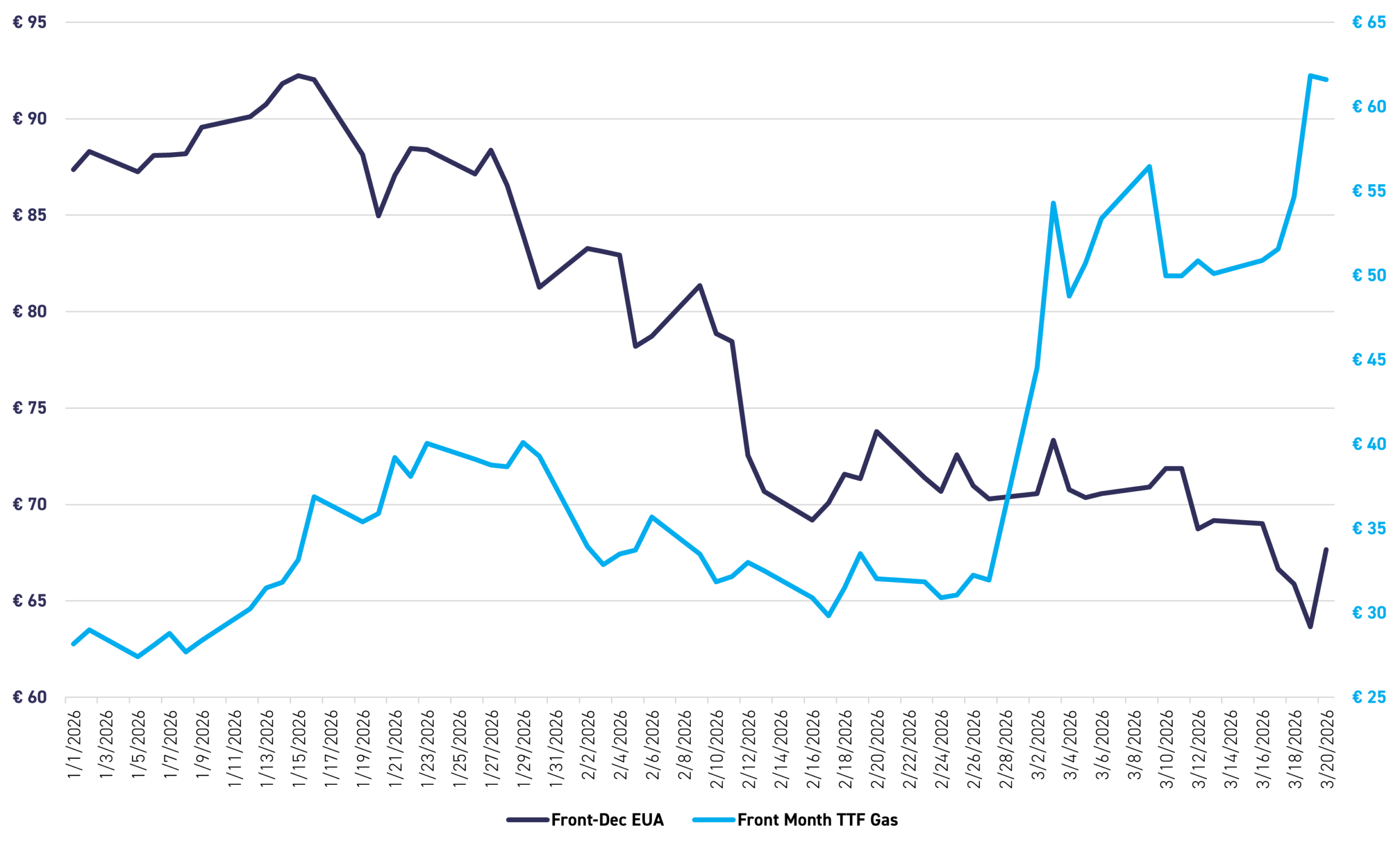

All of that being said, the one caveat in all of this is the rapidly deteriorating situation in global energy markets, with European TTF (Title Transfer Facility) natural-gas prices spiking again this week on further significant damage to energy-production facilities in the Gulf and in Iran. Figure 1 shows the price of the Dec-26 EUA contract versus the front-month TTF contract since January 1, with TTF prices of €61/MWh now more than double the level they were trading at only one month ago, and six times higher than US natural-gas prices.

Figure 1: Front-Dec EUA (LHS, €/tonne) versus Front-Month TTF (RHS, €/MWh) Jan 1 - March 20, 2026

Source: Bloomberg

As a result, while today’s relief rally is understandable given the result of the EU Council meeting, there could yet be further political pressure to come when the EU-ETS Review launches in late Q2/early Q3 if TTF prices spike further over the next couple of months and this then prompts further warnings from EU industry about high energy prices and their impact on European industrial competitiveness.

US news: a quiet week but CCAs remain subdued

The Dec-26 CCA contract traded down 8 cents over the course of the week as of March 18, closing at $28.87/t. The front-month and spot values are currently both slightly below the 2026 floor price of $27.96/t, with the market currently being held back by jitters over the high number of comments (>800) in response to the 45-day consultation period over the ISOR rulemaking draft, high gasoline prices in reaction to the war between the US/Israel and Iran (>$5/gallon), comments from Chevron and others about the pressure on Californian refineries, and a letter from 15 Democrats in the California assembly about affordability concerns.

We do not ultimately expect CARB to change the proposed reduction in the cap to 2030 outlined in the ISOR in the face of these pressures, but we do think it is likely that CARB will revise free allocations upwards. Accordingly, we think it likely that CARB will publish amendments to the ISOR in the near future, to be followed by a 15-day consultation period for comments, such that the revised version can still be presented to the Board in May.

- As reported by Carbon Pulse here.

Carbon Market Roundup

As of market close on March 19, the weighted global price of carbon closed at $46.90, down 3.80% week-over-week. EUAs fell to €63.65, a 7.39% weekly drop, while UKAs closed at £34.67, down 12.82%. In North America, CCA prices eased to $28.88, off 0.31% on the week, while RGGI allowances jumped to $28.03, gaining 14.64%. WCA also firmed, ending at $69.57, up 2.31% over the period.