EU-ETS Emissions Down Slightly in 2025, RGAs up on Virginia’s Bid to Rejoin RGGI

By Mark Lewis

4 Min. Read Time

With the long Easter holiday weekend followed by the ceasefire announcement between the US/Israel and Iran on Wednesday morning, the price action in EUAs has been stable over the last week. Yesterday saw the publication of the EU-ETS Verified Emissions Data (VED) for 2025, which, after extrapolating for the residual emissions not yet published, appears to show a year-on-year reduction of 1.5%, slightly softer than consensus expectations. In the US, the stand-out market over the last two weeks has been RGGI, with RGAs up over 20% since mid-March on Virginia’s bid to rejoin the scheme as of July 1.

EUAs stable over last 10 days as 2025 verified emissions data comes in slightly soft

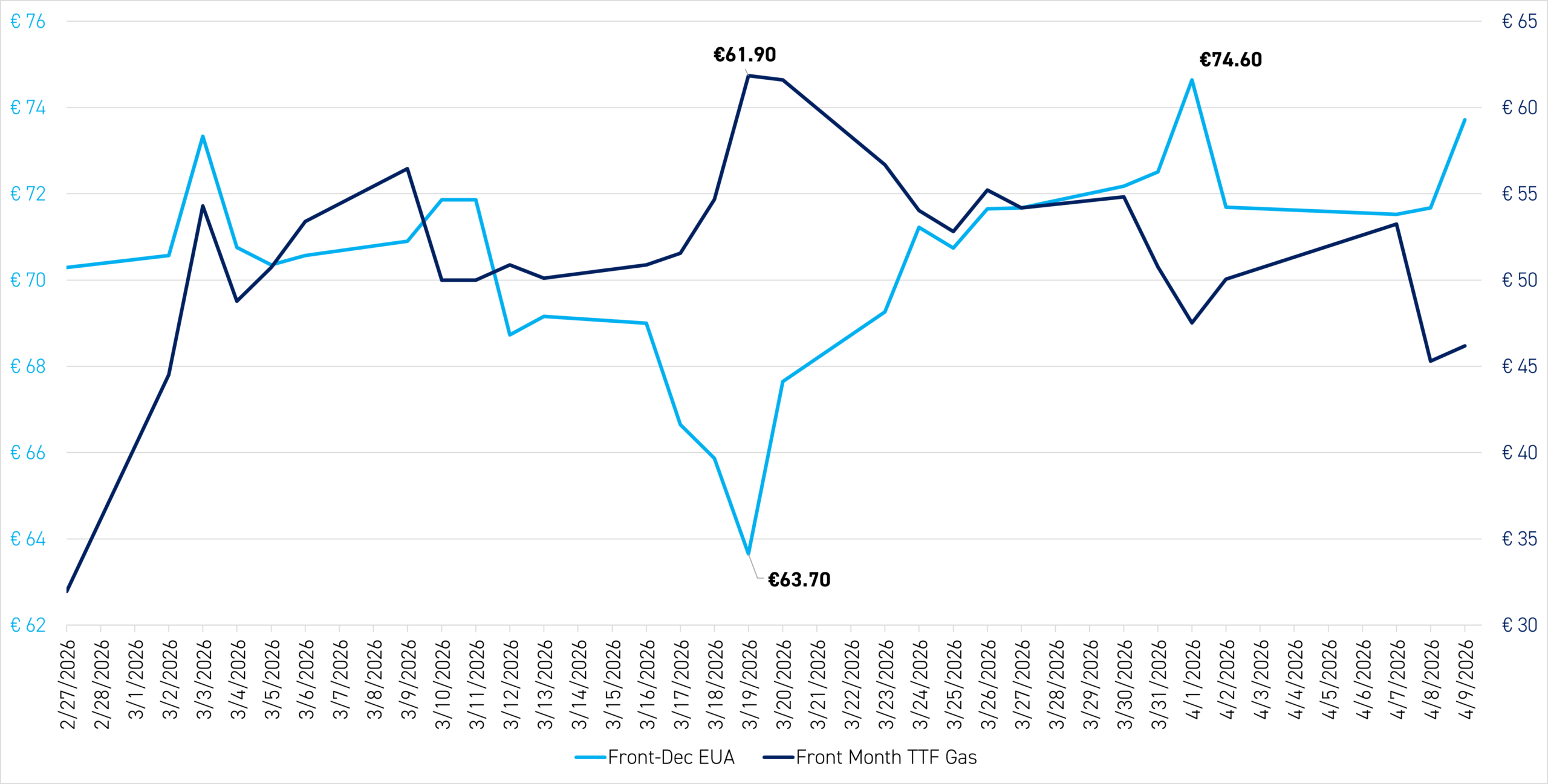

Figure 1 shows the Dec-26 EUA contract against the front-month TTF contract since the outbreak of hostilities between the US/Israel and Iran on February 28. EUAs have traded in a range of €63-€75/t over this period, reflecting two related shocks to the market. First, there has been the conflict itself and the impact this has had on energy prices, particularly EU natural-gas prices; second, the political reaction to this, with the EU Commission announcing changes to the workings of the Market Stability Reserve (MSR) and an accelerated timeframe for the EU-ETS Review with a view to calming the fears of EU industry over energy costs and competitiveness.

Figure 1: Front-Dec EUA (LHS, €/t) versus Front-Month TTF (RHS, €/MWh) Feb 27- March 27, 2026

Source: Bloomberg

As explained in our last blog, there is a strong inverse correlation between EUAs and TTF, reflecting the fact that the higher the TTF price goes, the greater the pressure on EU industry, and hence the greater the perceived political pressure to intervene in the carbon market. It is therefore no coincidence that the highest closing price for TTF year-to-date so far of €61.8/MWh on March 19 coincided with the lowest closing price YTD for EUAs of €63.7/t.

With the announcement of a two-week ceasefire on Wednesday bringing relief to global energy markets, TTF has fallen back to €46/MWh as of COB last night, down 13% from the COB on Tuesday before the ceasefire deal was announced – EUAs have therefore perked up, and are now up 16% from the low of €63.7/t of 19 March.

A second source of relief for EUAs has been the weaker-than-expected regulatory reaction – so far at least – to the pressure on EU industry as far as reforms of the EU-ETS are concerned. Last week, the market had been expecting that the Commission would propose both new and more generous free-allocation benchmarks for industry and a range of possible reforms to the MSR, but in the end, the publication of the benchmarks was postponed, and the MSR proposal was less ambitious than expected.

On the MSR reform, the Commission proposed that the current rule whereby the number of allowances in the MSR is capped at 400m EUAs and any allowances above that number are cancelled every year will be scrapped from 2027, thus allowing the MSR to build up a larger supply of allowances for smoothing future price spikes. However, the Commission did not propose changing the annual intake rate from the current 24% to 12%, nor did it put forward any change to the threshold below which it releases allowances back to the market.

We remain sceptical that such a limited proposal for changing the MSR will be enough to satisfy those member states who have been most concerned about the impact of high EUA prices on the EU’s industrial competitiveness, and we note that the Commission has reserved the right to propose further changes to the MSR as part of the broader EU-ETS Review, which is now expected to be launched in June. For now, though, the ceasefire between the US/Israel and Iran and the limited MSR proposal have calmed market nerves.

Meanwhile, yesterday saw the publication of the 2025 VED for the EU-ETS. With 93% of total emissions reported (95% of all stationary installations, 92% of aviation operators, 65% of maritime operators), and assuming the same trends hold across the entities that have not yet reported as have been registered by their peers who have, we estimate that the final tally will come in at 1,143Mt. This is only 10Mt lower than our own estimate of 1,153Mt, and 23Mt lower than the consensus number reported by Carbon Pulse on April 1,1 and would represent a like-for-like reduction versus 2024 of 1.7%.

US news: RGAs take all the headlines as Virginia seeks to rejoin RGGI in July

With CCAs still in a holding pattern close to the 2026 price floor as the market awaits the publication of the amended ISOR, the focus over the last couple of weeks has been on RGAs, which have received a strong boost from Virginia’s bid to rejoin RGGI as of July 1. Virginia’s emissions have risen sharply over the last couple of years on the back of surging power demand from data centres and increased gas-fired power generation, and the state looks set for a significant supply deficit this year. Clear Blue Markets estimates Virginia will have a full-year deficit of 3.3m short tons versus a forecast 2026 surplus for RGGI without Virginia of 0.6m short tons. This means that even though Virginia is looking to join halfway through the year, its addition as of July 1 would flip RGGI overall into deficit in 2026.

The prospect of additional tightness in RGGI this year pushed RGAs to a new all-time high closing price of $30.14/short ton on April 7. However, we would caution that this is not a done deal yet, as the other member states in RGGI would need to approve Virginia’s entry and may be reluctant to admit it halfway through the year, particularly with the extra tightness this would add to the system. As a result, we think it is more realistic that Virginia will rejoin as of January 1, 2027.

As of the close of business on April 8, the Dec-26 CCA contract was down 12% YTD, while RGAs were up 12% and WCAs down -9%.

- See the Carbon Pulse article, EU-ETS emissions seen modestly weaker in 2025 as weather, weak industry offset transport gains.