Energy & Politics Create Volatility for EUAs Ahead of Key EU Summit, Plus Washington and RGGI Auction Results

4 Min. Read Time

Global headlines this week have been dominated by Iran’s closure of the Strait of Hormuz and the ramifications this will have for the supply of Oil and Liquefied Natural Gas (LNG), the longer the strait remains closed. The EU is particularly dependent on LNG imports, and the benchmark TTF natural-gas contract has therefore been extremely volatile all week, and is now trading a €50/MWh, 60% higher than it was before the outbreak of hostilities between the US/Israel and Iran two weeks ago. The volatility in TTF has been mirrored in EUA prices, with EUAs trading higher earlier this week but then selling off yesterday on a Bloomberg story stating that the forthcoming EU Council meeting next week (March 19-20) will include a discussion about how the Market Stability Reserve (MSR) in the EU-ETS might be used to control prices in the future.

In the US, the results of the Q1 Washington auction were announced, with the clearing price coming in at the Tier-1 Allowance Price Containment Reserve (APCR) level of $65.26/t, while the results of the Q1 RGGI auction have just been released and look surprisingly strong at first glance.

Rising EU energy prices increase political pressure on the EU-ETS ahead of the EU Summit

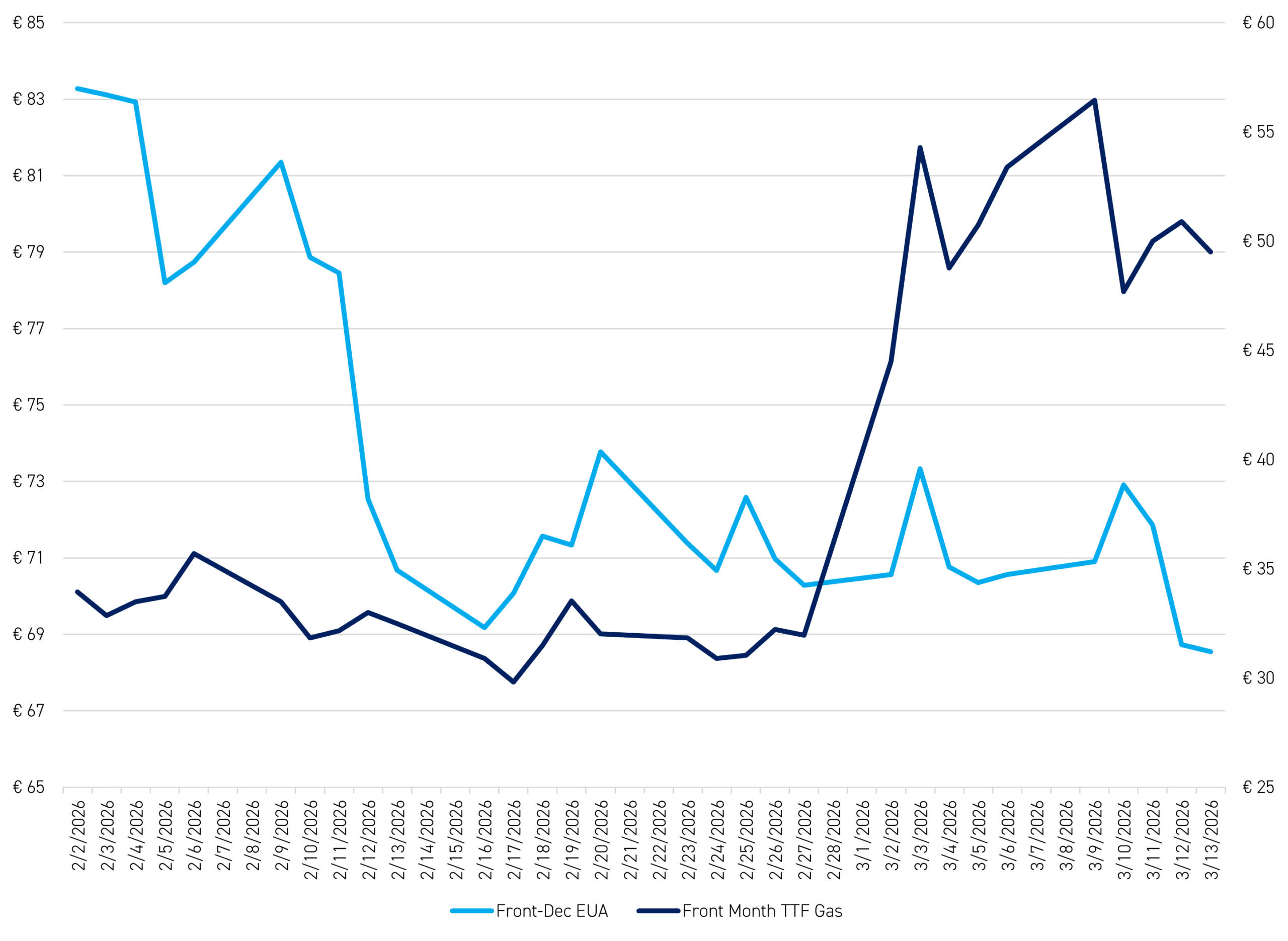

Figure 1 shows the price of the Dec-26 EUA contract versus the front-month TTF contract since February 1, with the violent spike in the TTF price on Monday, March 2, in reaction to the eruption of kinetic conflict between the US/Israel and Iran over the previous weekend clearly visible. As we noted in last week’s blog, EUAs held up well last week against this upsurge in nat gas TTF prices and were strong for the first part of this week as well, with traders bidding up carbon on the reflex ‘fuel-switching’ notion that higher gas prices means that higher carbon prices are needed to push natural-gas power generation ahead of coal-fired power on the grid.

Figure 1: Front-Dec EUA (LHS, €/tonne) versus Front-Month TTF (RHS, €/MWh) 1 Feb-13 March 2026

Source: Bloomberg

Yesterday, however, EUA prices dropped 4.5% after a Bloomberg story indicated that next week’s EU Council meeting will focus on the bloc’s energy crisis, mentioning specific measures likely to be floated for the forthcoming reviews of both the EU-ETS and the MSR with a view to reducing EUA prices.1

Here is the relevant paragraph from the Bloomberg story, which appears to have prompted yesterday’s sell-off:

While next week’s summit is not expected to produce a final decision on energy measures, leaders will attempt to give the Commission marching orders on which proposals to pursue. Those may include a fast-tracked revision of a carbon market mechanism, which automatically controls the supply of emissions permits. Under this plan, the so-called Market Stability Reserve, which withholds extra pollution allowances from circulation, would be recalibrated to lower the intake rate and reduce short-term price spikes.

We have consistently highlighted the growing policy risk in our recent blogs and are therefore not surprised to see heightened policy attention being given to the potential for using the MSR as a price-control mechanism – indeed, we expect this to be a central focus of the MSR Review later in the year. After all, the reality is that as a large net importer of oil and natural gas, the EU is at the mercy of geopolitical events such that the longer the Strait of Hormuz remains closed, the greater the policy imperative of reducing other energy-input costs – such as carbon – will become. Next week’s EU Summit will therefore be a key event in terms of offering clues as to the areas the Commission and member states will want to focus on in reforming the EU-ETS and the MSR later in the year.

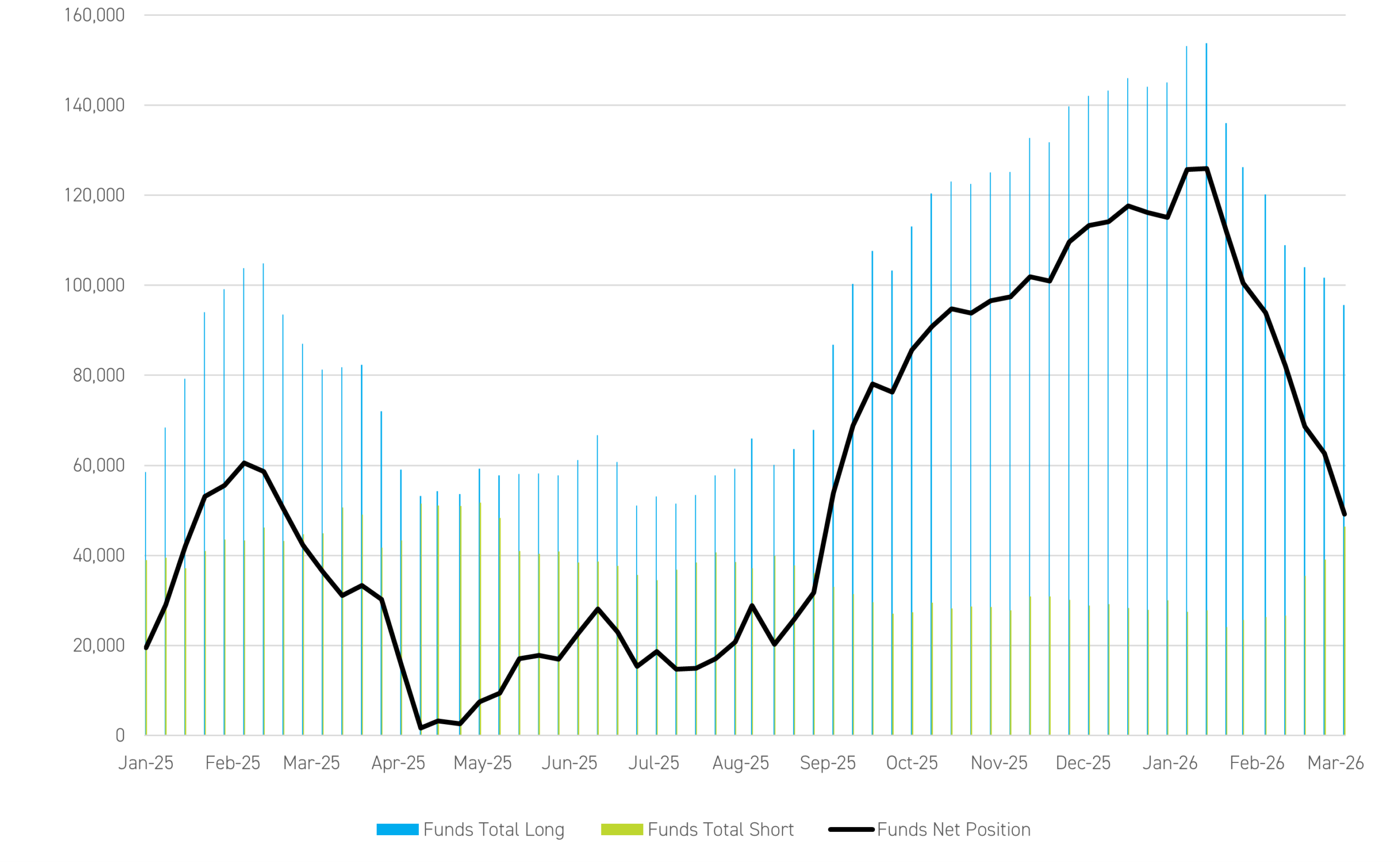

One other thing to note about EUAs this week has been the further reduction in speculative holdings, with net speculative length falling by another 13.5Mt to stand at 49.2Mt as of March \ 6, the lowest level since August 29, 2025 (Figure 2).

Figure 2: Net speculative holdings of EUAs, 1 January 2025-6 March 2026 (Kt)

Source: ICE

In theory, this should make for less volatility going forward, but with policy risk now the most important price driver in the short term, we would not be surprised to see net speculative length drop further in the coming weeks.

US news: Q1 auctions in Washington and RGGI

The results of Washington’s Q1 auction were released on Wednesday, with the price clearing at exactly the Level of the Tier-1 APCR price of $65.26/t, well below both the Vintage-26 Mar-26 price on the day the auction was held (March 4) of $72.65/t and the Q4-2025 clearing price of $70.86/t. The total number of allowances sold was 5.31 million, and the cover ratio was 1.76, down from the 1.94 recorded in Q4-2025. With the clearing price in line with the Tier-1 APCR price, we now expect another APCR auction in May, and for the notice for that to be issued today (March 13).

Washington floated a draft agreement for linking its market with the Western Climate Initiative on 3 March and has set dates for public workshops next month. However, getting linkage in place by the deadline of the first Compliance Period (November 1, 2027) appears ambitious, as it depends on the California-Quebec Program Review timeline.

Meanwhile, the results of the Q1 RGGI auction have just been released and look to have surprised to the upside. The auction cleared at $24.99, a 5.6% premium over the spot price on auction day despite increased volumes and the refilled CCR pool. The cover ratio of 3.3 (excluding CCR allowances), the highest since March 2025. This ratio implies a demand of 60 million allowances, representing approximately 73% of a year’s emissions—a sharp increase from the 37 million implied in December. With momentum building for Virginia to rejoin the scheme later this year, this is a shot in the arm for the RGGI scheme.

As of the close of business on March 12, the year-to-date performance of the Dec-26 contracts for both CCAs and WCAs was -12%, while RGAs have so far this year achieved a slightly stronger -7%.

- See Climate Market Now, 4 March 2026 (EUAs Holding Up So Far Against EU Natural-Gas Spike, CCA Q1-Auction Clears at Floor).

- See here for the Bloomberg Story: EU Weighs Looser Carbon Rules, State Aid to Cut Energy Costs. The EU-ETS Review and the separate MSR Review will both begin in Q3 of this year, but the MSR Review is expected to be completed more quickly, possibly by the end of the year.