EUA Prices Show Resilience Despite Tariff News Over the Weekend

3 Min. Read Time

EU Allowance (EUA) prices initially dipped on reports that the U.S. may impose a 30% tariff on certain EU goods starting August 1st, a potential headwind for European industrials. However, the market quickly recovered as buying activity picked up after prices dipped below €70. EUAs then began tracking the TTF nat gas prices more closely, slipping slightly lower in the afternoon.

Last week, after President Trump indicated that the deadline for the talks with the EU, and a number of other countries had been postponed to August, the market absorbed the news calmly, with prices trading between €71.99 and €69.89 in the first half of the week, effectively maintaining the EU ETS in the narrow €70-€75 channel that it has occupied since the start of May. The on-again, off-again trade talks and tariff threats have weighed on the market and it will likely take an agreement to push prices out of their current range.

More fundamentally, European carbon has seen little to move the needle either. While summer temperatures have risen to as much as 10 degrees Celsius above normal for the time of year, solar generation, and to a smaller extent wind, have managed to cover much of the additional demand for power for cooling. This has also lessened the burden on hydropower, where reserves are below their ten-year average levels for the time of year.

For industry, the outlook is also fairly neutral. Industrial output across the 20 Eurozone countries has begun to tick upwards; year-on-year output increased in February, March, and April after a solid 18 months of negative monthly figures. The recent improvement, however, is seen as vulnerable to the potential imposition of higher US tariffs if a trade deal fails to be reached, with steel and aluminum expected to bear the brunt of any higher levies, and this could dampen the output data going forward.

These factors have combined to keep the EUA market trading in a tight range. Typical daily high-low ranges began the year at in excess of €2.00, but have fallen steadily to where they were as little as €1.05. Likewise, the front-December futures contract started the year trading an average of 31.5 million EUAs a day in the first quarter, but volume slumped to 25 Mt in May and 28 Mt in June. For July it’s even less: less than 19 Mt a day has gone through on the ICE exchange. But these numbers are generally expected to reverse as the second half of the year unfurls, and particularly the fourth quarter.

With the compliance season expected to show up in growing daily volumes over the summer, and the onset of winter heating season expected to spur demand for EUAs as utilities hedge forward generation, EUAs are generally predicted to rally into the end of 2025.

Some of this recovery is also attributed to the end of the REPowerEU sales program, which is scheduled to terminate in the summer of 2026. The EU has sold nearly 60% of the budgeted 250 million EUAs since the summer of 2023, and has raised more than €11 billion of its €20 billion goal. REPowerEU has raised around €900 million less than it was programmed to, mainly due to lower-than-budgeted EUA prices, and there remains a possibility that additional sales may be scheduled to make up this shortfall. Nevertheless, once the REPowerEU sales stop, the market will flip to become tighter, as those 250 million (or more) allowances have been “borrowed” from future years’ auction schedules.

The shift will coincide with a tightening of the benchmarks that determine free allocation to industrial plants, thereby reducing the number of EUAs handed out each spring. This will bring more industrials into the market to cover their needs.

First up, though, will be the updating of the auction program for the rest of 2025. The most recent Total Number of Allowances in Circulation (TNAC) calculation in May determines the Market Stability Reserve’s annual siphoning-off of 24% of the market surplus and will be reflected in an adjusted sales program.

From September 2025 until August 2026, the MSR will remove 276 million EUAs from circulation by cutting the auction program by that amount. That’s 10 million more than were removed from September 2024 to August 2025, and 4 million more than were removed from 2023 to 2024. The updated auction schedule will be published by the EEX exchange later this month. Traders will also be watching to see whether the European Commission may extend the REPowerEU program to make up some of the shortfall.

Carbon Market Roundup

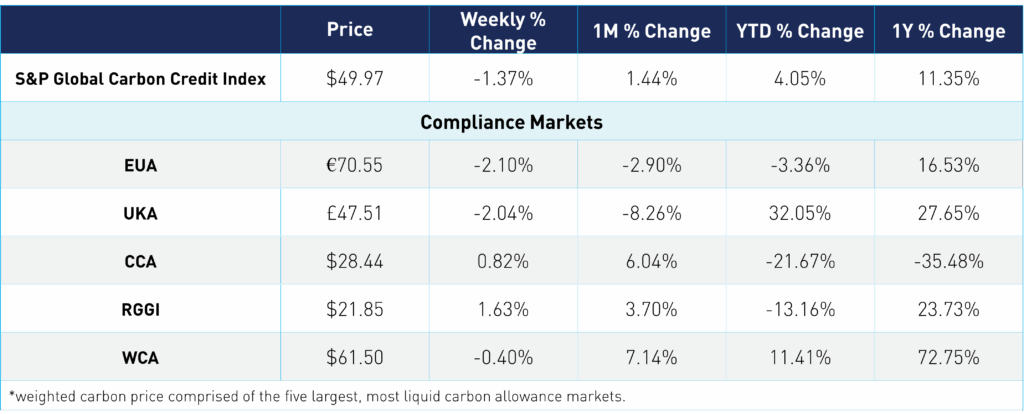

The weighted global price of carbon was $49.97, down 1.4% week over week. EUAs closed last Friday at €70.55, down 2.1% for the week. UKAs were down 2.0% at £47.51. CCAs ended up 0.8% at $28.44. RGGI was also up 1.6% at $21.85. WCAs were down slightly at 0.4% at $61.50.