Strong CCA Reauthorization Signal with Latest Draft Proposal Release, EUAs Boosted by Natural Gas

4 Min. Read Time

The state of California's carbon market is finally on the move. Draft proposals for AB 1207 California cap and trade were released earlier last week. The main highlights are the re-addition of the formal extension to 2045 and the introduction of an Emissions Containment Reserve (ECR) to tighten supply in low-demand auctions. Politico released the revised provisions here, though we've summarized the main points below.

- Extend the program to end of 2045 (reintroduced after previously removed from AB1207 in May)

- Establish Emissions Containment Reserve (ECR) that would permanently withhold allowances when the auction clearing price is below the trigger level (halfway between the auction reserve price and tier 1 level)

- Expands offsets use to a max of 10% of compliance obligations if they bring in nature-based solutions from Native American nations (4%) or use carbon removal (CDR) technology (2%)

The program extension is the main selling point as the market's supply/demand balance is already on a strong tightening schedule. The ECR would help support higher CCA prices though could face pushback from those concerned with the priority issue of affordability. Considering there is talk that RGGI is planning to remove their ECR and replace it with an increased minimum reserve price, it further reinforices the chance that it may not see approval in California. Offset use is another controversial item and with an increase to 10% from the current 4% limit, it's uncertain if we'll see unviversal approval. Regardless, this is a strong reauthorization bill and we are keeping an eye out for further details ahead of the conclusion of the legislative session mid-September.

What is an ECR?

- If triggered, ECR removes predetermined portion of allowances, withheld allowances would be transferred into the ECR for permanent retirement, serving as a downward adjustment tool (rules-based approach to supply adjustment).

- Trigger price set halfway between the auction reserve price and Tier 1, i.e., in 2025 the trigger would be $43.

- If introducing an ECR interferes with linkage with other jurisdictions, CARB can choose not to implement.

- RGGI ECR example: if triggered, the ECR has up to an annual withholding limit of 10% of the emission budgets (i.e., the share of each state in the regional cap) of participating states. Allowances withheld will not be re-offered for sale, effectively adjusting the cap downward. The trigger price is $7.86, increasing by 7% per year thereafter. Maine and New Hampshire do not participate in the ECR.

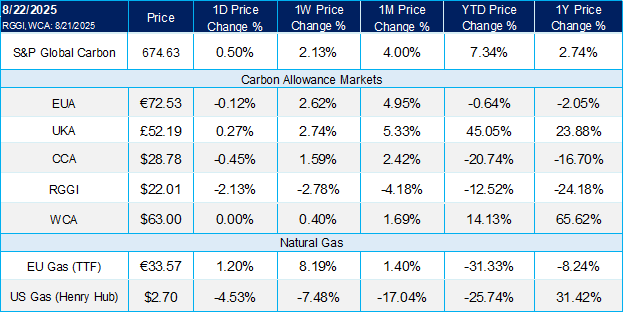

Meanwhile, California’s third quarterly auction of the year took place last week, with the results scheduled to be posted this Wednesday. Stay tuned for the next blog on coverage of the auction. December 2025 CCA futures closed on Thursday at $29.16/tonne on ICE Futures, the highest level in more than a week.

EUA Update

European carbon prices consolidated in the week ending August 22, with the Dec-25 futures contract posting a 2.6% weekly gain to end at €72.53. The front-December contract was supported by strengthening natural gas prices as the atmosphere in Ukraine worsened after President Trump appeared to take a back seat in the peace negotiations, while Russia and Ukraine continued to carry out attacks.

TTF prices (European natural gas benchmark) had dropped steeply in the previous week on a wave of optimism that the Russia-US summit in Alaska, and the following Ukraine-US talks in Washington DC were leading towards a ceasefire and potentially even peace talks between Moscow and Kyiv.

Any agreement to end the conflict would bring with it the prospect of sanctions on Russian gas being lifted, and September TTF had fallen 15% in the ten days leading up to Monday’s Washington meeting. The optimism was reflected in a Citibank analyst forecast calling for Russian gas shipments to resume before the end of 2025, and for the TTF price to average just €29/MWh in 2026.

Yet there are many who believe that Europe’s pivot away from Russian gas will not be halted. They concede that a peace deal will probably mean lower gas prices for the region, but not from a resumption in Russian shipments: instead, Russian gas exports will displace other sources, who will in turn find their way to Europe to complete with US LNG cargoes.

While TTF gas prices fell, EUAs on the other hand remained steadfast at between €70.25 and €73.00 over the same period, finding buying support from compliance entities whenever the price neared €70.00, but equally seeing selling pressure whenever the market neared €73.00.

This state of affairs has not substantially changed, with Friday seeing carbon prices top out at €72.80, but trading sources have been reporting some positive signs for EUAs, including a strong set of PMI data from Germany, and renewed analyst forecasts that see the market heading higher in Q4.

Numerous stakeholders are also seeing increased likelihood that EUA and natural gas prices will start to diverge, and that the correlation that has seen the two markets move in lock-step this year will begin to ease.

With the winter demand season on the horizon and EU countries still working to refill gas storages ahead of the October-December deadline, there is potential for gas prices to rally strongly, but traders point out that with Asian demand for LNG not picking up at the moment, most cargoes are heading to Europe and this is keeping the summer price down and the flow into storage steady.

At the same time, low gas prices are good news for European manufacturers, as it supports increased output and perhaps demand for EUAs from relevant sectors.

Carbon Market Roundup

The weighted global price of carbon was $51.34, up 2.1% week over week. EUAs moved 2.6% higher over the week to close at €72.53. UKAs were also up for the week, +2.7% to end at £52.19. CCAs were up 1.6% at $28.78. RGGI was down 2.8% at $22.01 while WCA was up 0.4% at $63.00.