EUAs Holding Up So Far Against EU Natural-Gas Spike, CCA Q1-Auction Clears at Floor

5 Min. Read Time

EUAs closed last week at €70.29/t, down -4.8% on the week, -13.5% for the month of February, and -20% the year to date. Meanwhile, the outbreak of war between the US/Israel and Iran over the weekend further complicates an already highly strained energy situation for the EU, and the impact on EU natural-gas prices is now the key thing to watch in the run-up to the EU Council meeting on March 19-20. In the US, the results of the Q1 California auction were mixed: all the allowances on offer were absorbed (including the additional supply from the undersubscribed May 2025 auction), but, as was largely expected, the auction cleared at the 2026 floor price of $27.94, and the Dec-26 contract has traded sideways over the last week since the results were announced.

EUAs: TTF price spike complicates an already difficult forthcoming EU Council Summit

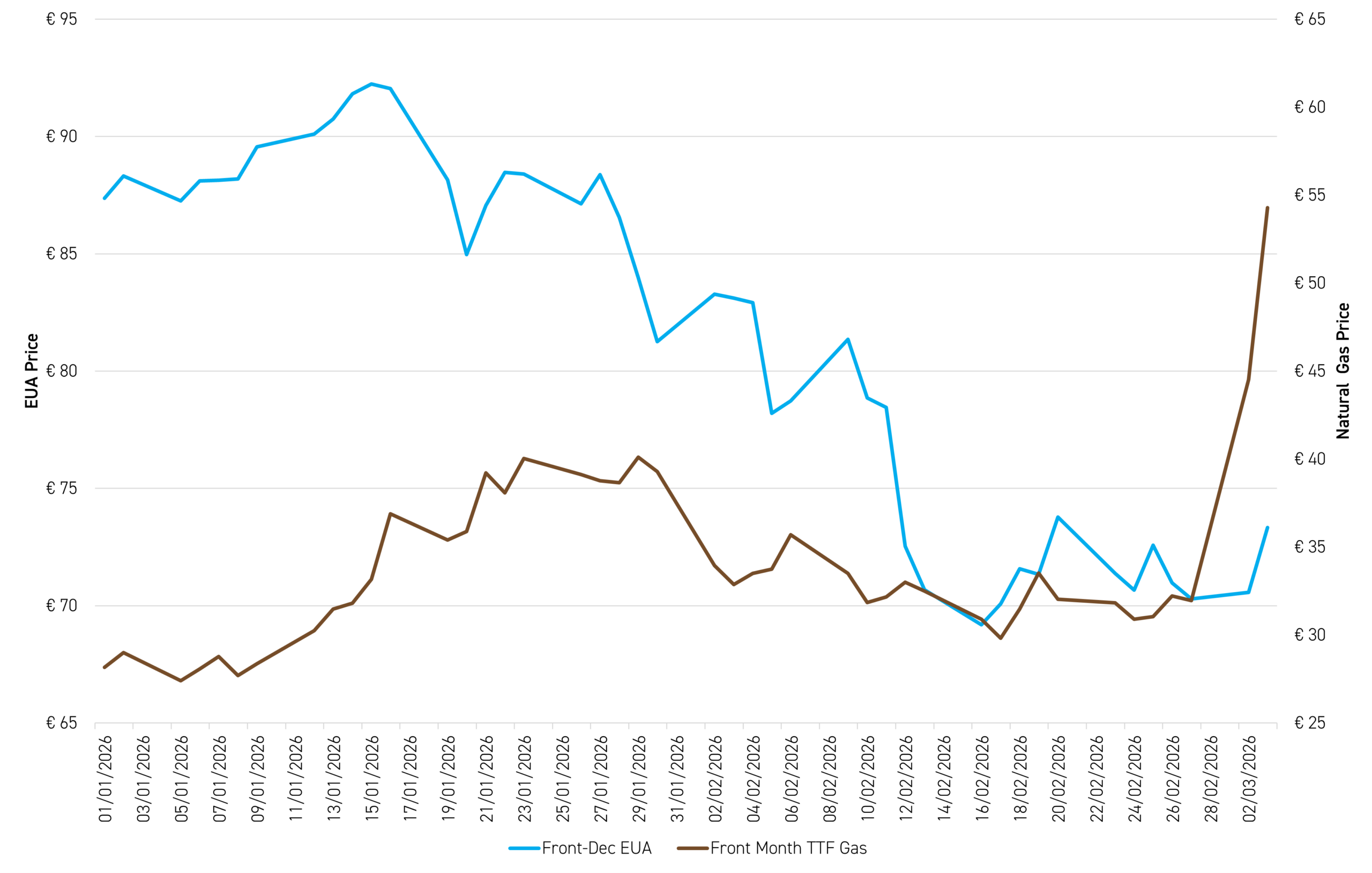

Figure 1 shows the benchmark Dec-26 EUA contract versus the benchmark front-month EU natural gas price (TTF, Title Transfer Facility) year to date, with the violent spike in TTF on March 2-3 following the outbreak of hostilities between the US/Israel and Iran over the weekend clearly visible.

Figure 1: Front-Dec EUA, LHS (€/tonne) versus Front-Month TTF, RHS (€MWh), Jan 1 - March 3, 2026

Source: Bloomberg

With Iran announcing over the weekend that it would impose a blockade on the Straits of Hormuz – the key sea-borne passageway through which 20% of both global oil and global LNG flows pass daily – oil and natural-gas prices spiked violently on Monday, but TTF spiked harder than anything else. Front-month Brent crude was up 7% on Monday, and a further 5% on Tuesday, but front-month TTF rose 40% on Tuesday and a further 22% on Tuesday, to close up 70% versus COB on Friday.1

At the same time, EUAs actually traded higher over the last two days, closing yesterday (Tuesday) at €73.33/t, up 4.3% versus Friday. The rise in EUAs yesterday reflected the fact that at a TTF price above €50/MWh, natural gas becomes prohibitively expensive as a fuel for power generation, which brings coal back ahead of gas in the merit order and thereby increases the demand for EUAs.

However, any short-term benefit to EUA prices from higher coal burn in the power sector risks being outweighed by the increased political pressure that will undoubtedly be brought to bear on the EU carbon market by this most recent spike in TTF prices.

As explained in our recent blogposts2, there has already been a barrage of policy noise in recent weeks on the EU-ETS, reflecting heightened focus among EU policymakers and politicians on high EU energy prices. The price of natural gas is the single largest source of concern as it is both a direct feedstock in its own right for EU industry, and an indirect cost input via its impact on EU power prices. However, whereas EU policymakers and politicians have no control over the price of natural gas, they can revise the EU-ETS policy.

And, there will be two crucial policy reviews starting in Q3 of this year, namely the EU-ETS Review and the Market Stability Reserve (MSR) Review. Now more than ever with this current spike in TTF prices, we would expect the forthcoming EU Council meeting on March 19-20 to result in coordinated suggestions for the EU-ETS review to consider: i) an increase in the size of the overall EU-ETS cap beyond 2030, ii) an extension of the cap by a few years beyond 2039 (which is the date by which the cap falls to zero under the current legislation), and iii) an increase in the total amount of free allowances awarded to industry rather than auctioned.

At the same time, we think the EU Council meeting will also produce concrete proposals for the MSR Review. Specifically, we think it is likely that the Commission and Member-State heads of government will request that the MSR Review formally consider allowing a larger number of allowances to be stored in the MSR from 2027 onwards than the 400m at which the MSR is currently capped. This would give the Commission more supply to play with in the future if prices were to exceed a politically acceptable level, especially if the conditions under which allowances in the MSR could be made available to the market were to be loosened as well.

If policy were indeed to develop along these lines during the MSR Review – and we now see this as increasingly inevitable – we would effectively be looking at a more flexible price-control mechanism than the current very cumbersome Article 29a in the ETS Directive (which has never been used in any case), and in our view this is something that should therefore be watched very carefully.

In short, the politics were already hardening towards enabling policymakers to exercise greater oversight and control of prices in the EU-ETS in the future, and the spike in EU gas prices caused by the war between the US/Israel and Iran will only reinforce this trend. The first signs of the emerging new framework should become visible at the EU Council meeting on March 19-20.

CCAs: Q1 auction clears at the floor, speculators on the sidelines

California held its first quarterly auction of the year last week, clearing at the 2026 floor price of €27.94/t. This is the first time that a CCA auction has cleared at the floor price while being fully subscribed, and the price represented a 1.4% discount to the prevailing spot price on the day of the auction. Also of note was the fact that non-compliance entities – i.e., investors – absorbed only 12% of the allowances on offer, their lowest take-up since the Q2 auction in 2022.

Prices traded slightly softer following the auction, with the Dec-26 contract closing the week at $29.45/t, down 1% on the week, 1% on the month, and 9.5% YTD. However, with prices now trading so close to the floor price, we think downside risk is extremely limited, and the market will now look to the conclusion of the initial 45-day comment period on March 9 as the next key date for confirmation that the legislative timetable is still on track.

If this is confirmed, we would expect to see an increase in speculative interest over the rest of March as the tightening foreseen by the ISOR is intrinsically constructive, with the main question being whether the timeframe for implementing it from January 1, 2027, which remains very much our base case, is still feasible.

Carbon Market Roundup

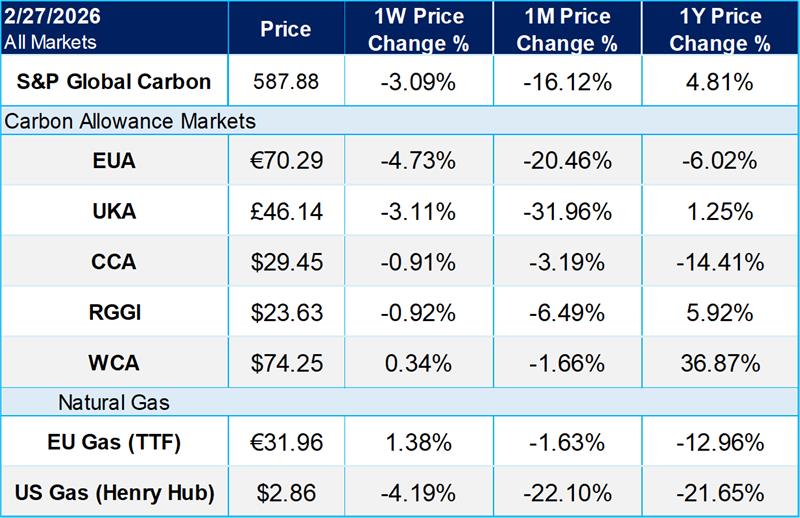

The weighted global price of carbon softened over the week, closing at $50.82, down 3.09%. EUAs fell to €70.29, a 4.73% weekly decline, while UKAs eased to £46.14, down 3.11%. In North America, CCA prices slipped to $29.45, off 0.91% on the week, with RGGI allowances slightly down by 0.92% to $23.63. WCAs held firmly to end at $74.25, up 0.34% over the period.

- For more on this, see the Bloomberg story of 2 March: Gas Prices Surge as Qatar Shuts World’s Largest LNG Export Plant

- See in particular our posts on Climate Market Now of 25 February (EUAs Get Some Relief Ahead of Upcoming Changes, CCAs Await Results of Q1 Auction), 18 February (Searching for the Signal: Making Sense of Last Week’s EU and US Policy Noise), 11 February (Hold Tight! Chancellor Merz adds to EU-ETS policy noise with confused intervention), 10 February (Cool Heads Required as EUAs Face Increased Volatility from Political Risk), and 5 February (EUAs Drop on Bloomberg Story, So What is Going On?).