Q4 Washington Auction Clears at All-Time High, EU Institutions Agree on 2040 Climate Law

3 Min. Read Time

The Q4-2025 WCA current auction cleared at $70.86, which was $6.56 higher (+10%) than the Q3 auction clearing price of $64.30 and a new all-time high (ATH) for a WCA auction settlement. The clearing price was at the upper end of the range of analysts’ expectations of $66.5-71.06, and was significantly above both the first 2025 Allowance Price Containment Reserve (APCR-1) level of $60.43, and the recently released 2026 APCR-1 level of $65.26, reflecting the fundamental tightness in the Washington market.

A total of 7.4m V25 WCAs and 364k V24 WCAs were offered in the current auction, and the cover ratio was 1.96, down from the 2.41 and 2.44 registered in the Q3 and Q2 current auctions, respectively, with compliance entities securing 6.45m of the allowances on offer (87%), and speculators 970k (13%). With the current Q4 V25 auction clearing above the ACPR-1 level of $60.43, the remaining 3.6m WCAs held in the 2025 Tier-1 reserve pool will now be auctioned in Q1 2026. The Dec-25 V25 contract closed on 11 December at $73.50, flat on the week.

The advance auction for V28 WCAs saw the sale clear at $29.40, and at 1.72, the cover ratio was the highest ever recorded. Compliance entities received 71% of the V28 WCAs on offer, the second-highest level of successful bids by compliance entities on record after the Q2-2023 level of 73%. The much lower price for the V28-vintage WCAs reflects market expectations that Washington will have linked its cap-and-invest program with California’s by the time the compliance obligation for 2028 is due, with the clearing price of $29.40 representing an 11-cent premium to the equivalent V28 CCA price on December 2, the day before the auction, but a discount to the secondary-market price, which traded flat across the week at $33.49.

CCAs rose 82 cents (+2.8%) over the last week to trade at $30.25 mid-afternoon on 11 December, with the options expiry on 15 December the next market event in view, and with decent levels of open interest (OI) on both the calls and the puts at the $30 strike price for the Dec-25 V25 contract as of 10 December (8.9m OI on the calls, 11m on the puts according to Carbon Pulse). The fundamental key to the CCA market in the near term, though, remains the long-awaited publication of the Initial Statement of Reasons (ISOR), by the California Air Resources Board (CARB). We would expect a bump in CCA prices if CARB publishes the ISOR before the forthcoming holidays, and conversely a slight drop or sideways drift in prices if there is a further delay into the new year.

EU institutions agree 2040 Climate Law, speculators further increase long EUA positions

Last week saw the EU Commission, Council, and Parliament reach a compromise agreement on the legislative framework for the 2040 EU Climate Law in the first trilogue meeting on Tuesday. Under the deal, the 90% reduction in EU-wide emissions required by 2040 versus 1990 levels will allow for 5% of emissions reductions to be offset with international offsets (Article-6 credits under the Paris Agreement), meaning that the net emissions reduction in the EU itself will be 85%. The question as to whether Article-6 credits will be allowed for use in the EU-ETS from 2031 onwards will be addressed at a later date, probably during the EU-ETS Review in the second half of next year.

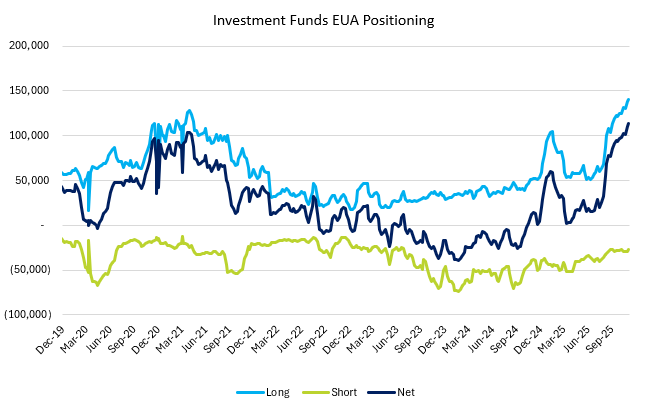

The latest Commitment of Traders data published on December 10 showed a second consecutive ATH in net speculative positioning in EUAs, with investment funds increasing their net holdings by a further 3m tonnes (Mt) to 113Mt. This reinforces the consensus view that balances in 2026 and 2027 are very tight, with analysts expecting a drawdown of 150-200Mt in the total number of allowances in circulation (TNAC) – the outstanding market inventory – in 2026. There is also likely a tactical element to the further increase in net speculative length, as today (December 15) sees the last EUA auction of 2025. With no new primary supply for three weeks and markets thinned of liquidity by traders’ holidays, prices usually bounce 5-10% over this end-of-year period.

EUA prices rose 2.2% last week, closing at €83.79 on December 12, having posted a high for the week of €84.40, just 10 cents shy of the year-to-date (YTD) high of €84.50. The December options expiry was uneventful, and with the Dec-25 contract expiring today, the Dec-26 contract becomes the benchmark contract. Dec-26 EUAs settled at €86.04 on December 12, again close to the YTD high of €86.99, and €90 now seems within reach over the next couple of weeks, given the holiday auction drought.

Carbon Market Roundup

The weighted global price of carbon was $59.20, up 2.2% week over week. EUAs were up 2.2% over the week, at €83.79. UKAs were down 0.4% at £55.90. CCAs were up 1.6% at $30.42. RGGI fell 4.2% to $26.35, while WCAs settled at $74.00, up 0.7% for the week.